Summary

Each year, community pharmacies dispense millions of scripts, give millions of vaccinations, and offer expert advice to most Australians, costing the federal government and patients almost $4 billion a year.

Pharmacy policy is too important to be controlled by a powerful lobby group. But the Pharmacy Guild of Australia, which represents most pharmacy owners, is calling the shots.

The Guild negotiates funding and policy directly with the federal government. Unlike almost any other country, Australia’s negotiations include no one else, and are based on almost no public evidence.

Bad governance has led to bad deals – unless you own a pharmacy. Profits have surged, while patients miss out on cheaper medicines and choices about where to get them, and taxpayers pay too much.

Dispensing fees are probably too high, and some payments aren’t justified at all. If the number of scripts falls below a predicted level, government has to pay up anyway, as if the predicted level was met.

Unique regulatory protections dictate who can own pharmacies and where they can be set up. For most scripts, discounts are being banned or discouraged by financial penalties. Meanwhile, a discretionary surcharge is allowed on many scripts. All these rules choke off competition that would improve choice, increase opening hours, and cut prices.

Skilled and trusted pharmacists should provide more types of care. But medicine checks and dose administration aids are poorly targeted or overpriced, prompting blunt caps on their growth. For new services, dozens of trials have been too weak to prove they are cost-effective, leaving the sector in a purgatory of fragmented state programs.

Pharmacy policy is a shakedown that needs a shakeup. Five reforms can get better value for patients and taxpayers.

First, no more backroom deals. Negotiations should be replaced by independent decisions, as happens for other types of healthcare.

If the federal government won’t do that, at a minimum patients and pharmacists should be at the table, and there should be clear public evidence to justify decisions.

Second, dispensing fees should be streamlined and reset. Unjustified fees should be scrapped. Fees should be set independently, based on cost not bargaining. A fee for stocking high-cost medicines should be redesigned to work better, and save up to $285 million a year.

Third, rules on pharmacy location and ownership should be removed immediately, and restrictions on discounts should be phased out.

Fourth, services must deliver value for money. The criteria for MedsChecks should be tighter and administration aids should be repriced. Pharmacists should be able to prescribe for urinary tract infection, but other services must wait for decisive evidence from national trials on the most cost-effective options.

Finally, the federal government should fund pharmacists in GP clinics, where evidence shows that their expertise can improve care.

Fairer fees and competition will change the sector. Some pharmacies may struggle, especially in rural areas. Some companies could dominate and raise prices or cut quality. But safeguards can prevent these risks: targeted financial support, scrutiny from the competition watchdog, and a better system to measure pharmacy quality.

Replacing bargaining with evidence, and protectionism with competition, will give patients lower prices and more choice, and taxpayers better value, while keeping pharmacies the accessible and trusted service Australians rely on.

Recommendations

Recommendation 1

Restore independent community pharmacy policy

- End Community Pharmacy Agreements.

- If the federal government will not do this, include pharmacists and patients in the agreements, and base them on public evidence.

Recommendation 2

Make dispensing fees simpler and fairer

- Expand and speed up price disclosure price cuts.

- Pay pharmacies sooner for very high-cost medicines.

- Automate the Safety Net recording process.

- Remove unjustified fees: the Safety Net recording fee, discretionary patient charges, and fees for 60-day dispensing.

Recommendation 3

Base pharmacy funding on cost and reasonable profits

- Make the Independent Health and Aged Care Pricing Authority (IHACPA) responsible for determining pharmacy remuneration, with pharmacies required to provide necessary data.

- Replace payment adjustment and the regional allowance with monitoring of pharmacy viability, targeted support, and reverse auctions in areas without a pharmacy.

Recommendation 4

End unfair protections and unleash competition

- Remove restrictions on where new pharmacies can be established, including allowing pharmacies in supermarkets.

- Remove restrictions on who can own pharmacies and how many they can own.

- Allow pharmacies to discount all medicines.

Recommendation 5

Safeguard competition and quality

- Direct the ACCC to do a market study of the community pharmacy sector and design appropriate safeguards to protect competition.

- Implement an independent quality and outcomes monitoring framework.

Recommendation 6

Ensure pharmacy services are good value

- Replace arbitrary caps on MedsChecks with tighter eligibility and information-sharing requirements.

- Reset pricing for dose administration aids to reflect increas-ing automation, and then remove caps.

- Fund pharmacist prescribing for urinary tract infections. Fund rigorous national trials of prescribing for other minor ailments, smoking cessation, and collaborative chronic disease management.

- Invest $80 million in pharmacists in general practice and Aboriginal Community Controlled Health Organisations.

1 Essential services are being held hostage

Community pharmacies perform vital services for Australians – dispensing medicines, advising patients, and providing one of the most accessible touchpoints in the health system. Governments and patients spend billions of dollars every year for these services, and they deserve good value.

But for decades, the Pharmacy Guild of Australia – one of the country’s most powerful lobby groups – has shaped pharmacy policy to protect the interests of pharmacy owners, blocking reforms that would deliver better value to taxpayers and patients.

1.1 Pharmacies are a critical part of our health system

The government subsidises prescription medicines and pays pharmacists – the main health professionals in Australia allowed to dispense medicines – to supply them to patients and provide advice.1Approved doctors practising in isolated areas without access to a pharmacy are also allowed to dispense medicines: Department of Health, Disability, and Ageing (2024a). Pharmacies are essential to access to and safe use of prescription medicines.

In 2024-25, there were more than 6,000 community pharmacies in Australia, and they dispensed 335 million prescriptions under the Pharmaceutical Benefits Scheme (PBS) and Repatriation PBS (a dedicated scheme for veterans).2Department of Health, Disability, and Ageing (2026a, Tables 2a, 2c and 13). Community pharmacy refers to any pharmacy that dispenses medicines to the general public. It does not refer to a specific kind of ownership or operating model. The other kind of pharmacies are hospital pharmacies, which dispense medicines to patients in hospital. In this report we refer to the PBS and RPBS together as the PBS. Community pharmacies provide the most common touchpoint that people have with the healthcare system.

On average, each Australian visits a community pharmacy 18 times a year.3See Pharmaceutical Society of Australia (2024). By comparison, Australians visit a GP on average six times a year: AIHW (2026a).

Pharmacists are highly skilled health professionals with expert knowledge of medicines. In the community setting, they dispense medicines, counsel patients on how to take them safely, and flag medicine interactions and prescribing errors. They also provide informal health advice and increasingly deliver clinical services, such as vaccinations.

Community pharmacists are among the most accessible health professionals in Australia, and patients can seek their advice without an appointment.

Each year, pharmacies receive about $3.8 billion for dispensing medicines and professional services.4This figure includes total spending on pharmacy remuneration and professional programs in 2025 dollars: Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024, Table 19). See Chapter 4 and Chapter 8 for more detail. Taxpayers and patients need to be confident they are getting good service, and good value, from this spending.

1.2 Pharmacy policy is dominated by the Guild

The Pharmacy Guild of Australia (the Guild) is the peak body representing community pharmacy owners (Box 1). It is also one of the most powerful lobby groups in the country.

Its political influence is partly financial, thanks to its significant political donations to successive governments on both sides of politics.5Grattan analysis of AEC (2026). See Box 1.

Box 1: The Pharmacy Guild of Australia

Established in 1927, the Pharmacy Guild is the peak body representing community pharmacy owners in Australia. In 2023, it had 4,154 member pharmacies – about 70 per cent of community pharmacies.aDepartment of Health, Disability, and Ageing (2024b, p. 5). It doesn’t include any Chemist Warehouse stores, which together account for about 9 per cent of all pharmacies and probably a larger share of the market.bDepartment of Health, Disability, and Ageing (ibid, p. 5), ACCC (2024, Table 1).

The Guild and Chemist Warehouse disagree on key pharmacy policies, including location rules and discounting restrictions: Gance (2017). The Guild is also a powerful lobby group. In the past five years, it has donated $2.5 million to political parties.cFigure includes donations from 2020-21 to 2024-25 and has been inflated to March 2026 dollars using the Consumer Price Index: AEC (2026). This makes it the largest donor from the healthcare sector over that period, and the 15th largest overall – larger than the Minerals Council of Australia.dGrattan analysis of AEC (ibid). Over that same period, the Minerals Council donated $2.2 million (March 2026 dollars). Over the past four years, the Guild has also spent $16.3 million on public campaigns.eFigure includes spending from 2021-22 to 2024-25 and has been inflated to March 2026 dollars using the Consumer Price Index: Pharmacy Guild of Australia (2025a) and Pharmacy Guild of Australia (2023a).

This political spending is funded in part by membership fees, and in part by the Guild’s wholly owned insurance and professional services firm. This firm – Guild Group – has generated $71 million in profits and has paid $51 million in dividends to the Guild over the past three years.fFigures have been inflated to March 2026 dollars using the Consumer Price Index: Guild Group (2025, p. 9), Guild Group (2024, p. 9), Pharmacy Guild of Australia (2025a, p. 34), and Pharmacy Guild of Australia (2023a, p. 34).

