Now comes the hard part of the great energy transition

by Richard Yan

Decarbonising the National Electricity Market (NEM) is key to decarbonising our economy. And a reliable, affordable, and clean energy system is the key to becoming a renewable energy superpower, a dream on which Australia’s governments are increasingly hanging our prospects. But troubled waters are ahead.

To the casual observer, the NEM seems fine. Carbon emissions have been falling, due primarily to renewable electricity policies that have delivered a renewables’ share of nearly 40 per cent. Power supply has generally been reliable, and prices have stabilised, albeit at an uncomfortably high level.

But now comes the hard part.

The federal government’s target of 82 per cent renewables by 2030 looks unachievable.

The NEM is operating closer to the reliability edge, more often. And new investments in energy infrastructure are not happening fast enough, despite repeated warnings of impending reliability issues.

Grattan Institute’s new report, Keeping the lights on: How Australia should navigate the era of coal closures and prepare for what comes next, identifies the problem and its causes, and plots a way forward for governments.

Governments can’t risk letting these reliability and affordability goals slip as the NEM transitions to low-carbon technologies. This is especially true for reliability. If the lights go out, governments could lose social licence for the energy transition.

So, what’s causing the reliability problem?

Renewables are intermittent. But that isn’t the cause. It is simply that not enough new electricity infrastructure of the right kind is being built in the right place and at the right time.

This is largely because of poor coordination. Timelines for closures of coal plants are being brought forward almost every year, while the build out of coal’s replacement – renewables, transmission, and storage – is being slowed down by bad planning, slow regulatory approvals, community opposition, and supply chain issues.

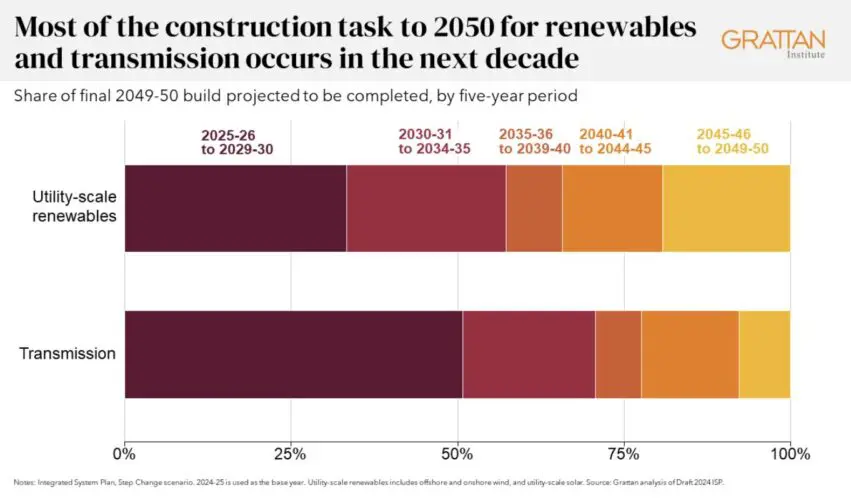

To put the scale of the problem in perspective, the Australian Energy Market Operator expects that about half of the new transmission and upgrades to existing transmission needed by 2050 needs to be built in the next six years.

Policies to encourage investment in renewables were successful as industry policy and in reducing emissions, but they are narrowly focused and no longer fit for the purpose of driving the transition.

The Renewable Energy Target supports renewables, but not other technologies that could displace coal while ensuring reliability at low cost. This includes storage and gas, the latter being valuable for both its dispatchable capacity and as a backup during renewables droughts.

Individual governments have recognised these issues and are taking matters into their own hands, from the federal government’s Capacity Investment Scheme to Victoria’s reincarnated State Electricity Commission and NSW’s EnergyCo, and secret negotiations with coal plants to extend their lives.

Some of these policies are probably helping. But some interventions are ad hoc and may make the problem worse by creating investor uncertainty. And they are certainly not coordinated.

Here’s how governments can chart a path through this energy policy minefield.

They should treat the problem ahead as being made up of two distinct eras: the coal closure era and the post-coal era. These eras have different characteristics and problems, which means they require different solutions.

The coal closure era will be messy, with reliability being the main concern. The task is to keep the lights on, and emissions coming down, with the tools available. During this period, major market reform isn’t the way to fix the immediate reliability issue. Instead, make tweaks and impose short-term fixes to manage existing and emerging risks.

Governments underwriting investment will be a feature of this era. Further ‘insurance’ deals with coal plants may make sense until adequate replacement capacity is connected, but these should be transparent to the market and avoid shifting excessive risk to taxpayers. Faster replacement capacity will require practical changes to lower the barriers to investment, approvals, and building. The solutions will be different in different jurisdictions.

Once the coal is gone, large lapses in reliability will be less of an issue. The task then becomes to create a clean and reliable NEM to meet the growing electricity demands from electrification of parts of the existing gas and transport sectors.

The NEM will look very different to what it does now. The physical system will be dominated by widely distributed solar and wind generation, connected by more transmission, and backed up by gas and short- and long-term storage.

The post-coal era will be here in less than 10 years. Planning for this future needs to start now.

The first and fundamental step will be for governments to agree on the respective roles of the market and governments in a net-zero electricity system.

Three priorities follow. The first is to design a market structure that will help ensure adequate energy resources in a high-renewables system. The second is to signal the introduction of an enduring carbon price, explicit or implicit, for the energy sector, to guide future investments and gas plant closures.

And the third is to better integrate and coordinate wind and solar farms, and so-called distributed energy resources, such as, rooftop solar and batteries.

The next few years will be messy. But it’s worth accepting that, while planning the major reforms that are crucial for a successful future NEM. This way, we can keep the lights on while also lighting the way to a prosperous green energy future.