Summary

For more than a century, gas has been deeply enmeshed in the Australian economy. It heats our homes and cooks our food, generates electricity, fuels industry, and brings in export income.

But in the past decade, this has started to change. As Australian households and businesses search for cheaper, cleaner, and more efficient fuels, they are using less gas.

Governments have largely ignored this decline, and have failed to plan for it. As a result, new problems are emerging: electricity networks are under strain, backup generation for the power system is not being built fast enough, gas bills are rising, and manufacturers are closing.

And yet, the use of gas will need to decline even faster to meet emissions-reduction targets. The energy transition is also a transition for gas – from a widespread fuel to one that occupies some vital but small niches in a mostly-electrified economy.

Without action, gas use will continue to decline, but the process will be costly, chaotic, and inequitable. Governments must take control to both accelerate and manage the gas transition.

First, governments should implement policies to methodically and predictably reduce gas use across the economy. This includes setting phase-out dates for the use of gas in households, using the Safeguard Mechanism to encourage industrial decarbonisation, and reforming the electricity market to properly price both the emissions costs and the reliability value of gas. Policies to fix forecast gas shortages should put demand reduction ahead of increased supply.

Each sector will move at a different pace, depending on its options. Even in a mostly-electric economy, there will still be some residual demand for gas. To meet this demand, Australia will need supplies of renewable gases such as biomethane and hydrogen. Governments should drive their development with targeted grants, finance, and a demand-side obligation.

A declining gas market will need to be managed very differently, to avoid sky-rocketing prices for consumers and stranded assets for gas network owners. Governments should reform pipeline regulation to facilitate progressive decommissioning.

The role of gas-powered electricity generation is also changing. It is running less often, but is increasingly valuable as a backup during rare renewable energy droughts. The federal and state governments should use upcoming reforms to the wholesale electricity market to remove financing barriers for new gas-powered generators.

Less demand for gas means more demand for electricity. Without integrated planning, consumers and taxpayers are exposed to the risk of over-investing in gas and under-investing in electricity infrastructure. Gas and electricity system planning should be integrated to keep infrastructure costs low, and ensure the electricity network can handle increased demand from gas-to-electric switching.

While LNG producers are riding high at the moment, they face a future of being high-cost producers in a shrinking market as other countries move to reduce their reliance on high-cost and imported energy sources. For as long as the LNG industry lasts in Australia, governments should ensure it pays its share of tax, cleans up after itself, and keeps its emissions under control.

Australia is at a critical juncture in energy policy. The decisions made now around gas will have lasting ramifications. The gas transition will not get easier or cheaper if we wait. The choice is between chaotic and inequitable, or steady and fair. It’s time to move.

Recommendations

Recommendation1

Reduce demand for gas across the economy, with targeted policies across households, industry, and power generation, including phase-out dates for residential gas use.

Recommendation 2

Accelerate growth of the biomethane and green hydrogen sectors with better targeted industry policy and a new national scheme to drive demand for renewable gases.

Recommendation 3

Reform regulation and planning of gas distribution networks to enable and encourage the safe, progressive decommissioning of the network as households electrify. Share the costs between consumers, industry, and government through a grand bargain.

Recommendation 4

Get market settings right to ensure there is sufficient gas-powered generation in the National Electricity Market.

Recommendation 5

Better integrate gas and electricity planning to enable a least-cost transition away from gas by expanding the Integrated System Plan to include gas, and integrating the build-out of electricity networks with the phase-out of gas distribution networks.

Recommendation 6

Prioritise demand-side measures to address future gas supply gaps by expanding the Australian Energy Market Operator’s ability to identify and use demand-reduction tools.

Recommendation 7

Manage the LNG sector more actively to maximise its benefit to Australia. Prepare for a post-LNG economy by reforming gas taxes, requiring emissions cuts from LNG, and using industry policy to replace the economic contribution of LNG.

1 It’s time to get out of gas

Australia has used gas since the 19th century, when towns gas first lit our streets. Large-scale use of natural gas took off in the late 1960s on the east coast, and the 1970s on the west coast. Australia is also one of the world’s largest exporters of gas.

Gas production and use makes a material contribution to Australia’s greenhouse gas emissions, around 20 per cent.1DCCEEW (2026), DISR (2024). In this report, we use the term ‘gas’ to describe fossil methane, also called natural gas. There are two routes to reduce these. The first is to stop using gas by switching to electric alternatives. The second is to continue to use gas, but abate the emissions by switching to renewable gas, using carbon capture and storage (CCS) to prevent emissions, or removing those emissions from the atmosphere at a later date.

Current policies are sending us down the second route without considering the consequences. The federal government’s Future Gas Strategy implies we can reach net zero while keeping gas production and usage high beyond 2050. But this would require impracticably large volumes of renewable gases, wide deployment of CCS, and large volumes of carbon removals.

These solutions are unlikely to be available in the volumes required at prices people are willing to pay. Renewable gas is a nascent industry in Australia, and while it has potential to grow, it has limits that mean it is unlikely to supply volumes equivalent to (fossil) gas today. Carbon capture can only deal with a small subset of emissions from gas production. Carbon removals are scarce, competition for them will be fierce, and there are persistent concerns with their reliability.

It is almost certain that gas use will need to decline substantially to hit net zero.

1.1 Producing and using gas generates emissions

Gas results in emissions in two ways:

- Producing gas (getting it out of the ground and processing it) generates both carbon dioxide and methane emissions.2Methane is a potent greenhouse gas, with 28 times the global warming effect of carbon dioxide per tonne measured on a 100-year timescale: DCCEEW (2025a). When methane is extracted, some escapes through seals and pipes directly to the atmosphere. Sometimes, it is intentionally ‘vented’ for operational reasons, and sometimes producers burn it (‘flaring’) to convert it into the less potent carbon dioxide. Underground gas reservoirs usually contain a mix of carbon dioxide and methane. The carbon dioxide is removed and released into the atmosphere as pollution: Clean Energy Regulator (2024).

- Using gas (burning it in factories, power plants, and houses) generates carbon dioxide.

A small portion of production-related emissions are related to gas for domestic use. But because most gas produced in Australia is for export, about 40 per cent of Australia’s total gas-related emissions come from producing gas that is then exported.3The emissions from burning Australian gas that is exported are not counted in Australia’s emissions – they are counted in the countries where they are burned.

And while Australia’s overall emissions are declining, the relative contribution of emissions from gas is rising: the share of gas-related emissions rose from 14 per cent of overall emissions in 2012 to 23 per cent in 2022.4DCCEEW (2026).

1.2 There are two routes to abating gas emissions – the electrification route and the gas route

There are two routes to abate the emissions from gas. The first, and simplest, is to stop using gas altogether by switching to electricity. This is already technically possible for many, but not all, users. The second route is to continue to use gas, and deal with the emissions another way:

- Switch to renewable gases, which do not emit greenhouse gases when produced or used (see Box 1).

- Use fossil gas, capture the emissions at the source, and permanently store them underground, using CCS.

- Burn fossil gas, emit greenhouse gases, and remove these emissions from the atmosphere later.5In this report we use the term ‘removals’ rather than offsets to reflect that most offsets used today remove atmospheric carbon; and that to achieve net-zero emissions, all offsets must reflect carbon removals rather than avoided emissions.

Achieving net zero from gas requires balancing four questions:

- What can be electrified, by when, and at what cost?

- How much renewable gas will be available and at what cost?

- How much can carbon capture feasibly reduce emissions?

- How much can we rely on carbon removal to offset any remaining emissions?

The infrastructure, regulation, and market design required to meet Australia’s energy needs look very different depending on the answers.

The shape of the economy in 2050 depends on the capacity of the three options to deliver abatement, and their relative attractiveness compared to electrification.

1.3 Australia’s current policy of high gas use forever is a risky approach to decarbonisation

The federal government’s Future Gas Strategy forecasts that gas production and consumption will stay high indefinitely. This is a high-risk strategy because it relies heavily on renewable gas, carbon capture, and carbon removals, to meet Australia’s emissions targets. While each will play a role, they can’t sustain gas use at forecast levels.

Based on current forecasts, gas use will stay high long into the future

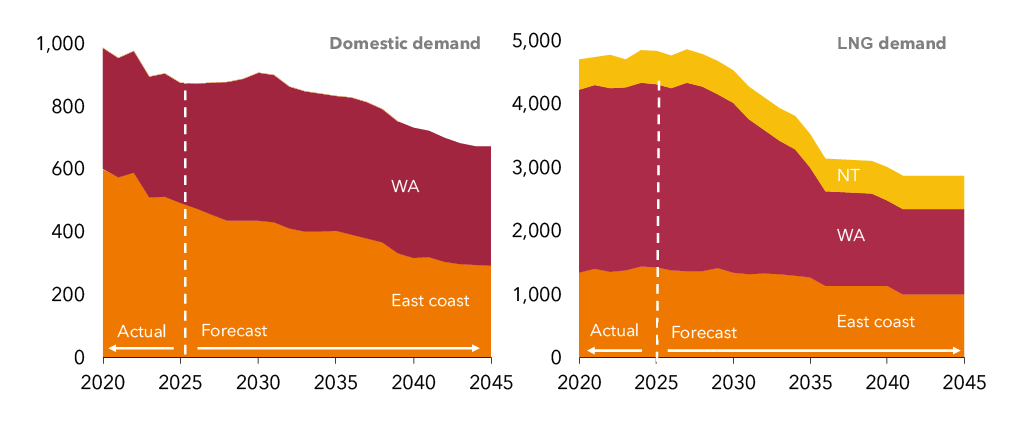

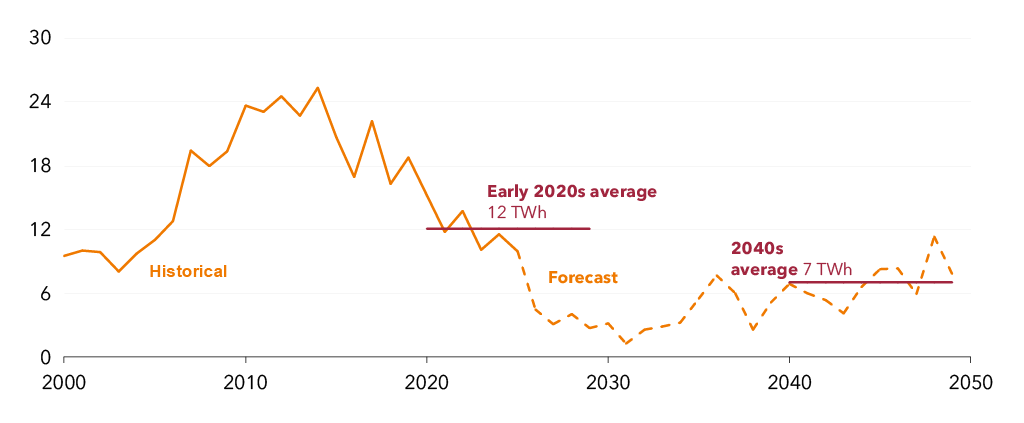

Australia is currently planning for billions in gas infrastructure because the Future Gas Strategy assumes very high gas use out to 2050 and beyond. The Australian Energy Market Operator’s latest 20-year forecasts are for domestic gas demand to decline by just 23 per cent by 2045 (see Figure 1.1 on the following page).