But the main source of the Guild’s power is its ability and willingness to weaponise a highly valued part of the healthcare system. Pharmacists are among the most trusted professionals in Australia.6In a survey of 1,267 Australians, 76 per cent rated pharmacists ‘high’ or ‘very high’ for their ‘ethics and honesty’, behind only nurses and doctors: Roy Morgan (2021, p. 2). The Guild has repeatedly leveraged this trust to mobilise patients against reforms that would, in many cases, benefit patients directly. This generally involves claiming that any such reform would put their local pharmacy out of business.

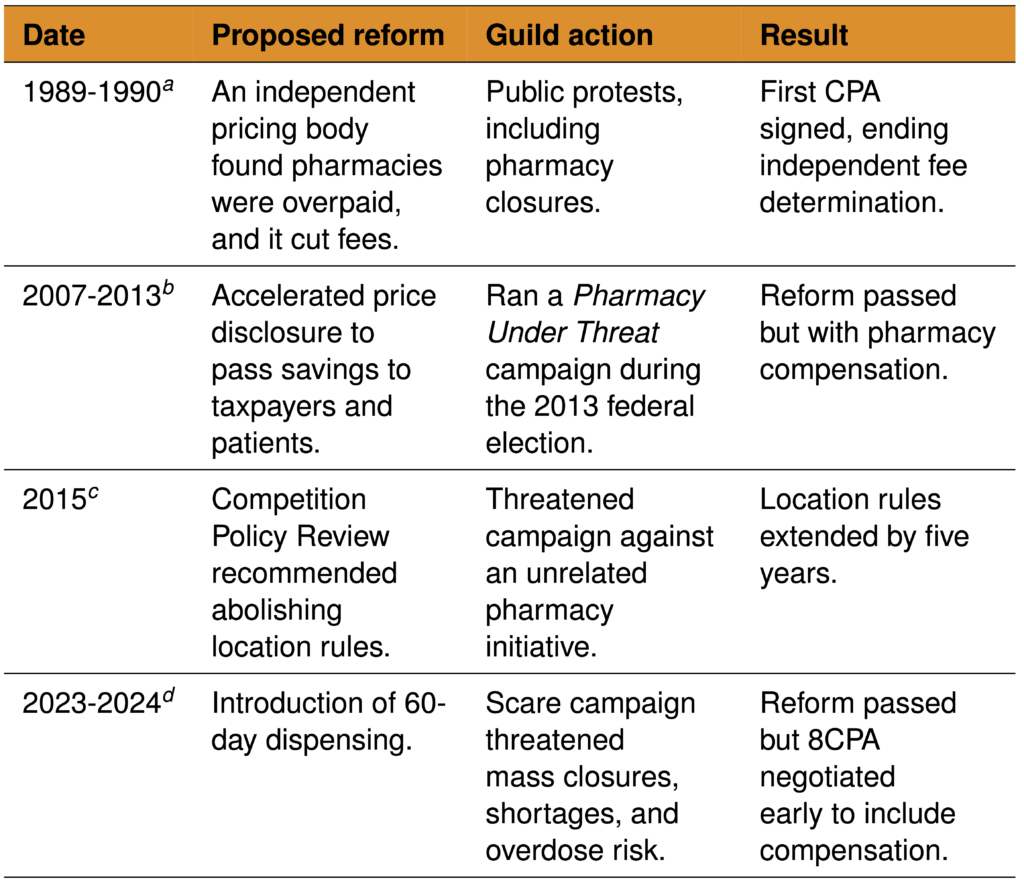

Table 1.1 summarises instances when the Guild has successfully blocked or watered down reform over the past three decades. Box 2 provides more detail on the most recent example: the scare campaign against 60-day dispensing.

Table 1.1: The Guild has a track record of blocking reform

Notes: CPA = Community Pharmacy Agreement.

a. Department of Health, Disability, and Ageing (2024b, p. 6).

b. See McInerney (2013), Clarke (2015), and ANAO (2015). To compensate pharmacies, the sixth Community Pharmacy Agreement partially delinked pharmacy fees from medicine prices: Ley (2015).

c. See Recommendation 14 of Harper et al (2015). The Guild threatened to launch a campaign against the proposal to allow pharmacies to discount over co-payment PBS medicines by $1 and only pulled back when the location rules were extended: Hurst (2015).

d. See Box 2.

The Guild has ensured that the evidence base needed to challenge its claims does not exist. Its ongoing refusal to provide pharmacy cost data has meant that no comprehensive costing study has been conducted since 1989 – almost four decades ago.7In 1989, the Pharmaceutical Benefits Remuneration Tribunal (PBRT) evaluated pharmacy cost data: ANAO (2015, p. 25). During the 2017 Review of Community Pharmacy Remuneration and Regulation (the King Review) – which the Guild agreed to support – it discouraged members from participating in a financial survey, citing methodological concerns: King et al (2017a, pp. 70-71) and Pharmacy Guild of Australia (2017a, p. 5). Today, the Guild requires researchers to obtain its endorsement before members are advised to participate in any research: Pharmacy Guild of Australia (n.d.[a]). Without cost data being public, the Guild can maintain the impression that the sector is perpetually on a knife’s edge, making claims of catastrophic harm from reform impossible to test or refute.

Box 2: The 60-day dispensing scare campaign

Most medicines in Australia are dispensed for 30 days at a time. But in April 2023, Health Minister Mark Butler announced that more than 300 medicines for stable, chronic conditions would become eligible for 60-day dispensing, to be rolled out in stages from later that year.aButler (2023a).

This change would lead to significant savings for patients – halving the dispensing fees for these medicines – and bring Australia in line with countries including New Zealand, the UK, France, and Canada that had already offered 60- or 90-day dispensing.bButler (2023b) and Af Geijerstam et al (2024).

The Guild opposed the change. Pharmacies would earn less from dispensing and lose retail revenue from reduced foot traffic. The Guild claimed this would result in mass pharmacy closures, commissioning modelling that projected up to 665 would shut within four years.cErgas (2023, Table E-3). This modelling used government uptake projections only for its minimum scenario. The central scenario – from which headline findings were drawn – and the maximum scenario both assumed uptake 24-to-78 per cent higher than government projections in each year: Ergas (2023, Table 4-1) and Department of Health, Disability, and Ageing (2023a, p. 26). As it turned out, even the government’s assumptions were too high: Breadon and Hu (2025).

The Guild warned of medicine shortages, with president Trent Twomey declaring he didn’t want to see ‘a Hunger Games stand-off in any community in Australia where some patients get double the medicine they need, while others get nothing’.dPharmacy Guild of Australia (2023b). It also argued that larger medicine quantities in homes would increase the risk of accidental overdose by children. Both claims were widely disputed, and there are no reports of such problems in countries with 60- or 90-day dispensing.eButler (2023c), RMIT ABC Fact Check (2023), and Af Geijerstam et al (2024).

Through billboards, television, radio, social media, phone calls, and encouraging direct conversations at the counter, the Guild tried to convince Australians that their local pharmacy would close and they would lose access to their medicines.fChrysanthos (2023), McKenzie (2023), and Scholefield (2023).

The government held firm. Stage one proceeded in September 2023. The Guild suspended its campaign soon after, having secured an agreement to bring forward negotiations for the eighth Community Pharmacy Agreement. That agreement began in July 2024 – a year earlier than planned – and included new payments that excessively compensate pharmacies for lost dispensing revenue (see Chapter 3).

In December 2024, stakeholders who opposed the Guild reportedly received a Christmas package from the Guild: a voodoo doll of Trent Twomey, some pins, and a packet of Glucogel jelly beans.gAs reported in The Australian Financial Review: Robin (2024).

There have been no reports of medicine shortages or overdoses from 60-day dispensing.hOne year after implementation, Payne (2024) found no evidence of negative outcomes, though analysis was constrained by data limitations. Meanwhile, the reform has delivered huge savings: in 2025 alone, patients saved $222 million and the government $252 million.iGrattan analysis using the methodology outlined in Breadon and Hu (2025), for medicines in stage 1, 2, and 3 of the 60-day dispensing rollout.

1.3 Pharmacies seem to be getting a sweet deal

Thanks to its decades of political influence, the Guild has secured the best of both worlds. Pharmacies earn growing profits while guaranteed government income insulates them from revenue declines. In effect, they profit as private businesses while shifting financial risk to taxpayers.

Pharmacy income extends well beyond PBS dispensing. Retail and over-the-counter medicine sales comprise about 30 per cent of the average Guild pharmacy’s revenue, rising to about 67 per cent for Chemist Warehouse stores.8Pharmacy Guild of Australia (2026a, Table 1) and Sigma Healthcare (2023, p. 22).

Pharmacies also earn revenue from private prescriptions. These are medicines not listed on the PBS for which patients pay the full cost with no government subsidy.9Department of Health, Disability, and Ageing (2024c). Unlike PBS prices, private prescription prices are entirely unregulated, meaning pharmacists can charge whatever they like. Two categories of medicine have turbocharged this revenue stream in recent years (Box 3).