On the east coast, domestic demand is forecast to drop more than 40 per cent, mostly driven by an 80 per cent decline in gas use in buildings (residential and commercial). Demand for gas in industry declines 26 per cent, and demand for gas used in gas-powered electricity generation declines just 1 per cent.6All figures compare 2045 to 2026. AEMO (2026a).

A market with demand dropping 40 per cent over 20 years is in fairly rapid decline. Still, a market consuming 300 petajoules of gas in 2045 will face huge challenges in hitting net zero just five years later.

On the west coast, the challenge is even more daunting. AEMO is forecasting gas demand will only marginally decrease, by 4 per cent to 381 petajoules, by 2045. Gas-powered electricity generation is forecast to decline by about a fifth, and household gas use by a half. But industrial gas demand is forecast to increase by 8 per cent over the next 20 years.7AEMO (2025a).

Demand for Australian liquefied natural gas (LNG) exports is forecast to decline faster than domestic demand, but the LNG sector is still forecast to be four times the size of the domestic gas sector by 2045.8Future LNG demand is difficult to predict. AEMO and federal government forecasts of future LNG demand declines are based on existing LNG contracts expiring, declining global LNG demand, and Australia being edged out by cheaper competitors. These trends are discussed further in Chapter 7.

Australia currently exports about 4,500 petajoules of LNG per year. Gas demand for that purpose is forecast to decline by about 40 per cent to 2,800 petajoules by 2045.9Most of this forecast decline comes from WA exporters. Legacy gas fields on the North West Shelf have been declining, to the point that Woodside retired a 2.5 megatonne train at the facility in 2025: Woodside (2025). New supply may be delivered from development of the Browse basin, but this project remains economically uncertain. The forecast of 2,800 petajoules assumes a constant amount of LNG exports from the NT in line with recent export figures, as no reliable independent forecasts are publicly available. Existing LNG demand is slightly overestimated through the combination of Australian Energy Statistics for NT with GSOO data for LNG production.

Figure 1.1: Demand for gas is forecast to remain high into the 2040s

PJ of gas demand

Notes: PJ = petajoules. East coast estimates are compiled from the 2026 Gas Statement of Opportunities and west coast estimates from the 2025 WA Gas Statement of Opportunities. NT LNG estimates are forecast as flat, based on current data in the Australian Energy Statistics. A full explanation of volume and emissions forecasts is in Appendix A.

Sources: AEMO (2025a), AEMO (2026a), DCCEEW (2025b).

High gas use means heavy reliance on implausible abatement options

High gas use means hitting net zero would require large amounts of renewable gases, CCS, and carbon removals.

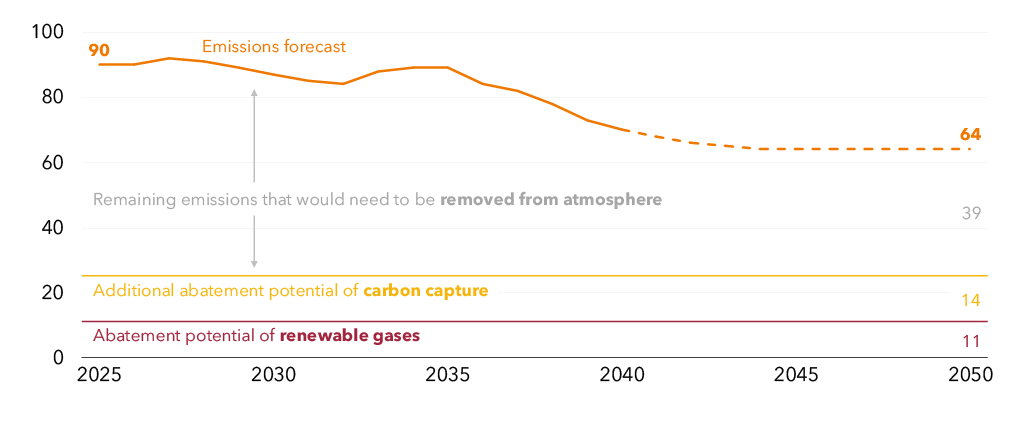

Analysis of the federal government’s emissions projections suggests Australia’s gas-related emissions will decline from 90 million tonnes today to 64 million tonnes by 2050 (see Figure 1.2).10See Appendix A for how this projection was calculated.

But any remaining emissions from gas in 2050 would all need to be offset through carbon removals.

On these projections, Australia will have too many emissions from gas in 2050 to hit net zero. The largest plausible role that renewable gases, CCS, and carbon removals might play is still not enough to enable the use of large volumes of gas. In the remainder of this chapter, we outline what role each of those options could realistically play.

Figure 1.2: Renewable gases and CCS can only solve a small share of gas emissions, and relying on carbon removals to tackle the rest is risky

Projection of gas-related emissions and estimated role of abatement options under current policies, MtCO2-e

Note: MtCO2-e = millions of tons of carbon dioxide equivalent emissions, and includes other emissions (such as methane) converted to carbon dioxide-equivalent amounts.

Sources: Grattan analysis of DCCEEW (2026), DISR (2024), AEMO (2026a), and AEMO (2025a).

Box 1: Renewable gases

Hydrogen is a critical input into a range of commodities including fertilisers, explosives, and chemicals such as methanol. Hydrogen can be made through a range of methods:

– Grey hydrogen is made by reacting methane gas with steam. This produces carbon emissions. Almost all hydrogen made in the world today is grey.

– Brown hydrogen is made by gasifying coal, which again produces carbon emissions.

– Green hydrogen can be made by running an electrical current through water. When using zero-emissions electricity, this method is zero emissions and is considered a renewable gas. This requires large volumes of renewable electricity delivered to the electrolyser site, alongside a reliable supply of purified water.

The hydrogen is then compressed and stored, or converted for transport and end use.

Green hydrogen could be used, with retrofitting, as an alternative to fossil methane for industrial gas users that require gas as a feedstock or a heat source. It could be used to replace methane in gas-powered generation – the Kurri Kurri and Tallawarra B power stations in NSW are theoretically capable of running on 15 per cent and 100 per cent green hydrogen, respectively. But neither station has any plans to start using hydrogen.

Biomethane is chemically identical to fossil methane, but is produced from biological sources such as food waste. Most biomethane is produced using anaerobic digesters, sealed tanks where organic matter breaks down without oxygen to form biogas, which is then ‘upgraded’ to biomethane by removing the carbon dioxide.

Burning biomethane, like burning fossil methane, produces carbon dioxide. But biomethane is considered renewable because it releases carbon into the atmosphere that was already in the active carbon cycle – that is, it was absorbed by plants and animals as they grew and would have been returned to the atmosphere through decomposition.

This is distinct from fossil methane, which releases carbon into the atmosphere that had been locked away for millions of years.

Not everyone agrees that biomethane can be considered ‘zero emissions’ or ‘renewable’. Burning organic matter releases carbon much faster than organic decomposition would. Methane can leak from anaerobic digesters. And if land is converted from being an active carbon sink to growing crops that are used for biomethane production, then biomethane production is not zero emissions.

However, biomethane can be produced with near-zero emissions, and so this report considers it a renewable gas and a potential pathway to decarbonising in some use cases.

1.4 Renewable gases will play a role, but it is likely to be small

Some gas-related emissions can be avoided by using more renewable gases – either hydrogen or biomethane – both of which can be produced with zero or near-zero emissions (see Box 1).11BioLPG is a third renewable gas that may play a role. Historically, Liquefied Petroleum Gas (LPG) is used mostly in residential gas bottles and some industrial applications. BioLPG is chemically identical to LPG, but is made from biological sources. This report focuses on hydrogen and biomethane because they will likely play much larger roles than bioLPG. Australia currently consumes about 43 PJ of LPG per year compared to nearly 900 PJ of natural gas: Elgas (2026).

But the resources and costs required to produce large volumes of hydrogen and biomethane are major barriers that constrain the role they can play in replacing fossil gas.

And hydrogen and biomethane present (different) logistical and infrastructure challenges which would need to be overcome to reach a scale where they could be substitutes for large quantities of fossil gas.

In a net-zero economy, both will be required in some quantities. But in practice, neither is likely to be available in the quantities required to replace a meaningful portion of fossil gas consumption, especially when there are cheaper and more efficient substitutes available via electrification.

Hydrogen is energy intensive, expensive and hard to transport

Producing sufficient hydrogen to substitute for natural gas would require substantial electricity generation capacity, electricity grid capacity, and water treatment.

Emissions forecasts in the federal government’s electricity and energy sector plan already assume production of 4 million tonnes of green hydrogen per year by 2050, but most of this is for export-oriented production of green iron and ammonia. Just 1 million tonnes, equivalent to 120 petajoules, is earmarked for ‘domestic decarbonisation’ – the chunk that could be used to help existing fossil gas users abate their emissions.12These figures cover all of Australia, not just the National Electricity Market.

Producing 1 million tonnes of hydrogen requires 48 terawatt-hours of electricity – equivalent to the combined annual output of the Yallourn, Eraring, Loy Yang A, and Loy Yang B coal-fired power stations.13Assuming 70 per cent capacity factor of the coal plants and assuming 70 per cent energy efficiency of hydrogen production as a likely current average of the range of efficiencies from electrolysis: Aminaho et al (2025), Boretti (2024), Jia et al (2025), Le et al (2023). Producing 4 million tonnes of hydrogen would require 31 gigawatts of new electricity generation capacity, nearly 40 per cent of current capacity in the National Electricity Market.14The current installed generation capacity in the NEM is 81 gigawatts: Open Electricity (2026).

Because it requires so much electricity to produce, green hydrogen is expensive. Current estimates are that hydrogen costs about $7.50 per kilogram, about five times the cost of natural gas.15Cost estimate for green hydrogen is based on a composite of public estimates of green hydrogen costs in Australia. See: DCCEEW (2024), GHD (2023), Fortescue (2024).

The physical challenges of moving hydrogen are well-understood. Compared to natural gas, hydrogen is lighter, smaller, ignites easier, burns faster, and holds less energy per unit of volume. Because it behaves so differently to natural gas, without equipment upgrades, it cannot be transported or burned in equipment designed for methane.

As a result, hydrogen use is likely to be concentrated in a small number of large industrial sites with built-for-purpose facilities. So, it is likely to play an important role in decarbonising some uses of natural gas (and coal) that do not have viable alternatives. But because of the challenges of producing it at scale, methane-to-hydrogen switching is not going to be a viable decarbonisation option for most gas users.

Substituting 1 million tonnes of hydrogen (120 petajoules) for fossil methane would meet about 20 per cent of the remaining gas demand in 2045, and reduce emissions by just 6 million tonnes per year. At present Australia produces about 0.1 petajoules of green hydrogen annually. Planning for an industry of 120 petajoules is already extremely ambitious; the capacity to do more seems out of reach.

Cheap feedstocks are scarce, so biomethane is likely to be expensive

Estimates of Australia’s potential to produce biomethane vary widely. One estimate suggested recoverable biomethane stocks could be hundreds of petajoules, able to displace 44 per cent of Australian fossil gas demand.16Yarnold et al (2025).

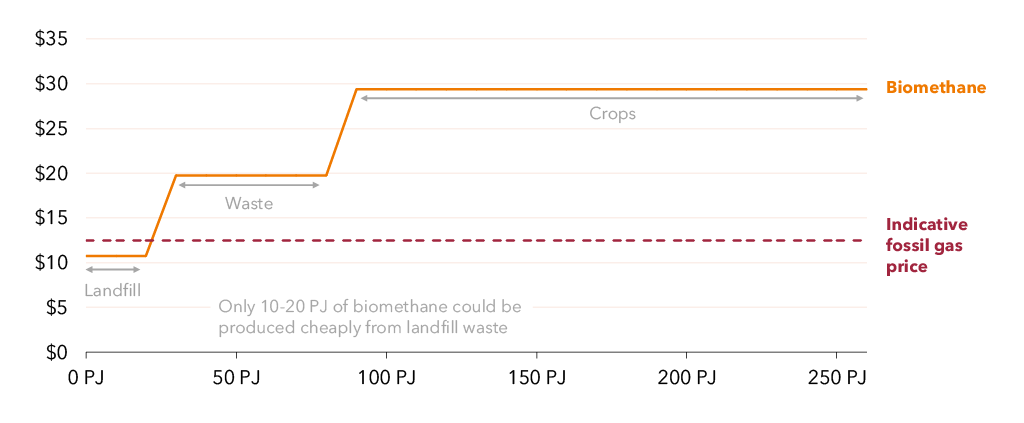

But the current forecasts being used by AEMO suggest that only about 90 petajoules of biomethane could be supplied at a price competitive to fossil gas, even as far out as 2050 (Figure 1.3).

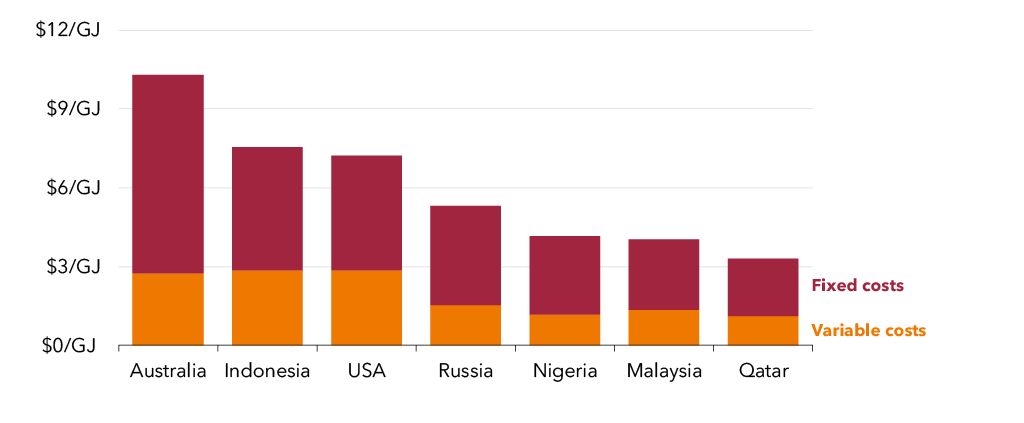

Figure 1.3: Small volumes of cheap biomethane are available, but producing it at scale would require using expensive feedstocks

Estimated costs and volumes of biomethane for different feedstocks in 2050, $/GJ

Notes: GJ = gigajoules. PJ = petajoules. Costs are forecast production costs in 2050, shown in today’s dollars. Indicative fossil gas price based on average domestic prices used in the ISP. Potential availability and prices of gases will change over the forecast period; estimates are best-efforts, based on best available current information.

Source: Grattan analysis of AEMO (2025b).

There are three main sources of biomethane feedstock, each with a different production cost. The cheapest feedstocks are in scarce supply, and the abundant feedstocks are the most expensive. So the more biomethane that is produced, the more expensive it becomes:17ACIL Allen (2025).

- Producing biomethane by capturing and upgrading landfill gas can be done cheaply, at about $11 a gigajoule, but there is not much of it, around 10-20 petajoules per year.

- Producing biomethane from waste could produce another 70-80 petajoules per year, at about $20 a gigajoule. This is about 40 per cent above east coast gas prices for the past 12 months, and at this price, many gas users would be unable to afford the gas.

- Producing biomethane from crop residue could produce hundreds of petajoules per year, but at nearly $30 a gigajoule, it would be prohibitively expensive for most gas users.18Other sources have similar estimates. RACE for 2030 estimates about 400 PJ of total feedstock (compared to 290 PJ from ACIL Allen) and 50 PJ of landfill and waste feedstock (compared to 90 PJ from ACIL Allen): Blunomy (2025), Kaparaju (2023), AEMO (2025b).

Feedstocks for biomethane are generally different to the feedstocks suited to other biofuels, such as sustainable aviation fuels or biodiesel, but some feedstocks can be used to produce multiple biofuels, and feedstock competition is likely to increase as production methods improve and cheap feedstocks are exhausted.19Currently there is little feedstock competition between biomethane and other biofuels: feedstocks such as sewage waste, food waste, and animal manure are currently better suited to biomethane, whereas oils, fats, and woody waste are better suited to liquid fuels. The greater the production of either fuel, the more likely competition is to arise between uses of feedstocks as more expensive routes for production are used, with less optimal feedstocks employed. Developments in technical processes for fuel manufacturing may introduce new competition or complementarity between uses of feedstocks over time.

Aviation, long-distance trucking, and diesel power generation will all rely on these fuels for their path to net zero. They are likely to be more willing to pay for access to scarce feedstocks than many gas users that have electrification alternatives. So competition for feedstocks is likely to tilt supply towards low-carbon liquid fuels rather than biomethane.

Biomethane has unique logistical challenges

Because it is produced by processing organic matter, the production of biomethane is tied to the availability and location of suitable feedstock streams. Digesters must be located close to the sewage treatment centres, farms, or other sources of feedstock that they use to produce biomethane. Facilities fuelled by agricultural residues also face seasonal constraints to their feedstock supply.

Biomethane production differs from fossil gas because it is made from many small, scattered waste sources rather than a few large gas fields.

Fossil gas supply chains are built around moving large, steady volumes through shared infrastructure. Biomethane production is typically smaller-scale and local, transporting batches of biomethane volumes with seasonally variable output, reflecting where organic wastes are generated.

Moving the gas is also harder. Injecting small volumes into the network still requires fixed capital costs for compression, monitoring, and metering equipment. Transmission pipelines are usually built for much larger volumes, and connection points may be far away. As a result, transporting biomethane can be disproportionately expensive, making local use more practical than piping it long distances.

So, similarly to hydrogen, biomethane is likely to be cost-effective in specific cases – gas-powered generation, industrial heat, or industrial feedstocks.

Without a major cost reduction, demand for biomethane is unlikely to exceed the 90 petajoules that could be produced annually for about $20 per gigajoule by 2050.20$20 per gigajoule is the price in 2050 in today’s dollars, assuming cost reductions from today. Leaving aside feedstock costs, the cost of biomethane technology is likely to decline over time, and the cost of biomethane may decline faster than projected as the sector improves feedstock coordination, develops a supply chain and shared infrastructure, and replicates successful business models. But biomethane production is a mature technology, so it is unlikely to see cost reductions from breakthrough innovation. Modelling commissioned by AEMO suggests biomethane costs may decline by a relatively modest $4 per gigajoule by 2050.21ACIL Allen (2025).

Ninety petajoules of biomethane would reduce emissions by about 5 million tonnes of carbon dioxide, and meet less than 15 per cent of forecast gas demand in 2045. Current production levels are essentially zero, and to scale up to produce 90 petajoules will require considerable industry development effort. This is discussed further in Chapter 3.

1.5 Carbon capture and storage can play only a limited role in reducing gas emissions

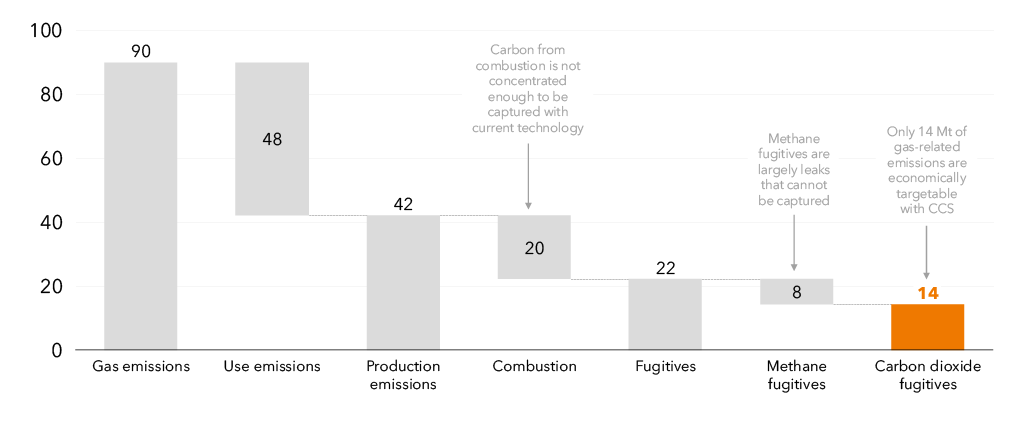

About half of gas-related emissions come from using (as opposed to producing) gas. Most of these emissions are combustion emissions – carbon dioxide given off when gas is burned. These emissions can theoretically be captured and stored.