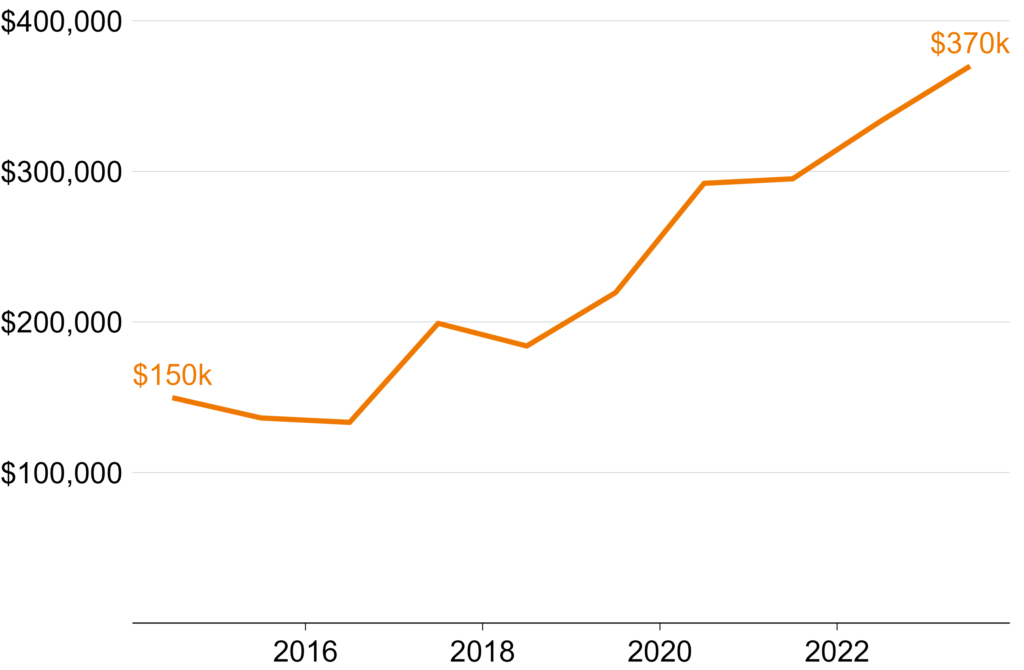

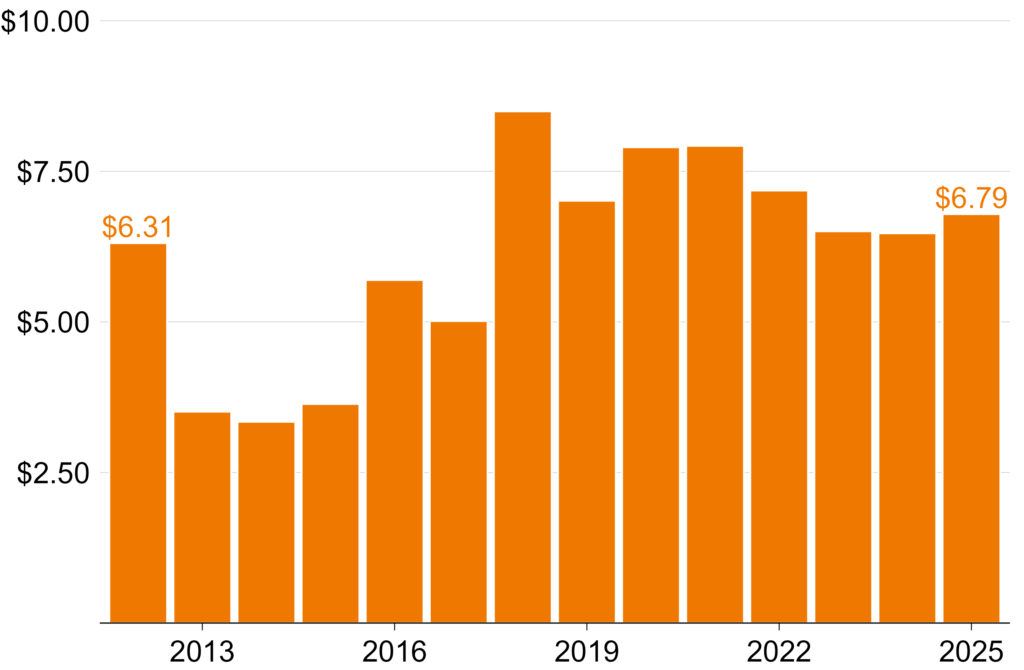

The available evidence on pharmacy finances – limited as it is – suggests a highly profitable sector. Guild survey data suggest that average pharmacy profits have more than doubled over the past decade (Figure 1.1). This excludes Chemist Warehouse stores, but their rich valuation and surging sales suggest they’re not struggling either.10Smith (2025) and Sigma Healthcare (2025, p. 4).

Pharmacy discounting could also be a sign of profitability. Pharmacies often discount medicines to win customers, surrendering 17 per cent of their remuneration on average (see Chapter 6).11Grattan analysis of Department of Health, Disability, and Ageing (2026b) and Department of Health, Disability, and Ageing (2026c). Pharmacies may offer discounts to attract patients who then spend more on retail goods.

Figure 1.1: Pharmacy profit is increasing

Average profit (before tax) of Australian community pharmacies, adjusted for inflation

Notes: Net profit is total revenue minus total expenses, cost of goods sold, and notional proprietor’s salary. Data from the Guild Digest, an annual survey of 300-to-600 pharmacies that is weighted to represent the Australian community pharmacy sector. Years refer to financial year (e.g. 2023-24 is shown as 2024). Values have been inflated to March 2026 dollars using Consumer Price Index: ABS (2026a). Sources: 2015 to 2025 Guild Digests, available at Pharmacy Guild of Australia (n.d.[b]).

1.4 What this report is about

It’s clear that pharmacies are receiving substantial government funding and generating substantial profits. The combination of rising profits, opacity, and regulatory capture warrants scrutiny.

The following chapters identify the many policies that benefit pharmacy owners at the expense of patients and taxpayers, and how to fix them:

- An exclusive negotiating position to set policy and funding (Chapter 2)

- Payments with no public justification for their structure or value (Chapter 3 and Chapter 4)

- Unparalleled protection from competition through pharmacy ownership and location rules (Chapter 5)

- Restrictions on discounting that increase costs for patients (Chapter 6)

- Minimal monitoring and reporting of quality, efficiency, or results (Chapter 7)

- Funding for pharmacy services that haven’t shown good value-for-money (Chapter 8)

This report does not cover the development, manufacture, or wholesale distribution of medicines in Australia, or the level and structure of patient payments or Safety Net thresholds.

Box 3: Private prescriptions are a lucrative revenue stream

Two types of medicine have boosted revenue from private prescriptions in recent years.aNote that some of these scripts were probably dispensed online rather than through traditional pharmacies.

Glucagon-like peptide-1 receptor agonists (GLP-1 RAs) – such as Ozempic and Mounjaro – are used to treat type 2 diabetes and obesity. Since May 2020, total sales have increased almost 10-fold, with most of the growth in private prescriptions.bIn April 2025, 43.8 per cent of prescriptions were private: Falster et al (2025).

In the 12 months to April 2025, an estimated 2.9 million private prescriptions for GLP-1 RAs were accessed.cThis only includes GLP-1 RAs listed for type 2 diabetes. The true number of private GLP-1 RA prescriptions was probably higher: Falster et al (ibid). Based on current Chemist Warehouse prices, this represents about $83 million in pharmacy remuneration per year.dAs of July 2026, Chemist Warehouse charged $144.99 for a 1.34mg/mL 3mL pre-filled Ozempic pen: Chemist Warehouse (2026). On the PBS, the medicine and wholesale costs are $116.23, meaning $28.76 of pharmacy remuneration: Department of Health, Disability, and Ageing (2026b). The figure is conservative, because non-discount pharmacies probably charge even more.

Medicinal cannabis prescriptions are also increasing. In 2025, 6.35 million units were dispensed in Australia, almost entirely as private scripts.eSee Penington Institute (2026, p. 3). Only cannabidiol, used to treat a rare form of epilepsy, is available on the PBS: Healthdirect Australia (2026). There were only 7,000 prescriptions for cannabidiol dispensed in 2025: Department of Health, Disability, and Ageing (2026c). If pharmacies charged only the standard current PBS dispensing fee, this would represent an additional $91 million to pharmacies each year. Again, the true figure is probably higher.

2 Restore independent pharmacy policy

Community pharmacies are funded and regulated through Community Pharmacy Agreements, which are negotiated between the federal government and the Guild. This arrangement has its roots not in policy design, but in a political crisis. The result is a process that is sheltered from outside scrutiny, dominated by a single interest group, and unlike any other major health funding arrangement in Australia.

The Community Pharmacy Agreement should be abolished and replaced with the more transparent, evidence-based alternatives proposed in this report. If the government won’t do that, agreements should be based on public evidence, and negotiated with pharmacists and patients – not just pharmacy owners.