But most sources of carbon dioxide emissions are too diffuse, or the sources are too small, to easily capture. For large single sources of combustion emissions, using CCS requires new energy- and capital-intensive steps that are unviable without a high carbon price, and uncompetitive with other solutions even with a high carbon price. Because of this, the role CCS can play in decarbonising gas is capped.22The exception is emissions from ammonia production: 40 per cent of these are concentrated and easily separable, and so could be captured: Chahrour and Wulf (2025). There are eight operating ammonia plants with CCS globally. Other CCS methods such as at gas power plants, or even capturing carbon dioxide directly from the air, are currently between 50 per cent and 1,200 per cent more expensive than CCS on natural gas processing: IEA (2020).

About half of emissions from gas production, 20 million tonnes, are combustion emissions, and as noted above, these are difficult to capture. The remaining 22 million tonnes are fugitive emissions – unintended releases of gas to the atmosphere.23DISR (2024). Of these fugitive emissions, eight million tonnes are methane that leaked through gaps in equipment, or are intentionally vented for operational reasons. These can and should be reduced through increased efficiency, but cannot be captured using carbon capture technology.

The rest is carbon dioxide. Some of that carbon dioxide is accidental leaks and venting which CCS cannot capture. The remaining portion is the venting of pure carbon dioxide gas that has been separated. The abatement potential of CCS is limited to this portion of gas emissions (see Figure 1.4).

Figure 1.4: Only a small share of gas-related emissions are currently able to be addressed with economical carbon capture and storage

Emissions from gas production and use, MtCO2-e

Notes: MtCO2-e = millions of tons of carbon dioxide equivalent emissions, and includes other emissions (such as methane) converted to carbon dioxide-equivalent amounts.

Source: Grattan analysis of DCCEEW (2026).

At most, CCS could technically abate 14 million tonnes – about 15 per cent of gas-related emissions.24In reality, only a portion of the 14 million tonnes of carbon dioxide fugitive emissions that are process offgas can be captured, whereas leaks cannot. For the purposes of our calculation we assumed the entire portion could be capturable offgas, because it is not possible to reliably break down these emissions into two categories. Our estimate is therefore a generous one. This is a generous estimate: it assumes that every gas processing facility in Australia has CCS operating with capture rates of 100 per cent.25The Gorgon CCS project off WA has capacity of 4 Mtpa but injected just 1.4 million tonnes in 2024; the Moomba CCS project in SA has capacity of 1.6 million tonnes per year but stored just 0.8 million tonnes last year: Morrison (2025). Given Australia has just two operational CCS projects with capture rates of about 40 per cent, the real volume of emissions that can be abated with CCS is likely to be much smaller.

1.6 There are hard limits on carbon removals

Carbon removals face several hard limits, so relying on them to abate millions of tonnes of emissions from using gas in 2050 is high risk. It would reduce the availability of carbon removals for other sectors, push up the cost of hitting net zero for everyone, or simply result in missing emissions targets.

While in the short term removals are better than no action to reduce emissions at all, in the long term their use must be limited to sectors that don’t have viable alternatives.

Removing carbon from the atmosphere takes a large amount of land

While there are lots of different ways of creating carbon offsets, removing carbon dioxide from the atmosphere through reforestation is currently the most used.26CER (2026a).

If Australia were to offset 64 million tonnes of carbon emissions every year (forecast emissions from residual gas use in 2050), we would need to plant and maintain about 16 million hectares of temperate forest – more than twice the size of Tasmania.27Calculation based on estimates from the Kyoto Protocol State of the World’s Forests: FAO (2001), ABARES (2025).

Planting trees is not the only way to remove carbon from the atmosphere – carbon can be stored in soils and kelp forests, and new technologies are emerging that may play an increased role such as direct air capture and mineralisation. But storing carbon in living ecosystems at scale is challenging, and neither mineralisation nor direct air capture have been proven to be commercially viable at scale even with high effective carbon prices. It is not tenable to base an emissions strategy solely on these.

Carbon removals will be scarce, and competition for them will be high

Gas is not the only sector Australia is trying to decarbonise. Many other sectors with high emissions have no clear abatement option other than carbon removals.

Farming cattle (55 million tonnes of emissions per year), flying planes (9 million tonnes), and making cement (5 million tonnes) are all major sources of emissions in Australia that will likely rely on carbon removals for some time.

Should Australia choose to open domestic carbon markets to overseas buyers, there will also be competition for Australian carbon removals from international customers with hard-to-abate emissions, including in emissions-intensive countries such as Japan, South Korea, and Taiwan. This would open up a potentially lucrative new export industry.28For example, the Australian Energy Market Commission assumes that the shadow cost of carbon offsets would be about $450 a tonne in 2050. If the market for offsets converged to this value, using carbon removals here would be equivalent to forgoing $22 billion in export income: Wood McKenzie (2025a), AEMC (2024).

And carbon removals are not entirely reliable

The reliability of carbon removals has been called into question many times, and reliability is likely to decrease in future.

Numerous studies have found mismatches between forecast and actual carbon offset capacity.29Macintosh et al (2024a), Macintosh et al (2024b), Probst et al (2024). And forestation-based offsets are increasingly vulnerable to climate-induced disruption, which may not be adequately priced in using current methodologies.30Dye et al (2024). Staking Australia’s emissions targets on methodologies with high degrees of uncertainty is high risk.

1.7 Gas use will need to decline substantially to hit net zero

Each of these abatement options – carbon capture and storage, renewable gases, and carbon removals – carries risks and challenges and can only abate small volumes.

Emissions from gas are 90 million tonnes today. At best, carbon capture and storage might abate 14 million tonnes, hydrogen another 6 million tonnes, and biomethane another 5 million tonnes. Relying on carbon removals to do the rest is not feasible; they will not be available in volumes or prices that make this possible.

In short, it is not viable to keep using gas in such high volumes and still expect to hit net zero. The most reliable way to decarbonise gas is to reduce gas consumption by electrifying all uses of gas that can be feasibly and commercially electrified and in the next chapter, we show how to do this.

In the rest of the report, we outline how to manage the decline of the gas market.

2 Safely and predictably reduce gas use

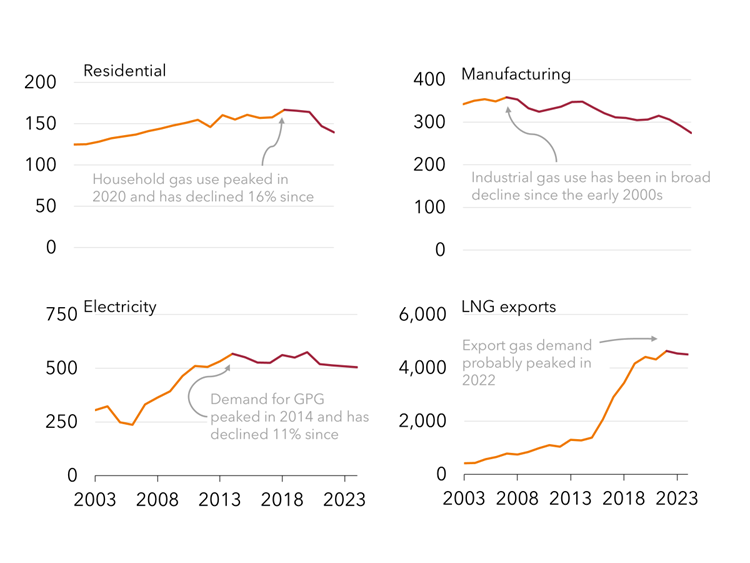

Gas use in Australia is already in decline. Domestic gas consumption has declined from 986 petajoules in 2020 to 876 in 2025, an 11 per cent drop in five years.

The decline is across sectors. Household gas use peaked in 2022 and has declined 16 per cent since. Industrial gas use has been in decline since the early 2000s as manufacturing has declined. And gas for power generation peaked in 2014 and has declined 11 per cent since.

But these declines have largely not been driven by emissions-reduction policy. And they are not fast enough to hit our emissions targets.

Reducing emissions from gas use will ultimately require households and businesses to change their appliances and machinery from gas to electric alternatives. To make sure the asset owner makes the ‘right’ decision, and chooses an asset that uses less or no gas, governments need to send consistent signals about goals and timeframes; and they need to put in place long-term support to overcome barriers to change.

To help households electrify, governments should set phase-out dates for residential gas use, and remove barriers to electrification.

To sharpen incentives to reduce industrial gas use, the federal government should tighten the Safeguard Mechanism. Beyond this, targeted industrial policy will be required to reduce technology and financial risk faced by firms making large capital investments.

In the electricity sector, a carbon constraint is needed to achieve an efficient deployment of gas power generation. Reforming the Safeguard Mechanism is the simplest way to do this.

Coordinated policy across sectors would provide more certainty about the pace and scale of gas reductions, and contribute to meeting emissions-reduction targets. Governments should waste no more time.

2.1 Households are moving away from gas

Across Australia, households have started moving away from using gas for heating, cooking, and hot water (see Figure 2.1).

Figure 2.1: Gas demand in Australia is declining across all sectors

PJ of gas use

Notes: PJ = petajoules. GPG = gas-powered generation. Manufacturing gas use does not include all industrial use. Electricity demand is final gigawatt-hours converted back to petajoules. Full methodology explained in Appendix.

Sources: DCCEEW (2025b), AER (2025a).

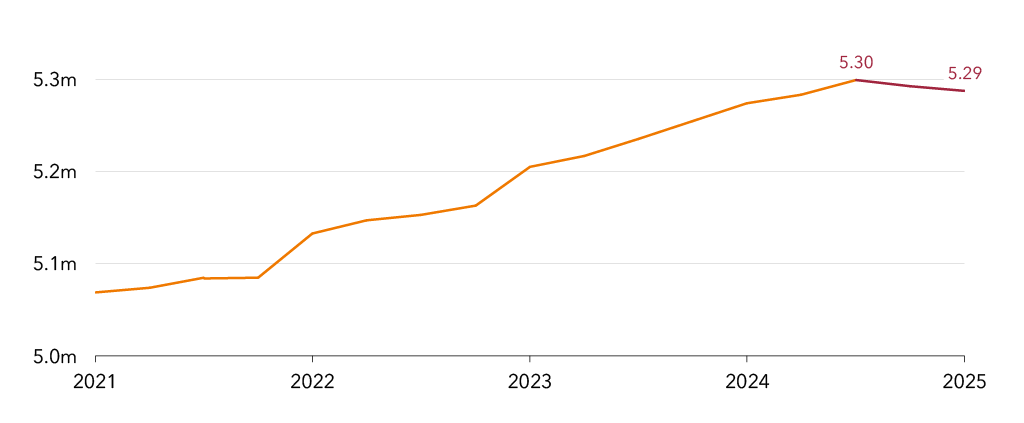

In 2025, for the first time, the number of households consuming gas has declined (defined as customers with an active retail gas plan, see Figure 2.2). Residential gas demand has declined 12 per cent since 2019 on the east coast,31AEMO (2026a). and 27 per cent on the west coast.32AEMO (2025a).

Figure 2.2: The number of households consuming gas has declined for the first time

Total residential gas customers in Australia

Note: Excludes the Northern Territory. This data refers to customers with retail gas plans. Separate network data on gas connections indicate numbers still rising, but the gas retail data provide a more accurate view of the number of customers actually consuming gas, as opposed to customers with dormant gas connections.

Sources: Grattan analysis of AER (2025a), Essential Services Commission (2026), and ERA WA (2025).

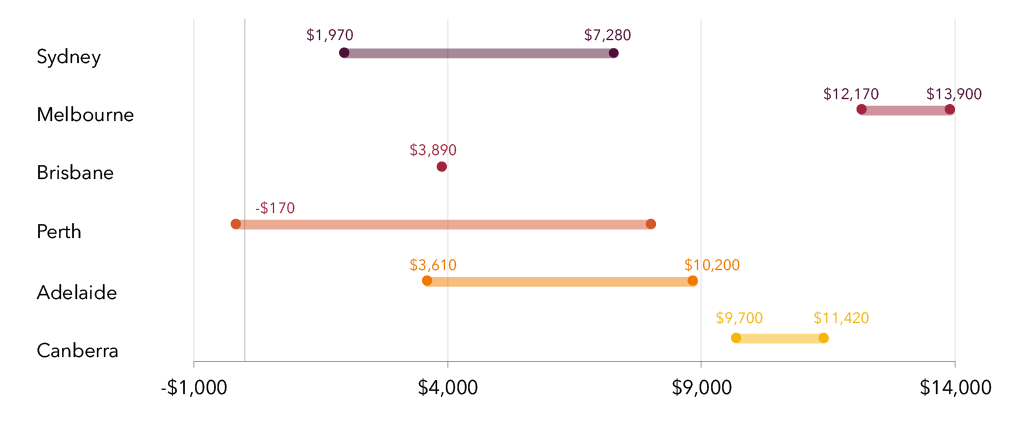

For most households in Australia, upgrading their cooking, water heating, and home heating from gas to efficient electric appliances saves money. These savings can be considerable, especially in colder states such as Victoria, where homes typically use a lot of gas (see Figure 2.3).

Figure 2.3: Most households will save money if they upgrade from gas to electric appliances

Potential range of household savings over 10 years, 2023 dollars

Notes: The leftmost dot reflects the savings over 10 years from electrifying hot water and cooking for a house without gas heating; the rightmost dot is the savings over 10 years from electrifying heating, hot water, and cooking. Includes the upfront cost of new appliances, assumed to be replaced when old ones break. See Appendix B of

T. Wood et al (2023a) for further detail.

Sources: Grattan analysis in T. Wood et al (ibid).

Modelling by the federal government found that by switching to electric cooking, space heating, and water heating, Australian households could save $1,040 per year (including upfront capital costs).33Treasury (2025). In our 2025 report Bills down, emissions down, Grattan’s analysis made a similar finding.34Reeve et al (2025).

But our analysis shows that more than half of households will face one or more barriers to upgrading their appliances to all-electric. For the one-third of households that rent, their appliances are their landlord’s choice, not theirs. For property owners who live in multi-unit buildings, there are issues around common property and building management. Then there are households on low incomes or who have few savings: these households will not have access to the upfront capital required to upgrade. And some older houses will require more significant rewiring to electrify.35T. Wood et al (2023a).

Government action is required in five areas to help households upgrade

For households to access the benefits of all-electric homes, governments need to take action in five areas:

- Policy: Set a date for an end to household gas use; map the pathway to that goal; and integrate planning for the switch from gas to electricity in energy system planning.36Residential gas makes up only a small portion of overall national emissions. However, phasing out gas in homes is a significant logistical exercise – it will take decades to replace millions of appliances. To electrify at lowest cost, those appliances should be replaced at end of life. For these reasons, the electrification of residential gas demand should start immediately.

- Regulation: Ban new gas connections; require decommissioning; and manage the network death spiral.37See Chapter 4.

- Equity: Remove gas appliances from public, social, and Indigenous housing; set minimum rental standards; and provide incentives to landlords ahead of these to replace gas appliances with electric ones.

- Consumers: Give consumers consistent and reliable information about how to make the change, and facilitate access to financial assistance for those who need it.

- Complementary measures: Invest in the additional skilled workers needed to deliver electrification, and regulate electric appliances to ensure the appliances perform well.

To date in Australia, progress on these actions has been patchy. Only the ACT has set a date for an end to household gas. Only the ACT and Victoria have gas roadmaps (the NSW government says it will produce a roadmap in late 2026). There has been some progress in integrating gas and electricity planning, but more work is needed.38This is discussed further in Chapter 6.

Victoria and the ACT have banned new gas connections, and in other states (except WA) the full cost of a new connection must be paid upfront.

The federal and state governments are working together to electrify public, social, and Indigenous housing, but so far only 100,000 of Australia’s 450,000 social houses have been targeted.39DCCEEW (2025c), AIHW (2025). Only Victoria has minimum rental standards that cover gas appliance replacement, and discounts to encourage landlords to electrify and improve energy efficiency in rental properties.

Victoria and the ACT have good information resources available for consumers; other states do not.40For example, Victoria’s State Electricity Commission has launched a one-stop-shop info hub and marketplace for appliances, installers, and government rebate applications. The federal government has tried to encourage private sector finance products to support home upgrades, but data on the rollout is not public. Some states have finance available.

Reverse-cycle air conditioners have been brought into the energy performance regulatory framework, and heat pumps should be included by 1 July 2027. Cooktops remain unregulated.

The federal and state governments should increase their efforts in all the above areas. In particular, states that have not set dates and created roadmaps should do so.

Leaving the transition unmanaged does not preserve consumer choice

While governments continue to avoid setting clear direction, households will keep making long-term decisions, such as replacing gas appliances or connecting to gas networks, without understanding the long-term cost implications or even the likelihood of their gas network being decommissioned.41ECA (2025a).

Avoiding the issue also fails to acknowledge that nearly half of consumers do not have a realistic choice to get off gas. It is these consumers who will be left with higher energy bills in the name of preserving choice for the few who have deliberately opted to remain on gas.

If governments are concerned about consumer choice, they should make the choice real. Consumers who really want to use gas, despite the poor economics, should be nudged towards using LPG. This would mean they take full responsibility for their choice, by handling their own supply instead of relying on a network where their choice is cross-subsidised by those who can least afford it. And consumers who face barriers to exercising the choice to electrify should have those barriers removed.

2.2 Industry is more complex than households

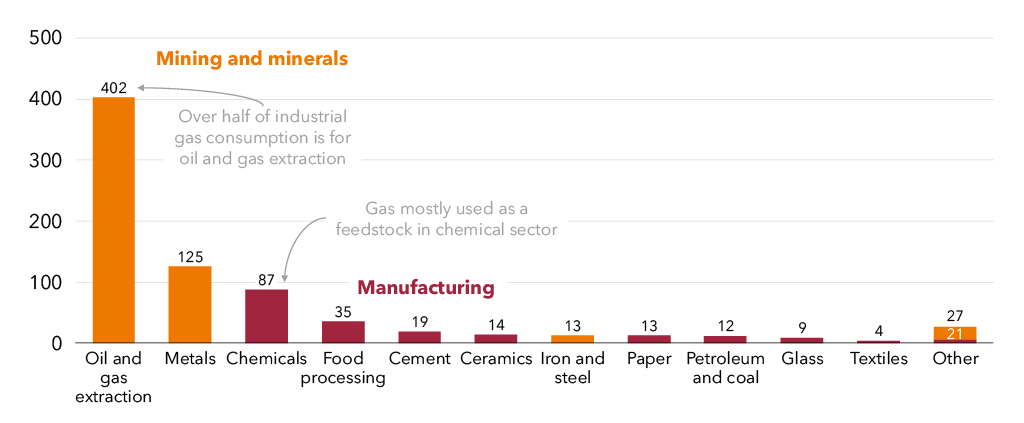

Gas is used in a wide range of industries in Australia: as a feedstock in chemical production for products such as fertiliser and explosives, and providing heat for everything from metals refining and manufacturing to food-processing and paper production.

Most gas used in the industrial and mining sectors is consumed in gas and LNG production, non-ferrous metals refining (particularly alumina refining), chemicals production, and cement production. Most of this gas is used for heat; the exception is the chemicals sector where some of the gas is used as a feedstock (see Figure 2.4).42Feedstock refers to raw materials used for industrial processes. When gas is used as a feedstock, it means it is used for its molecules to create other products, not burned for energy.

Figure 2.4: A few sectors account for the majority of industrial gas use

PJ of gas consumption by sub-sector, 2023-24

Notes: PJ = petajoules. Metals refers to metals other than iron and steel.

Sources: Grattan analysis of DCCEEW (2025b).

Industrial gas demand has been in broad decline since the early 2000s, dropping slightly faster than overall manufacturing energy usage.43DCCEEW (2025b).

This has largely been driven by a decline in manufacturing, from about 15 per cent of GDP in the 1970s to about 5 per cent today, as manufacturers close or move offshore for competitiveness reasons.44See, for example, Dyno Nobel (2021), Dyno Nobel (2025), Industrial Info Resources (2024), and S. Evans and Bleby (2025).

Gas substitutes vary across industries

Much of industrial gas consumption is used to generate low-temperature heat, which can be readily electrified. Up to 50 per cent of Australia’s current process heat market is less than 250°C, much of which is using gas. This suggests a sizeable potential for electrification of current processes.45Based on CSIRO’s analysis of the 2022-23 Australian Energy Statistics: CSIRO (2025).

For process heat below about 150°C — used in food processing, brewing, and light manufacturing — electric substitutes such as heat pumps and electric boilers are already available, and should become more competitive as capital costs fall, providing other barriers do not persist.46RACE for 2030 (2021).

Two other uses of gas are harder to abate – gas burned to generate high-temperature heat, and gas used as a chemical feedstock.

For higher-temperature (more than 250°C) processes in sectors such as cement and metals, electrification remains difficult, and a burnable fuel is usually required. But there are options: for example the AdBri Birkenhead cement plant in South Australia has been using progressively more waste-derived fuel over the past 23 years, replacing up to 50 per cent of gas use.47Boisvert (2026).