2.1 What is the Community Pharmacy Agreement?

Since 1990, the federal government has negotiated a series of five-year agreements with the pharmacy sector – Community Pharmacy Agreements – to govern how community pharmacies are funded and regulated. There have been eight agreements to date.12The eighth Community Pharmacy Agreement came into effect on 1 July 2024 and will run until 30 June 2029, after which the ninth Community Pharmacy Agreement is expected to supersede it. See Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024). The sector is represented by the Guild (see Box 1).13Section 98BAA of the National Health Act requires that the Community Pharmacy Agreement be with an organisation representing the majority of community pharmacy owners.

Community Pharmacy Agreements are expensive. The current agreement is expected to cost $25.8 billion over its five-year term.14Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024).

2.2 The Agreement emerged from a political standoff, not a policy process

Before the first Community Pharmacy Agreement, in 1990, the sector looked very different. Pharmacy remuneration was determined independently by the Pharmaceutical Benefits Remuneration Tribunal (PBRT).15The PBRT was established in 1981 to insulate funding decisions from political pressure: ANAO (2015, Table 1.1).

Under this model, dispensing fees per script fell as the number of scripts dispensed by a pharmacy rose, which rewarded small, inefficient pharmacies. As a result, Australia had a high number of pharmacies by international standards, with many clustered together in urban areas.16Department of Health (2014, p. 6).

This was the case until 1989, when the PBRT concluded – based on surveys of dispensing costs – that pharmacies were being overpaid, and it moved to cut fees sharply.17The PBRT decided to abolish an existing 25 per cent mark-up and reduce the dispensing fee by 23 per cent: Department of Health, Disability, and Ageing (2024b, p. 6). Pharmacists responded by holding public rallies, with some owners closing their pharmacies in protest.18Ibid. The then Health Minister intervened by negotiating directly with the Guild and bypassing the PBRT entirely.19Ibid (p. 6).

The result was the first Community Pharmacy Agreement, signed in 1990. It replaced the old funding structure with one that no longer gave higher funding per script to lower-volume pharmacies, introduced location rules restricting where new pharmacies could open, and funded pharmacy buy-outs and mergers.20Department of Community Services and Health (1990).

While the PBRT still exists, its only remaining roles are to give legal effect to the terms of the Community Pharmacy Agreement, and to step in and set remuneration if the parties fail to reach a deal.21Section 98B of the National Health Act.

The precedent set by the first Community Pharmacy Agreement – a bilateral negotiation where politics pushed aside evidence – still haunts Australia today.

2.3 The Community Pharmacy Agreement is uniquely opaque and unrepresentative

The Community Pharmacy Agreement is determined through a process that is sheltered from outside scrutiny and dominated by a single interest group. No other major health funding arrangement in Australia works this way. Even compared to other countries with negotiated pharmacy agreements, Australia’s stands out for its lack of transparency and representativeness.

2.3.1 The negotiation is a black box

The terms of each Community Pharmacy Agreement are determined through months of closed-door negotiations.22For example, in the lead-up to the fifth agreement being signed, the Department of Health conducted dozens of meetings with the Guild – face to face, by email, phone, and teleconference – over more than six months: ANAO (2015, pp. 61, 83). There is no public documentation of the process and no empirical justification provided for the policies and spending agreed.23A 2015 Australian National Audit Office audit of the fifth Community Pharmacy Agreement is the most detailed public account available, but it revealed minimal detail on the negotiation process: ANAO (ibid). For an agreement governing billions of dollars of public spending, this is a remarkably low level of transparency.

It hasn’t gone unnoticed. The Consumers Health Forum of Australia, the Pharmaceutical Society of Australia,24The peak body for the pharmacy workforce. and other stakeholders not party to negotiations have repeatedly raised concerns.25See Jackson et al (2023a, p. 8) and King et al (2017b, p. 81). Improved transparency was also recommended by the 2017 Review of Community Pharmacy Remuneration and Regulation (the King Review).26Recommendations 5.4 and 6.3: King et al (ibid).

2.3.2 The right people aren’t at the table

Since the first Community Pharmacy Agreement, negotiations have taken place solely between the government and the Guild. The Guild represents most pharmacy owners, but not the pharmacists who work in pharmacies or the patients who rely on them.

This is a significant gap. Many stakeholders – including some pharmacists – say they are dissatisfied with the arrangement, and question the Guild’s ability to represent their interests.27Jackson et al (2023a) found broad dissatisfaction with the representativeness of negotiations. One pharmacist said: ‘Having the [Community Pharmacy Agreement] negotiated by a small group of owners with a vested interest is quite insulting, and quite inappropriate. They have a vested interest in achieving commercial prosperity.’ This is unsurprising: the interests of pharmacy owners do not always align with the priorities of employed pharmacists, let alone patients.

The King Review recommended that the Pharmaceutical Society of Australia and the Consumers Health Forum of Australia be included as equal participants in negotiations.28Recommendation 8.4 of King et al (2017b). Chemist Warehouse has argued that this expanded signatory list would not adequately represent their interests as the largest banner group because they are not members of the Guild: Gance (2017). For the past three agreements, stakeholder groups have had some formal participation in the lead-up to negotiations and in overseeing their implementation.29This has consisted of stakeholder consultations and, for select groups, positions on oversight committees: Department of Health, Disability, and Ageing (2025a), Department of Health (2022), and Department of Health, Disability, and Ageing (2019). But some stakeholders reported consultations were inadequate and had little meaningful impact: Jackson et al (2023a, p. 8). But this has not extended to the negotiations themselves. Apart from the Pharmaceutical Society of Australia – which was a signatory to a small professional services section of the seventh agreement – no one but the Guild and the Department has ever had a formal seat at the table.30Department of Health and Pharmacy Guild of Australia (2020) and Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024).

2.3.3 Australian community pharmacy is an outlier

The Community Pharmacy Agreement is the only agreement of its kind for Australian healthcare services.31A partial exception is the Pharmaceutical Wholesaler Agreement. This was previously included in the Community Pharmacy Agreement but has since been separated into its own agreement that suffers from many of the same shortcomings: Department of Health, Disability, and Ageing and National Pharmaceutical Services Association (2024).

GP, specialist, optometry, and allied health rebates are set through the Medicare Benefits Schedule by the government, with new items added on the recommendation of the independent Medicare Services Advisory Committee.32Department of Health, Disability, and Ageing (2024d). Public hospital prices are set by an independent pricing authority, and calculated using cost data.33IHACPA (n.d.). Bilateral funding agreements with other health sectors – for example, for pathology and diagnostic imaging – have not been continued.34Pathology Funding Agreements (1996 to 2016) and Memoranda of Understanding with the diagnostic imaging sector (1998 to 2008) set negotiated spending targets, while individual services were paid for through fee-for-service Medicare payments: Jackson et al (2023b), Duckett and Romanes (2016), and ANAO (2014).

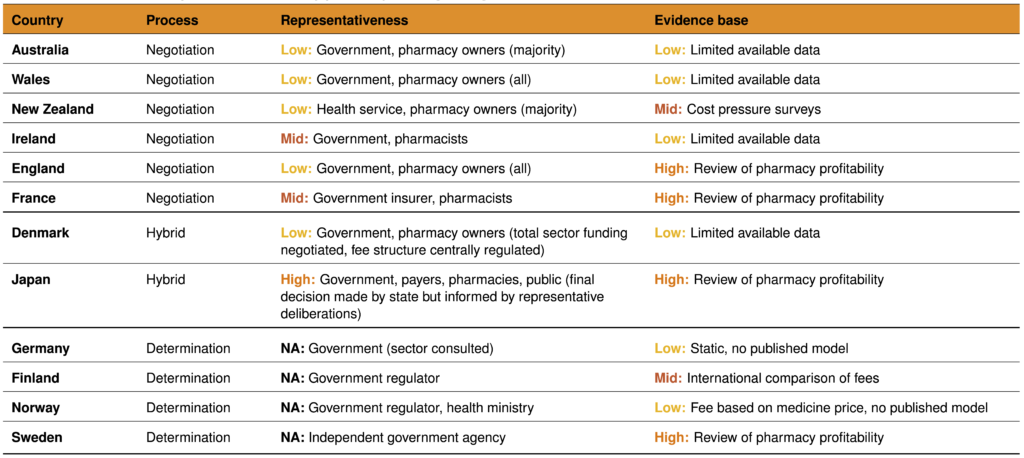

Table 2.1 rates pharmacy funding arrangements in comparable countries on three dimensions: the representativeness of the stakeholders in the negotiating room, the level of evidence they use to make their decisions, and how well their decisions are explained to the public.

Some other countries use sector-level negotiations to set pharmacy funding, but even among those, Australia stands out. No other jurisdiction combines such a narrow negotiating group with such a complete absence of public evidence and transparency. Wales comes close, but even there, all pharmacy owners are represented – not just a majority.

Table 2.1: International comparison of community pharmacy funding arrangements

Notes: Representativeness = the degree to which decision-makers reflect the interests of those affected by their decisions. Evidence base = the amount and quality of evidence used to inform decisions.