In the longer term, the substitute for gas for some users is likely to include biomethane or hydrogen. Much of the gas consumed in the chemicals sector is used for feedstock, not heat. Electrification cannot substitute for this directly; instead an alternative source of molecules is needed, and this is mostly likely to be low- or zero-emissions hydrogen.48Low-emissions hydrogen adds carbon capture and storage to traditional production. This removes about 60 per cent of the associated production emissions. Zero-emissions hydrogen uses 100 per cent renewable electricity to create hydrogen from water. Again, these substitutes are currently expensive to use, and not widely deployed.

There are one or two examples where industrial gas use may increase if gas substitutes for coal (see Box 2).

Box 2: Gas may still be a transition fuel for iron and steel

The large coal users in the industrial sector are the iron and steel, minerals processing, and cement sectors.aDCCEEW (2025b). One way to reduce, though not eliminate, emissions in these sectors is to use gas, instead of coal, for high-temperature heat.

Three factors will influence whether this happens: the relative price of coal versus gas (currently $5-$7/GJ for coal versus $13/GJ for gas); the cost of changing kilns and furnaces; and the availability and price of gas versus zero-carbon substitutes such as hydrogen or electro-smelting.bYCharts (2026) and AER (2025b).

If all Australian steel production switched from coal to gas, it would add to annual gas demand by 50 petajoules, and would approximately halve emissions at these facilities.cGrattan calculation based on Energy Transitions Commission (2023). Direct iron reduction using gas is more energy efficient than using coal.

Switching to using hydrogen has the same extra capital costs and operating costs, but higher fuel costs until hydrogen can match natural gas prices.

Iron and steel is one of the few areas where a coal-to-gas transition may still make sense, to allow time for zero-emissions alternatives to emerge. Switching from coal to gas in 2027 would only result in more emissions over 25 years than switching coal-to-hydrogen if hydrogen became available and competitive by 2038. This would require developing a hydrogen industry in 11 years that could supply 50 petajoules of hydrogen annually (500 times what is produced today) at a price substantially lower than it is today. This seems unlikely.

Reducing industrial gas use faster requires a comprehensive policy suite

As noted above, zero-emissions solutions for much of heavy industry are still developing to commercial scale. Industrial assets have long design lives – sometimes up to 40 or 50 years. The decision process to renew, refurbish, or retire an asset begins well before the end of its life, and future emissions get locked in at the design stage for a new or refurbished plant.49For example, in February 2021, BlueScope announced the beginning of a process to make decisions about a steel smelter which would reach the end of its design life somewhere between 2026 and 2030: Bluescope (2021).

At best, most Australian industrial facilities will have one chance to make a large investment that decarbonises their operations between now and 2050. If lower- or zero-emissions technology is not technically and commercially proven when asset renewal planning starts, a firm may choose not to replace the facility and it will close at the end of its life. If the firm does decide to replace it before zero-emissions technology is available, there is a risk it will do a like-for-like replacement of an old facility, or shift to a proven but still emissions-intensive process. None of these are an ideal outcome.

To prevent this, policies have to tackle two problems simultaneously:

- providing a stable long-term signal that emissions must be eliminated, creating technology pull; and

- providing short-to-medium-term assistance to share the risks of developing the solutions that will do so, creating technology push.

The federal government already has the building blocks for this push-and-pull approach, but it should use them more effectively.

The Safeguard Mechanism is not providing a strong enough signal

The Safeguard Mechanism (see Box 3) is the government’s policy to reduce emissions from the large industrial facilities over the long term.

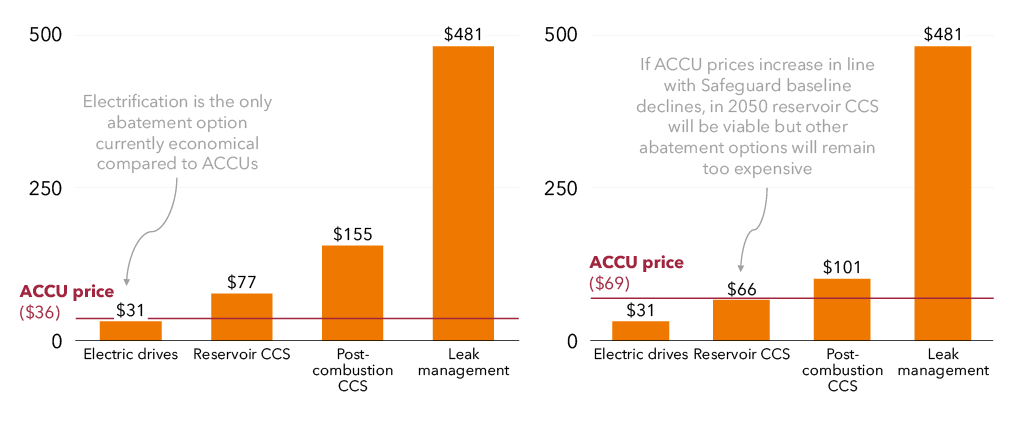

But because it allows unlimited offsetting, and because the baseline decline rate is slow, the signal it sends is weak. At present, carbon credits cost about $36 per tonne of carbon dioxide50Demand Manager (2026). and facilities need only offset the equivalent of 14.4 per cent of their 2022 emissions.

This is an effective carbon price of about $5 per tonne of carbon dioxide. This is far too low to pull through solutions such as green steel or green ammonia, where the gap between traditional production and decarbonised production is more like $100 or more per tonne.51T. Wood et al (2023b).

The Safeguard Mechanism is due to be reviewed in 2026-27. The government should use this process to reform the Safeguard Mechanism to send a sharper signal to develop and deploy low- and zero-emissions industrial technology. This could involve limiting offsetting, increasing the rate of baseline decline, or both.

Box 3: How the Safeguard Mechanism works

The Safeguard was introduced by the Abbott government in 2015, and reformed by the Albanese government in 2022. It applies to any facility that emits more than 100,000 tonnes of carbon dioxide equivalent per year. This includes major industrial facilities, all LNG facilities, most coal mines, three airlines, and some rail freight companies.

Safeguard facilities are assigned a baseline level of emissions. If the facility emits above its baseline, it must surrender carbon credits to cover the difference.aThese can be Australian Carbon Credit Units (ACCUs) or credits purchased from other facilities that emit less than their baselines. If a facility emits below its baseline, it receives credits which it can then sell to other facilities, or save for the future. Facility baselines decline by 4.9 percentage points each year to 2030 and 3.285 percentage points after that.bIn 2024-25, 17 facilities had more generous decline rates of 1 percentage point per year, because they were trade-exposed.

There is no limit to the number of carbon credits that facilities can use to meet their obligations. Of the 207 facilities covered by the Safeguard, in the 2024-25 period, 143 facilities exceeded their baselines. This generated 13.7 million tonnes of carbon dioxide-equivalent above the allowed emissions, and therefore requiring an equivalent number of carbon credits to be surrendered.cCER (2025).

Targeted industry policy is also needed

As noted above, industrial facilities make large capital investments rarely. If new technology is still high-cost or risky at the renewal point, it will not be chosen over proven traditional approaches, even if the latter results in a long-term emissions liability.

For this reason, the government should establish financing facilities to risk-share with large industrial facilities at the point of machinery renewal, so that this renewal uses low-emissions technology.

Governments will need separate but complementary policies to address technology risk and financial risk.52Technology risk is uncertainty about whether a new technology will work. Financial risk is uncertainty about whether a technology can be commercially deployed. Technology risk is more suited to grant-style assistance, because removing technology risk creates positive spillovers (benefits extending beyond those who took the risk), and because the risk of failure is high. Addressing financial risk is more suited to a financial instrument, such as concessional loans.

The federal government already has a suite of policies aimed at industrial transformation including the National Reconstruction Fund, the Clean Energy Finance Corporation, the Powering the Regions Fund, the Net Zero Fund, Hydrogen Headstart and tax credits, the Green Iron Investment Fund, and the Future Made In Australia Innovation Fund. Much of this funding is sitting uncommitted. What is needed is not more money, but better co-ordination and targeting.

Much existing funding is targeted at sectors that need radical improvements in technology and economics to move away from gas. Substantial and long-term risk-sharing between the private sector and government is needed to help these sectors transform. But at present this support comes at the expense of other industries where technology is ready, but the economics are not – for example, the food and beverage and pulp and paper sectors, or alumina digestion.

Small emitters may need a different approach

There is also some gas use in facilities that are below the participation threshold for the Safeguard, such as food processing and paper manufacturing. This gas is mostly used for low-temperature heat, where electricity is a more realistic substitute.

These mid-tier firms are stuck with the worst of both worlds: they are large and complex enough to need bespoke solutions, but not big enough to have dedicated energy management expertise, fund their own R&D, or have easy access to capital.

Many of the ways in which these firms can electrify present risks on both capital costs and operating costs. But government support programs tend to be biased towards sharing capital cost risk, and towards larger projects that carry higher risks.

It may be administratively complex to expand the Safeguard to include smaller firms. Another option may be to use an upstream obligation to create the long-term signal to decarbonise without increasing the administrative burden. At the same time, these firms also need better access to risk-sharing assistance.

Designing detailed policies to reduce emissions, improve energy efficiency, and encourage electrification for smaller industrial emitters is beyond the scope of this report. But lack of policy in this sector is a persistent gap and one that should be filled.

2.3 Gas use for electricity is declining, but needs to be right-sized

Gas use in the electricity sector peaked in 2014, plateaued, and is now in decline. Most models of the future electricity system forecast that some gas will be used as back-up for a mostly-renewables system. But precisely how much gas-powered generation will be needed is difficult to forecast because there are so many uncertainties around future access to gas, emissions policy, and the attractiveness of alternatives.

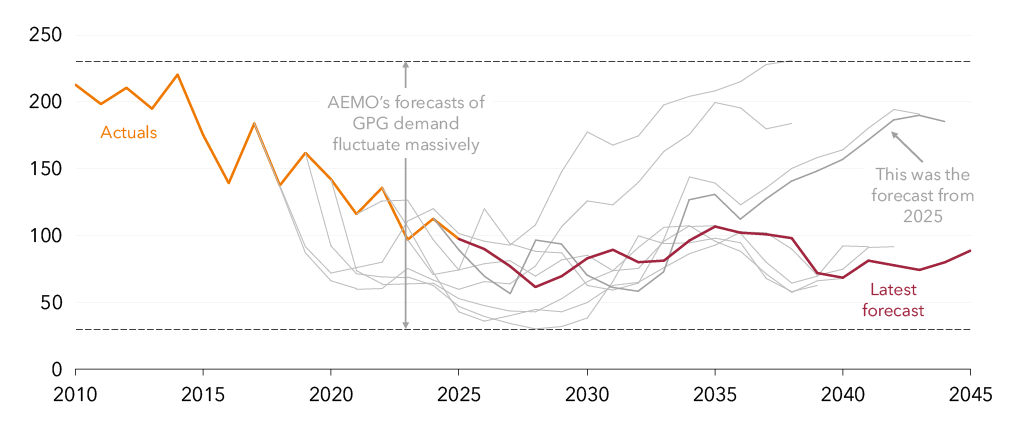

Over the past nine years, the Australian Energy Market Operator’s forecasts of future gas demand for gas-powered generation have varied by up to 200 petajoules, though they are generally declining (see Figure 2.5). Last year’s forecast was that gas-powered generation would require nearly 200 petajoules in 2044, and this year that figure more than halved.

Figure 2.5: AEMO’s forecasts of future gas-powered generation vary widely

Successive yearly forecasts of east coast gas demand for electricity generation, PJ

Notes: PJ = petajoules. AEMO = Australian Energy Market Operator. GPG = gas-powered generation. Forecasts are from base years of 2018 up to 2026.

Sources: Grattan analysis of AEMO Gas Statement of Opportunities, 2018 to 2026.

Until and unless other technologies can more affordably substitute its backstop function as a support during renewable droughts, gas-powered generation is likely to be essential to the safe running of the future power system. But getting the volume of gas-powered generation right depends on properly pricing the emissions impact of running gas-powered generation.

A carbon constraint in the electricity sector is essential to right-size gas-powered generation

To meet emissions-reduction targets, the electricity sector needs to reduce the amount of electricity coming from fossil fuels. Without a constraint on these emissions, coal generation will stay in the system for longer, renewables generation will be lower, and gas generation will be higher.

With a carbon constraint in place, renewables generation would grow faster, and gas output would be lower, because clean sources of dispatchable generation, such as pumped hydro and batteries, would take its place.

There are many ways that a constraint on carbon in the electricity sector could be designed. In our view, the most pragmatic option available to the federal government is to re-activate the Safeguard Mechanism to cover the electricity sector.53The Safeguard Mechanism already makes provision for the electricity sector, but this part of the legislation is currently inactive. We lay out the case for reactivating the Safeguard in more detail in Chapter 3 of Reeve et al (2025).

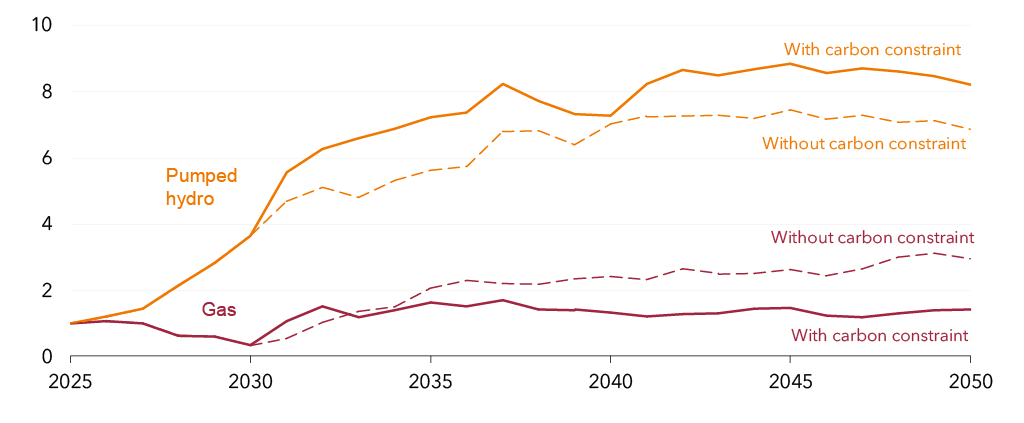

Our modelling shows that there would be less gas-powered generation in the National Electricity Market in coming decades under a reformed Safeguard Mechanism (Figure 2.6). Gas is still present, and playing the important role of backing up the system when renewables and storage are not sufficient. But, because it is paying for the climate damage caused by its emissions, its role is limited to the times when it is strictly necessary. With emissions properly priced, other sources of dispatchable generation, such as pumped hydro, deliver an increased share of generation.

Figure 2.6: Without a carbon constraint in the electricity sector, gas takes a much higher share of the market for dispatchable generation

Index of pumped hydro and gas-powered generation output, with and without an emissions constraint, 1 = 2025 output

Notes: Carbon constraint applied from 2030, consistent with an emissions budget where Australia meets its 2030 and 2050 emissions-reduction targets, and meeting the reliability standard. For full details see Appendix B of Reeve et al (2025).

Sources: Jacobs for Grattan, Reeve et al (ibid).

Importantly, our analysis also shows that the overall system cost is lower with a constraint in place than without one.54Ibid.

Recommendation 1:

Reduce demand for gas across the economy, with targeted policies across households, industry, and power generation:

– Set dates to phase out residential gas use.

– Remove barriers that many households face to electrification.

– Reform the Safeguard Mechanism to sharpen incentives for large industrial users of gas to reduce emissions.

– Better target existing industrial policy to reduce technology risk and financial risk for large industrial emitters.

– Fill the policy gap for small industrial facilities.

– Reactivate the Safeguard Mechanism in the electricity sector to accelerate power system decarbonisation.

3 Expand the renewable gas sectors

Renewable gases will be critical decarbonisation routes for some users of gas who will find it difficult to electrify. But both types of renewable gas – biomethane and hydrogen – face barriers to being used at any meaningful scale. Governments must accelerate their deployment.

Green hydrogen has benefited from government support to develop small-scale electrolysers, but no one is buying the gas. There are very few users of hydrogen today, and none seem likely to switch to green hydrogen at scale without significant further government support.

Switching a customer from methane to hydrogen involves large capital costs. But without a large buyer, green hydrogen will not grow. The federal government should focus on unlocking the first wave of big green hydrogen buyers by targeting production-side support to existing users of grey hydrogen to lower the cost of switching.

Biomethane faces the opposite problem. Thousands of businesses use methane everyday, so the market is there. But biomethane has not enjoyed the same level of support as hydrogen to develop production facilities. The government should accelerate support for biomethane production to reduce costs and de-risk private investment.

Once both industries are operating at small scale, the government should use demand- and supply-side measures to accelerate them. Instead of Victoria and NSW introducing separate renewable gas targets in 2027 as planned, there should be a single national scheme to drive demand for renewable gases.

And the federal government should remove broader barriers to renewable gases. For hydrogen, this means a relentless focus on lowering the cost of electricity, the biggest driver of green hydrogen costs. And biomethane producers will need a clear feedstock strategy, and support to compete against incumbent gas companies.

3.1 Renewable gases are still fledgling in Australia

There are few producers and even fewer users of green hydrogen

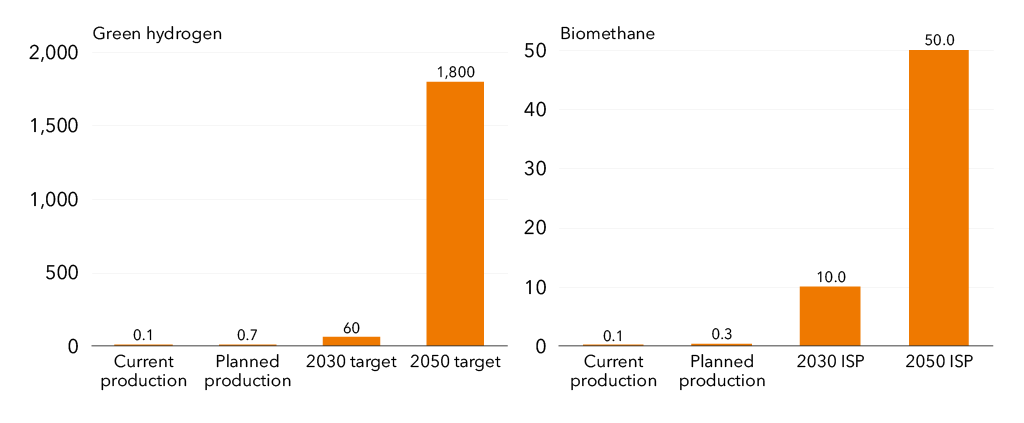

There are just 13 operating electrolysers in Australia today, with a collective green hydrogen production capacity of about 1,000 tonnes per year, about 0.1 petajoules.55CSIRO (2026).

The existing electrolysers are mostly for niche uses such as transport, and are remote from the major sources of potential long-term hydrogen demand. A further 10 electrolysers under construction have a capacity of about 4,600 tonnes per year, another 0.6 petajoules.

This compares to the federal government’s target to produce 60 petajoules of hydrogen by 2030, and 1,800 petajoules by 2050.56Hydrogen targets are set in tonnes: 0.5 million tonnes for 2030 and 15 million tonnes for 2050. We convert tonnes to joules using a conversion factor of 120 megajoules per kilogram of hydrogen. To hit these targets, Australia would need to increase hydrogen production 86-fold in the next four years, and 2,600-fold by 2050 (Figure 3.1).

Figure 3.1: Australia is a long way off track for renewable gas production

Annual production of green hydrogen and biomethane, PJ

Notes: PJ = petajoules. ‘Planned production’ refers to electrolysers under development for hydrogen and the planned Delorean and Wasleys biomethane projects.

Sources: Current production is from CSIRO (2026). Green hydrogen targets are from DCCEEW (2022) and biomethane targets are from AEMO (2025b).

Biomethane is also a tiny sector, with just one producer

Biomethane is even smaller, with just one operational production facility – Jemena’s Malabar facility in NSW, which produces 95 terajoules (0.095 petajoules) per year.57Jemena (2026).

Australia today has about 250 anaerobic digesters, producing biogas from decomposing organic matter.58Biogas, a mixture of methane and carbon dioxide, is the gas produced from anaerobic digestion of organic matter. Biomethane is produced by ‘upgrading’ biogas (removing the carbon dioxide). These digesters produce about 20 petajoules of biogas each year, about 1.5 per cent of Australia’s gas demand.59IEA (2024a).

Malabar is the only one of these that upgrades its biogas into biomethane. This is despite the biomethane production process being a mature technology – Europe alone has more than 1,600 grid-connected biomethane digesters.60EBA (2025a).

A small pipeline of new biomethane projects is starting to emerge in Australia:

- The Delorean project in Adelaide will process food waste to inject up to 210 terajoules of biomethane a year into the gas network.

- The Wasleys piggery, also in Adelaide, will process pig effluent to inject up to 40 terajoules of biomethane a year into the gas network.