Sources: Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024), Community Pharmacy Wales (2025), Health New Zealand | Te Whatu Ora (2025a), Grant Thornton (2021), Department of Health Ireland (2025), Community Pharmacy England (2024), Fédération des Pharmaciens de France (2023), Andersen and Skov-Johansen (2024), Hansen et al (2021), Health and Global Policy Institute (n.d.), Health and Global Policy Institute (2019), Federal Union of German Associations of Pharmacists (ABDA) (2025), Sosiaali- ja terveysministeriö (2020), Apotekforengingen (2024), and Tandvårds- & läkemedelsförmånsverket TLV (n.d.).

2.4 This Community Pharmacy Agreement should be the last

The key functions of the Community Pharmacy Agreement should be replaced with more transparent, evidence-based alternatives. Pharmacy remuneration should be set by an independent body (see Chapters 3 and 4), and funding for other community pharmacy services should be determined through a separate process (see Chapter 8).

That leaves little for Community Pharmacy Agreements to do, and no reason for them to continue. The current agreement should be the last.

If the agreements are retained, they should at least be reformed:

- Include the Pharmaceutical Society of Australia, the Consumers Health Forum of Australia, and other pharmacy owners

- Base decisions on cost data released before negotiations

- Document the decision-making process and make outcomes subject to ongoing quality monitoring and reporting

The Guild will probably oppose the recommendations in this report. It is likely to claim, as it has before, that reform threatens the viability of the sector and the communities that depend on it. The best response to these arguments is transparency, so that taxpayers and patients can know if these claims are accurate.

3 Make dispensing fees simpler and fairer

Community pharmacies exist, first and foremost, to dispense medicines. For PBS medicines, the cost of dispensing is shared between patients and the government. Many fees that add to that cost are poorly designed, and some are completely unjustified. Fixing these issues would deliver better value for taxpayers, cut patient fees, and support the delivery of high-cost medicines.

This chapter outlines how to address these structural flaws, and Chapter 4 covers how the value of the fees should be set.

3.1 How dispensing is funded

Community pharmacies receive a series of payments for dispensing PBS medicines, each ostensibly covering a different cost. The fees are paid by the government, the patient, or both. The following sections explain each component.

3.1.1 The Commonwealth Price

When a pharmacy dispenses a medicine, the total amount they receive in return is called the Commonwealth Price.35The Commonwealth Price is intended to cover the costs of dispensing PBS medicines, not any other pharmacy operations. The Commonwealth Price has four components:36Department of Health, Disability, and Ageing (2026d).

- Medicine costs – The approved ex-manufacturer price and wholesale mark-up ($0.24 to $223 depending on medicine price) reimburse the pharmacy for the price it has already paid to the manufacturer and wholesaler.

- Handling and infrastructure – The administration, handling, and infrastructure fee ($5.12 to $100.12 depending on medicine price) covers the costs of storing and handling the medicine and maintaining the required pharmacy infrastructure.

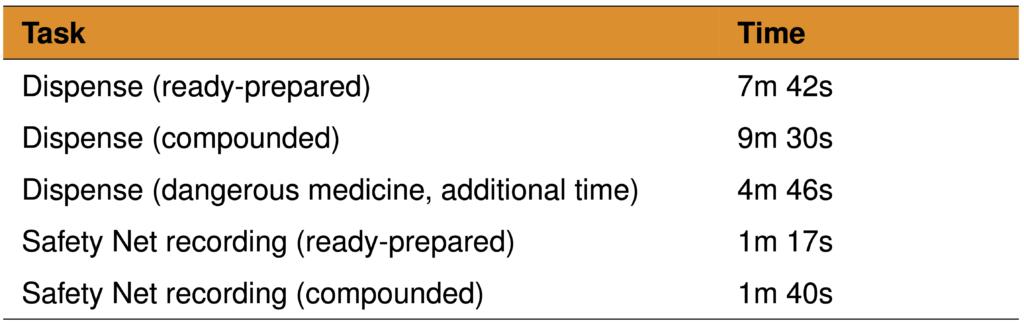

- Dispensing services – The dispensing fee ($9.24 for ready-prepared medicines, $11.28 for compounded medicines) covers dispensing – from receiving the prescription, verifying and preparing the medicine, to counselling the patient and handing it over.

- Other – Fees that vary by medicine type, patient circumstances, and pharmacist discretion, including the dangerous medicine fee ($5.73), Safety Net recording fee ($1.54 for ready-prepared medicines, $1.99 for compounded medicines), and allowable additional patient charge (up to $2.79).

The exact values of these payments are listed in Table A.1 in Appendix A.

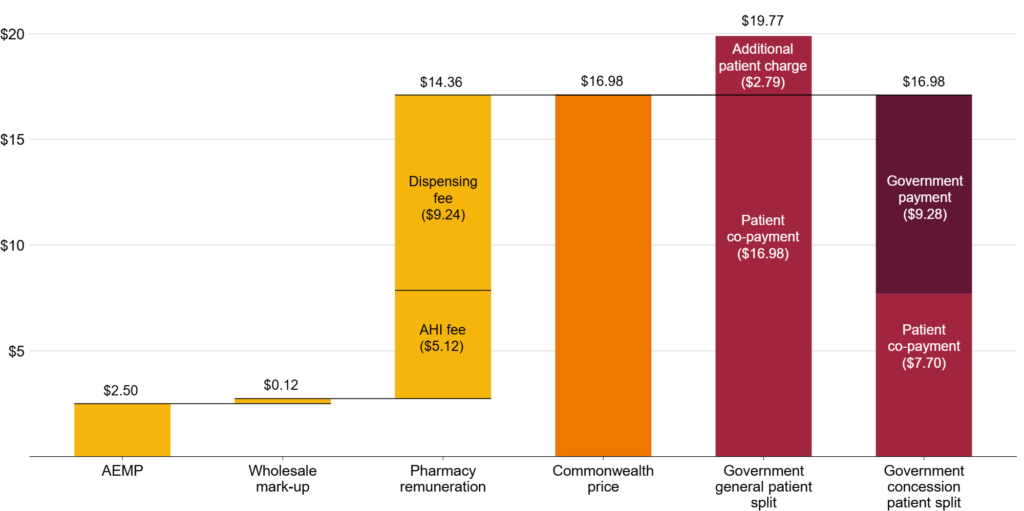

The Commonwealth Price is split between the patient and the government, with patients paying up to the maximum co-payment ($25 for general patients and $7.70 for concession patients) and the government paying the rest.37On top of the maximum co-payment, patients may pay after-hours fees, brand or therapeutic group premiums, or special patient contributions: Department of Health, Disability, and Ageing (ibid). Figure 3.1 provides an illustrative example using atorvastatin – a common, low-cost medicine for high cholesterol – of how this payment is split.

Figure 3.1: Patients and the government split the cost of dispensing

Cost components of the Commonwealth Price of atorvastatin 10mg (pack of 30), July 2026

Notes: Atorvastatin 10mg (pack of 30) has the PBS item number 8213G. AEMP = Approved ex-manufacturer price. AHI = Administration, handling, and infrastructure. The full allowable additional patient charge ($2.79) has been applied to the general patient fee here, but pharmacists may choose to apply part or none of this charge, provided the total patient cost does not exceed the general patient co-payment of $25. No Safety Net recording fee or after-hours fees have been included. Atorvastatin does not attract any brand or therapeutic group premiums.

Sources: Department of Health, Disability, and Ageing (2026d) and Department of Health, Disability, and Ageing (2026b).

3.1.2 Additional funding for 60-day dispensing

The current Community Pharmacy Agreement introduced the Additional Community Supply Support payments to compensate pharmacies for income lost due to 60-day dispensing (see Box 2).38Payments apply to over co-payment Section 85 medicines: Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024, p. 13) and Department of Health, Disability, and Ageing (2026e). Section 85 medicines cover most community pharmacy dispensing: Storen et al (2022).

These payments consist of two components:39Department of Health, Disability, and Ageing (2026e).

- Component 1: $5.12 for each over co-payment 60-day script dispensed.

- Component 2: $0.13 for each over co-payment script dispensed.40In 2024–25, this covered 67 per cent of PBS dispenses: Department of Health, Disability, and Ageing (2026a, Tables 2a and 3a).

Together these payments will cost $2.1 billion from 2024 to 2029.41This covers the term of the eighth Community Pharmacy Agreement: Department of Health, Disability, and Ageing (2026e).

3.2 Pharmacy funding has structural flaws

There are three main problems with the design of dispensing fees:

- Pharmacies are reimbursed above the prices they pay for medicines, and the policy to fix it isn’t quick or precise enough

- The financial risks from stocking high-cost medicines are addressed through a wasteful and ineffective mark-up

- Pharmacies get several arbitrary, unfair, and costly fees

3.2.1 Price disclosure works, but not well enough

When a new medicine is added to the PBS, the approved ex-manufacturer price is set through negotiations between the manufacturer and the government. This process takes into account the cost of manufacture, the type of medicine, and the prices of other similar medicines.42Department of Health, Disability, and Ageing (2017).