- A much larger facility, Kalfresh, is under construction in Queensland and will process agricultural waste to generate electricity in a gas peaking plant.

But these projects are mostly sub-scale demonstration plants, not yet the signs of an industry taking off, and well short of the volumes that would play a meaningful role in the energy transition.

This is concerning, because biomethane is likely to be an important route to decarbonising hard-to-electrify gas applications at least cost. The Integrated System Plan assumes the availability of about 10 petajoules of biomethane by 2030 (which would require Australian production volumes to increase more than 100 times in the next four years) and 50 petajoules of biomethane by 2050 (which would require production volumes to increase more than 500 times over 24 years).61See Figure 20 in AEMO 2025b.

The global biomethane market is growing fast – in the past three years, the US has expanded production capacity by an average of 16 per cent a year62Wood McKenzie (2025b). and the EU by an average of 20 per cent.63EBA (2025b). The Australian biomethane sector would need to grow much faster than this to play a meaningful role in the gas economy.

The long-term outlook for biomethane production potential in Australia is highly uncertain. A report for Energy Networks Australia estimated that Australia has the potential to produce 400 petajoules of biomethane each year.64Blunomy (2025). Yet global biomethane production volumes in 2023 were just 295 petajoules.652023 is the most recent data available at IEA (2025a). Two things are clear about Australia’s biomethane sector – first that a material volume of biomethane will be essential to achieving net zero at least cost, and second, that on current trends, Australia will not deliver biomethane in anywhere near the volumes required.

3.2 Industry policy should do four things to help these sectors grow

Australia grew the renewable electricity sector to the size it is today by using sequenced industry policy that provided different support as the sector grew:

- Technology-specific support, typically through grants to deploy first-of-a-kind demonstration projects.

- Supply-side support, to increase production to a minimum viable amount to support an industry. This was usually delivered as larger grants or loans through bodies such as the Clean Energy Finance Corporation.

- Demand-side support, in the form of a target and tradeable certificate schemes, with an obligation on large businesses to purchase certificates from producers.

- Further support if needed to maintain growth, such as an ongoing de-risking mechanism to unlock private sector investment (for example through contracts for difference), or the provision of common infrastructure.

Neither hydrogen nor biomethane has enjoyed this kind of systematic support. For hydrogen, government policy tried to leap to stage 4 (ongoing de-risking) while stages 1 and 2 were still playing out. For biomethane, government policy has generally been lacking across the board. For both gases, state-based renewable gas targets are now proposed to come in from 2027, which is too soon, because neither sector has reached minimum viable scale.

Industry policy for both gases needs a reset.

3.3 Hydrogen policy moved too fast for a nascent industry

Policies aimed at growing the green hydrogen sector have not been coordinated across the federal and state governments, and have so far been unsuccessful in stimulating the development of scaled electrolysis capable of producing green hydrogen in volumes and at prices that represent a viable decarbonisation pathway.

To date, the Australian Renewable Energy Agency has provided $361 million in grants to 69 projects related to hydrogen. This funding has overwhelmingly gone to small-scale hydrogen production projects.66ARENA (2026).

More recently, the federal government has announced two policies aimed at stimulating large-scale hydrogen production:

- Hydrogen Headstart – a $2.4 billion fund to provide revenue support to large hydrogen producers equivalent to the difference between the cost of production and the market price.

- The Hydrogen Production Tax Incentive – a refundable tax offset of $2 per kilogram of hydrogen.

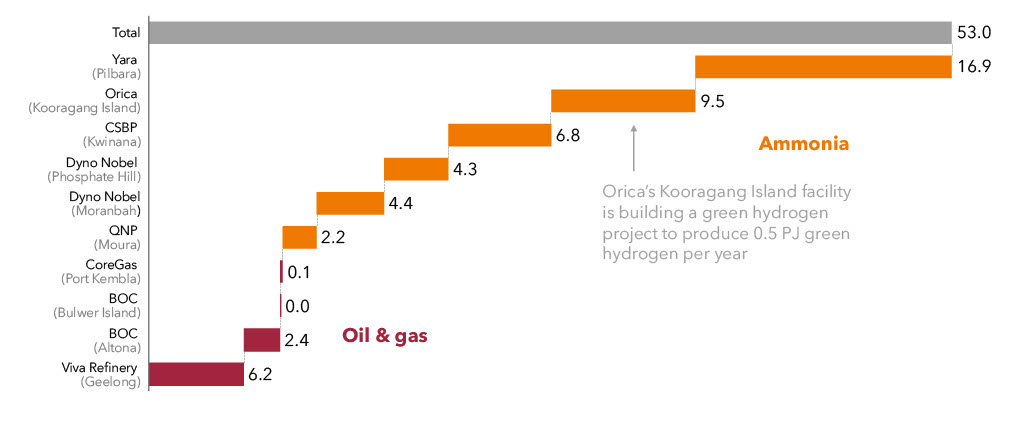

To date, Hydrogen Headstart has announced funding for two projects, neither of which is yet operational. One is Orica’s Kooragang Island explosives factory in Newcastle, which currently consumes nearly 10 petajoules of grey hydrogen per year (see Figure 3.2). The electrolyser will produce 0.5 petajoules of green hydrogen per year, and represents the first case of grey-to-green hydrogen switching in Australia.67The second project, the Murchison Green Hydrogen Project in WA, is for export ammonia, so does not displace existing grey hydrogen consumption in Australia. The recipients of the second round of Hydrogen Headstart funding are set to be announced at the end of 2026, and the hydrogen tax incentive does not commence until 2027.68In the 2026 budget, the Federal government reduced the funding available under Round 2 of Hydrogen Headstart by $1 billion and pushed back its forecasts of expenditure under the tax credit to reflect the slower than anticipated growth in the hydrogen sector.

Figure 3.2: Currently just 10 facilities in Australia use hydrogen, all of it grey

Annual hydrogen consumption, 2022, PJ

Notes: PJ = petajoules. Grey hydrogen refers to hydrogen produced from methane steam reforming. Estimates of hydrogen consumption at Ampol’s Lytton refinery are not available.

Source: Grattan analysis of DCCEEW (2022).

Despite the substantial commitment of funds, most have yet to be disbursed, and progress on large-scale hydrogen projects has largely stalled. A slew of major projects have been cancelled in recent years:

- In October 2024, Origin Energy withdrew from a partnership with Orica to build the country’s largest hydrogen production plant, in the Hunter Valley, citing the high cost of hydrogen.69Origin Energy (2024).

- In July 2024, Fortescue Future Industries cancelled its plan to build a hydrogen production plant at the site of AGL’s old Liddell coal mine in NSW, stating it was prioritising other hydrogen opportunities.70Murphy and Condon (2024).

- In May 2025, the South Australian government cancelled its plans to build a hydrogen electrolyser in Whyalla, citing delays in the local steelworks’ plans to use hydrogen for steel-making.71MacLennan (2025).

- In July 2025, Stanwell cancelled its plans to build the $12.5 billion CQ-H2 hydrogen production plant in Gladstone, Queensland, after the new state government withdrew funding for the project.72Hines (2025).

Production-side support should focus on existing users of grey hydrogen

There are two potential groups of buyers of green hydrogen: businesses that already use hydrogen, and businesses that would switch from methane. Each face different barriers.

Today, just 10 facilities in Australia use hydrogen, all of it grey and produced onsite, most of it used for ammonia production (see Figure 3.2). Collectively, they use 53 petajoules of hydrogen per year, about 440,000 tonnes – a similar volume to the federal government’s 2030 green hydrogen target (60 petajoules, 500,000 tonnes).73Two further facilities – the Kurri Kurri power station in the Hunter Valley and the Tallawarra B power station south of Sydney – are also hydrogen-ready (their equipment is capable of burning some share of hydrogen).

These businesses are the obvious place to look for early buyers of green hydrogen, because these facilities are already set up to use hydrogen. But to switch from producing grey to green hydrogen would still involve costly upgrades at each facility.

This is where production-side support should focus – switching these 10 existing hydrogen users to green by replacing their steam methane reformers with large electrolysers.

Currently, the cost of green hydrogen is about $63 per gigajoule versus approximately $12 per gigajoule for fossil methane.74Monaghan (2024). So production-side support should help to bridge that gap for these businesses. With a $50 per gigajoule cost gap, the two rounds of Hydrogen Headstart could unlock production of about 370,000 tonnes of hydrogen – enough to meet about 84 per cent of hydrogen demand for all current users of grey hydrogen in Australia for one year.75Based on $1.25 billion already allocated Hydrogen Headstart Round 1, and $1 billion allocated for Round 2.

At this scale, Headstart should support the small-scale facilities needed to scale up. Further rounds of Hydrogen Headstart may be required for larger entities later on, which could be funded by restructuring the Hydrogen Production Tax Incentive.76The hydrogen sector is not currently at sufficient scale to benefit from the tax credit. A tax credit benefits large, sophisticated businesses that are making profits.

Longer term, the federal government should ensure its broader industry policy settings support the use of hydrogen in industries where it is a viable replacement for coal and natural gas; such as iron-making and alumina refining.

This will require demand-side support, because the processes to refine ores will need to change to use hydrogen instead. These industries will also require much larger volumes – for example, maintaining current steel production using hydrogen would require around 50 petajoules of hydrogen annually. And they will also need integration with broader energy infrastructure development, because additional electricity will also be needed.

3.4 Biomethane needs production-side support to grow

Unlike green hydrogen, which is nascent globally, we have clear blueprints from overseas about how to scale up the use of biomethane. Several countries have successfully developed meaningful biomethane sectors through targeted policy. For example:

- Italy had essentially no biomethane industry in 2018. As of 2023, through feed-in tariffs and capital grants, it had about 133 biomethane plants, producing 28 petajoules a year, with substantial further growth planned by 2030.77Yarnold et al (2025).

- Denmark established a biomethane sector in 2014, and by 2024 produced about 27 petajoules per year, about 40 per cent of its total gas demand. Denmark deployed both production-side support (through feed-in tariffs) and demand-side support (through a biomethane blending obligation on gas providers).78ibid.

In Australia, though, early-stage technology support for biomethane has been almost non-existent. The Australian Renewable Energy Agency (ARENA) has supported just three biomethane projects with about $60 million in grants.79Malabar (Sydney), Delorean (Adelaide) and Wasleys (Adelaide). This should be accelerated: the federal government should ask ARENA and the Clean Energy Finance Corporation to drive development of demonstration and commercial pilot plants.

These investments should be expanded to cover more feedstocks, locations, and types of producers. The goal should be to establish replicable models for biomethane production.80There is no technology support needed on the demand side, because appliances and equipment that use fossil methane require no modifications to use biomethane.