The approved ex-manufacturer price is the maximum price at which a manufacturer can sell the medicine for.43See Section 84 of the National Health Act 1953. But they can – and often do – sell medicines to pharmacies for less than this price to gain market share.44Department of Health, Disability, and Ageing (2025b). Historically, this meant pharmacies could purchase medicines at discounted prices while being reimbursed the full ex-manufacturer price by the government, effectively profiting at taxpayers’ expense.

In 2007, the government introduced a price disclosure policy to claw back savings for taxpayers.45Ibid. Manufacturers are now required to report the actual prices at which medicines are sold, with reimbursement gradually reduced to reflect those prices.46Price disclosure applies to all multi-brand, off-patent, or generic medicines, unless specifically exempt: Department of Health, Disability, and Ageing (ibid).

Similar systems are used successfully in other countries, including in England47In England, reimbursement prices for Category M medicines – which covers most generic medicines – are set using purchase and sales data reported by manufacturers and wholesalers: Community Pharmacy England (2026). and in the Medicaid program in the US.48Medicaid provides health insurance for disadvantaged Americans. Pharmacies are regularly surveyed on prices and the results are used to calculate a national average price for each medicine. State Medicaid agencies can use these figures as the basis for pharmacy reimbursement. See Medicaid (2026).

In Australia, price disclosure has cut the price of many medicines. Over the past 10 years, there have been about 2,000 price reductions, averaging 21 per cent.49Analysis includes the October 2017 cycle to the April 2026 cycle, and counts unique medicines (medicine and form) rather than item numbers: Department of Health, Disability, and Ageing (2025c). The prices of 251 medicines were cut in 2024, saving the government and patients about $167 million in 2025.50Grattan analysis of Department of Health, Disability, and Ageing (2026c), Department of Health, Disability, and Ageing (2025d), and Department of Health, Disability, and Ageing (2024e). Savings are estimated by applying 2025 prescription volumes to the difference between prices before and after 2024 price disclosure reductions.

But two flaws limit the effectiveness of price disclosure.

First, because data are collected over six months and then processed over a further six months, it can take up to a year for a fall in market prices to translate into a lower PBS price.51There are two overlapping, year-long cycles, with price reductions in April and October: Department of Health, Disability, and Ageing (2025b). Shortening this cycle to monthly – as in England and the US – would deliver savings sooner.52See Community Pharmacy England (2026) and Medicaid (2026). To smooth out short-term fluctuations, reductions could be made on an annual basis using several months of data.

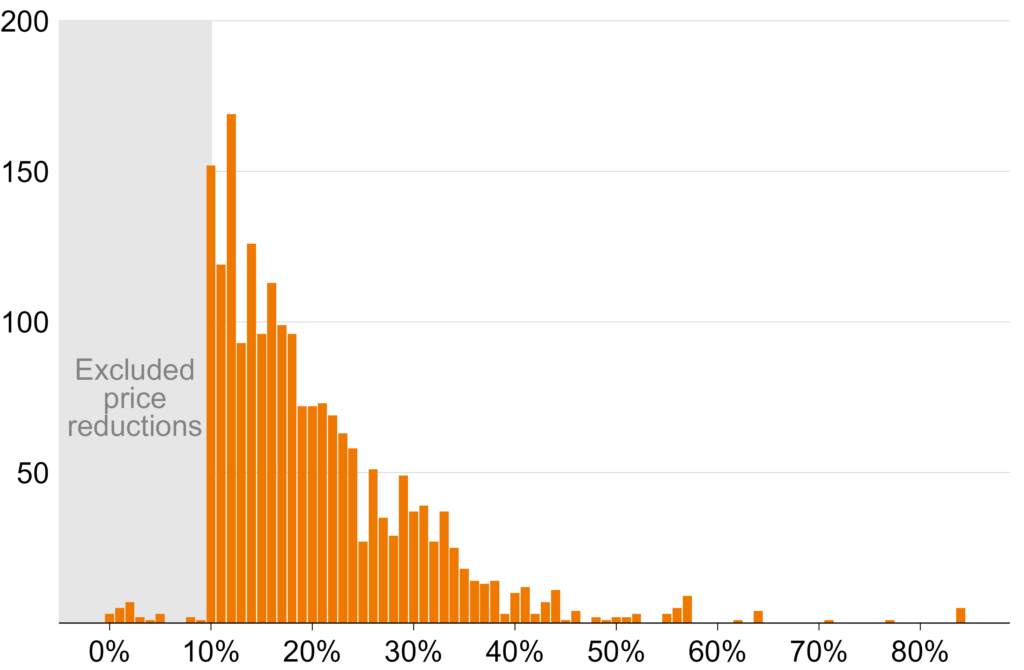

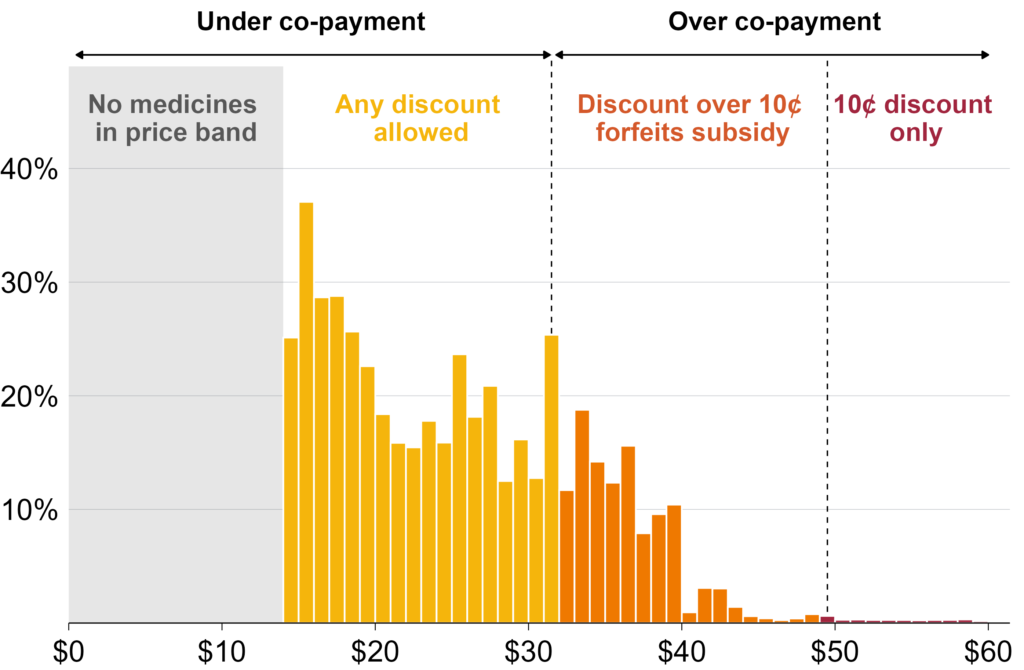

Second, price reductions only kick in if the discount is more than 30 per cent for some medicines and more than 10 per cent for others.53Designated brands – generally low-cost medicines that have been subject to price disclosure for several years – receive certain protections against medicine shortages, including a 30 per cent threshold for price reductions and a $4 price floor. An exception applies where discounting has averaged at least 12.5 per cent across the previous three data collection periods, in which case the standard 10 per cent threshold applies: Department of Health, Disability, and Ageing (2026f). Smaller discounts have been more common than larger ones over the past decade (Figure 3.2). But the thresholds mean that discounts smaller than 10 per cent are ignored.54Except where the price floor is hit. There is no good reason for these excluded discounts.55The distribution in Figure 3.2 probably understates the true cost of the thresholds. The visible gap below 10 per cent shows discounts that are never passed on, but medicines subject to the 30 per cent threshold can be discounted by up to 29 per cent without triggering any reduction at all. Those missed discounts are not visible in the chart.

Figure 3.2: Patients and taxpayers are probably missing out on more discounts below the 10 per cent threshold

Number of price disclosure reductions by size, October 2017 to April 2026

Notes: Includes all price reductions from the October 2017 to April 2026 price disclosure cycles. Reductions below 10 per cent are due to medicines from designated brands hitting the $4 price floor.

Source: Grattan analysis of PBS Brand Price Reductions Reports, available at Department of Health, Disability, and Ageing (2025c).

The threshold should be set to zero, so that each cycle the reimbursement price is simply reduced to match the average market price. Under this model, manufacturers would still have an incentive to discount to win market share, but those discounts would be passed on to taxpayers in full.

Since 2022, discounts have been ignored for some medicines that cost $4 or less.56Designated brands are subject to a price floor of $4: Department of Health, Disability, and Ageing (2026f). This is supposedly because shortages are more common for these medicines.57See the National Health Amendment (Enhancing the Pharmaceutical Benefits Scheme) Act 2021. But no public analysis has been released to show this, or to enable assessment of whether the policy has worked.

Price reduction thresholds should be removed and the justification for, and level of, the $4 price floor should be publicly reviewed.

3.2.2 A cheaper and better way to manage financial risk from high-cost medicines

Pharmacies receive an administration, handling, and infrastructure fee for every PBS medicine they dispense. One part of this is a fixed fee of $5.12 for the physical infrastructure to store and supply medicines. The other part increases with the cost of the medicine, which is intended to compensate pharmacies for the financial cost of stocking high-cost medicines, and reaches a maximum of about $100 (Table A.1 in Appendix A).

These two components should be separated.

The physical cost of storing a medicine does not vary with its price,58While some medicines are more expensive to store – for example those requiring refrigeration – price differences between medicines generally reflect patent status rather than storage requirements. For example, a brand-name medicine and its generic equivalent require identical storage but may be priced very differently. so the fixed component should simply be absorbed into the dispensing fee. The dispensing fee would then cover all costs associated with stocking, handling, and dispensing a medicine.

Unlike storage costs, financial risk does vary with medicine price.

The number of high-cost medicines on the PBS is rising.59The average dispensed price for over co-payment PBS prescriptions increased in real terms from $55 in 2014-15 to $95 in 2024-25: Department of Health, Disability, and Ageing (2016) and Department of Health, Disability, and Ageing (2026a). In 2024-25, just 10 medicines accounted for 30 per cent of all spending on over co-payment PBS medicines, with six of these medicines averaging more than $1,000 per dispense: Department of Health, Disability, and Ageing (2026a, Tables 3a and 5a). The King Review noted that current funding arrangements do not adequately support the supply of these medicines.60King et al (2017b, pp. 92-93).

The problem is the structure of pharmacy reimbursement.61All references in this and the following paragraph are from King et al (ibid). Pharmacies purchase medicines and are reimbursed only after dispensing them. If they can’t dispense a medicine – because a patient orders it specially and fails to collect it, or because it is damaged – the pharmacy has no reimbursement pathway and bears the full cost. Separately, pharmacies must pay GST at the point of purchase but cannot reclaim it until the end of the month. For most medicines, that is manageable, but for a medicine costing tens of thousands of dollars it may not be.

Pharmacies may choose not to stock these medicines at all, or to order them only after considerable delay.62The interim report of the King Review observed that this was already happening in some instances, referencing a survey of pharmacies conducted by the Australian Journal of Pharmacy that found that 22 per cent were not stocking high-cost hepatitis C treatments due to cash-flow issues: King et al (2017a, p. 130). This could have real consequences for patients.

Until now, the financial risk associated with high-cost medicines has been managed through the administration, handling, and infrastructure fee, with more expensive medicines attracting a higher fee. But even the highest level is low compared to the cost of some medicines, only covering a tiny fraction of the potential financial loss. For the 217,000 PBS scripts dispensed in 2025 with a wholesale cost greater than $5,000, it covered less than 2 per cent of these costs.63Grattan analysis of Department of Health, Disability, and Ageing (2026c) and Department of Health, Disability, and Ageing (2026b). Wholesale cost here is approved ex-manufacturer cost plus wholesale mark-up, reported as ‘Price to Pharmacists’. Note that some highly specialised medicines attract a different handling fee instead of the standard administration, handling, and infrastructure fee, but this fee is even lower: the maximum is $40, compared to about $100 for standard medicines: Department of Health, Disability, and Ageing (2024f).

With the fixed component of this fee moved into the dispensing fee, the variable component should be abolished and replaced with a risk-sharing mechanism that pays pharmacies faster for these high-cost medicines.

For medicines with an ex-manufacturer price above a defined level, the government should pay pharmacies a fixed proportion – say, 80 per cent – of the purchase price when the pharmacy purchases the medicine, rather than waiting until dispensing.64The optimal threshold and proportion would need to be determined carefully, taking into account the distribution of medicine prices, pharmacy cash-flow patterns, and the risk of stock management distortions at the boundary.

Almost none of this would be new expenditure: it’s money the government would pay anyway once the medicine is dispensed, just brought forward to give pharmacies security when they stock high-cost medicines. By covering most, but not all, of the upfront cost, the government would reduce the financial risk of stocking these medicines without eliminating the incentive not to waste them.

The cost to government of paying for medicines that are not dispensed would probably be small. And the savings would probably be substantial: in 2024-25, pharmacies received almost $285 million in variable, cost-linked administration, handling, and infrastructure fees on over co-payment scripts alone.65Figure reported in 2024-25 dollars. Calculated by multiplying the number of over co-payment prescriptions dispensed by the baseline fee – $4.79 at the time – and then subtracting that amount from total administration, handling, and infrastructure fees received by community pharmacies in 2024-25: Department of Health, Disability, and Ageing (2026a, Tables 3a and 17a) and Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024). The number of over co-payment prescriptions dispensed was found by multiplying the total PBS scripts from Table 15a by the ratio of prescriber’s bag to non-prescriber’s bag prescriptions from Table 3a and then adding the total RPBS scripts from Table 15a: Department of Health, Disability, and Ageing (2026a).

This reform would reduce a barrier to patient access to high-cost medicines, and deliver savings to taxpayers in the process.

3.2.3 Some smaller fees are unjustified and unfair

Pharmacy remuneration includes many small fees. Three of them cannot be justified: the allowable additional patient charge and the Safety Net recording fee, which are charged to patients, and the Additional Community Supply Support payment, which is paid by the government.

The allowable additional patient charge

When a medicine costs less than the maximum patient co-payment, pharmacists may charge general patients an additional fee of up to $2.79, provided the patient’s total out-of-pocket cost does not exceed the maximum co-payment amount.66Department of Health, Disability, and Ageing (2026d).

This fee doesn’t compensate for a service. If dispensing fees are set to cover the full cost of dispensing (see Chapter 4), then it’s just a government-sanctioned surcharge on patients buying cheap medicines.

The cost to patients adds up. No data are reported on how often the fee is charged. But in 2025, if all eligible prescriptions had attracted the maximum fee, it would have cost patients up to $347 million.67Grattan analysis of Department of Health, Disability, and Ageing (2026c) and Department of Health, Disability, and Ageing (2026b). This figure is calculated using an allowable additional patient charge of $3.45, which was its value in 2025. It has since fallen to $2.79 in line with a reduction in the maximum patient co-payment. In 2025, about 80 per cent of the 127 million non-Safety Net scripts dispensed for general patients were eligible.

The discretionary nature of the fee is also unfair. Pharmacists will be more likely to waive it if they face price competition from nearby pharmacies. In areas with less competition – for example, rural and regional areas with limited pharmacy access – patients may have no choice but to bear the full additional charge. This means the fee falls most on those with the least ability to shop around.

The solution is simple: the fee should be removed.

The Safety Net recording fee

The PBS Safety Net allows patients who spend above a certain amount on medicines in a calendar year to pay less for their remaining prescriptions that year.68The threshold is currently $1,748.20 for general patients, after which they pay the concessional co-payment rate, and $277.20 for concession patients, after which their medicines are free: Department of Health, Disability, and Ageing (2026g).

To access the scheme, patients must have their spending on prescriptions recorded. This is done either by attending the same pharmacy each time – which keeps a digital record – or by the patient physically carrying a paper record to present at each pharmacy they visit.69Department of Health, Disability, and Ageing (2026g) and Services Australia (2026).

The clunkiness of this system is limiting its effectiveness. While no official data are available, in 2025 the ABC reported that almost 500,000 Australians who qualify for the Safety Net each year do not access it, potentially forgoing hundreds of dollars in savings each.70Branley and Lloyd (2025).

Pharmacies can choose to charge the Safety Net recording fee – $1.54 for ready-prepared medicines and $1.99 for compounded medicines – as compensation for the administrative work of recording prescriptions.71See Department of Health, Disability, and Ageing (2026d). No data are available on how often pharmacies choose to charge this fee.

But there are two problems with this fee.

First, the task it compensates for is trivial. Recording a prescription involves filling out a simple table.72Pharmacists must enter the date, their signature, and three clinical details – all of which are typically automatically generated by pharmacy software. Some pharmacies use software that automatically prints a label with this information, which can then be stuck directly onto the form: Department of Health, Disability, and Ageing (2026g). But dispensing involves many small administrative steps – not all of which apply to every medicine – so there is no reason to pay a discrete fee for this one and not the others.

Second, the fee applies to some patients and not others. As with the allowable additional charge, pharmacists can apply it only to general patients, for under co-payment medicines, where the fee doesn’t push the patient’s out-of-pocket cost above the co-payment cap.73Department of Health, Disability, and Ageing (2026d).

These conditions shield concession-cardholders from extra costs and prevent fees from exceeding the maximum co-payment. But if the purpose is to compensate pharmacists for a service they perform, limiting the scripts that attract the fee makes little sense. The administrative work of Safety Net recording does not vary by concession status or medicine price.

The solution is to abolish the fee and automate PBS Safety Net recording entirely, as is already done for Medicare Safety Nets.74For individuals, Services Australia automatically records Medicare expenses and applies the benefit once the threshold is reached: Department of Health, Disability, and Ageing (2025e). This would eliminate the administrative burden for pharmacists and ensure no patient misses out.

Additional Community Supply Support payments

Unlike the other two unjustified fees, which are paid entirely by patients, Additional Community Supply Support payments are paid by the government.

The payments are intended to compensate pharmacies for lost dispensing revenue from 60-day dispensing (see Box 2).75Pharmacy Guild of Australia (2024a).

There are three problems with this justification.

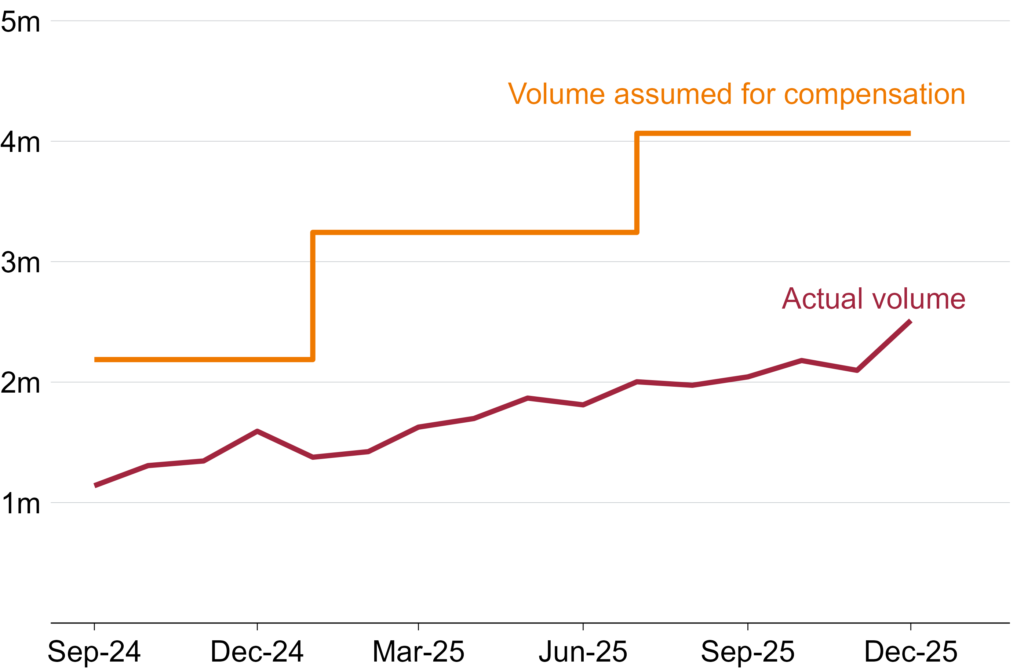

First, uptake of 60-day dispensing has been much slower than expected. In 2025, only about half of the 60-day prescriptions that were forecast in the eighth Community Pharmacy Agreement actually materialised (Figure 3.3).76In 2025, actual 60-day prescriptions made up only 51.6 per cent of those forecast: Grattan analysis of Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024) and Department of Health, Disability, and Ageing (2026c).

Figure 3.3: Compensation for 60-day dispensing losses was based on overestimates of uptake

Forecast and actual monthly volume of over co-payment PBS medicines dispensed from 60-day prescriptions

Notes: Medicines were added to the eligibility list for 60-day dispensing in three stages, with the final stage commencing in September 2024. Volume forecasts are from half-yearly forecasts provided in the eighth Community Pharmacy Agreement, which have been divided by the number of months to convert them to average monthly rates. Actual volumes are calculated using the methodology outlined in Breadon and Hu (2025).

Source: Grattan analysis of Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024) and Department of Health, Disability, and Ageing (2026c).

Yet pharmacies were compensated as if the forecast had been met. The Community Pharmacy Agreement guarantees pharmacies the full $2.1 billion regardless of actual dispensing volumes.77Where over co-payment 60-day prescription volumes fall short of forecasts, Additional Community Supply Support unit payments are increased to make up the difference: Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024, Appendix A). See Box 5 for detail.

Second, the payments are poorly targeted. Compensation should have been tied only to the number of 60-day scripts dispensed, since they reduce dispensing volume and revenue. Instead, most standard 30-day scripts attract small compensation payments too, meaning pharmacies are compensated regardless of whether they are affected by the policy change at all.

The third problem is that, like all components of pharmacy remuneration (see Chapter 4), the values of the payments lack any transparent or evidence-based justification. There is no public documentation of how the values were determined or whether they bear any relationship to actual losses incurred.

Additional Community Supply Support payments should be removed.

The right way to maintain sector viability is with fair dispensing fees that cover the cost of dispensing, and focused support for struggling pharmacies. The next chapter shows how to do it.

4 Set the right price

Not only is pharmacy remuneration poorly structured – as the previous chapter showed – the level is also set the wrong way.

Community pharmacies exist to ensure all Australians have adequate, safe, and equitable access to medicines. Achieving that requires dispensing fees that fairly compensate pharmacists – while also ensuring public money is spent wisely.

But dispensing fees are set through negotiation and not grounded in real-world evidence, so there is no way to know whether they represent fair value – for patients, taxpayers, or pharmacies themselves.

Fees should instead be based on the actual cost of dispensing, with ongoing monitoring of pharmacy profitability.

4.1 Dispensing fees are a stab in the dark

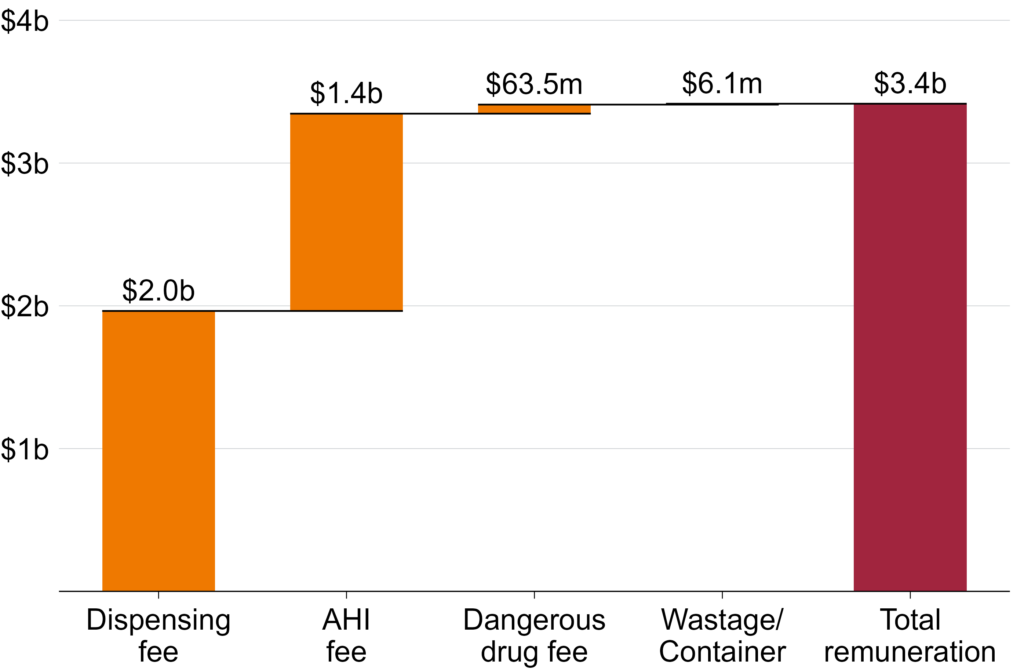

Pharmacy remuneration is the largest financial component of the Community Pharmacy Agreement.78Ibid (pp. 8-9). In 2024-25, pharmacies were paid about $3.4 billion (Figure 4.1).79Figure is in 2025 dollars.

Community pharmacies dispensed 335 million prescriptions in 2024-25, so even a small increase quickly adds up: each additional cent per script translates to $3.4 million for pharmacies.80Department of Health, Disability, and Ageing (2026a, Tables 2a and 2c). Even overpaying slightly has big budget consequences. Yet fee levels have been determined through successive Community Pharmacy Agreement negotiations, with no public justification.81By contrast, the English government has commissioned two independent studies of the costs and profitability of community pharmacies in the last 15 years to inform contractual negotiations: PricewaterhouseCoopers (2011) and Frontier Economics (2025).

Figure 4.1: Pharmacy remuneration costs billions each year

Pharmacy remuneration for over co-payment dispensing by cost component, 2024-25

Notes: AHI = Administration, handling, and infrastructure. Values include total government and patient funding for over co-payment Section 85 and Section 100 PBS items dispensed by community pharmacies. Wastage fees compensate pharmacies for medicines that cannot be dispensed because a pack had to be opened to supply a smaller quantity than the standard pack size, and container fees cover the cost of any additional packaging supplied with a dispensed medicine: Department of Health, Disability, and Ageing (n.d.).

Source: Department of Health, Disability, and Ageing (2026a, Table 17a).

4.2 We might be paying too much for dispensing

No one knows what it actually costs to dispense a prescription in an Australian community pharmacy.82This was a key call-out in the King Review: King et al (2017b, p. 62). And it’s no accident. Unlike in other countries, efforts in Australia to establish the real cost of dispensing have been blocked by the Guild, forcing the government to negotiate fees in the dark (Section 1.2).

But while there is currently no way to know if pharmacies are being overpaid, or underpaid, there are signs that the sector may be over-compensated.

4.2.1 Funding has grown despite efficiency gains

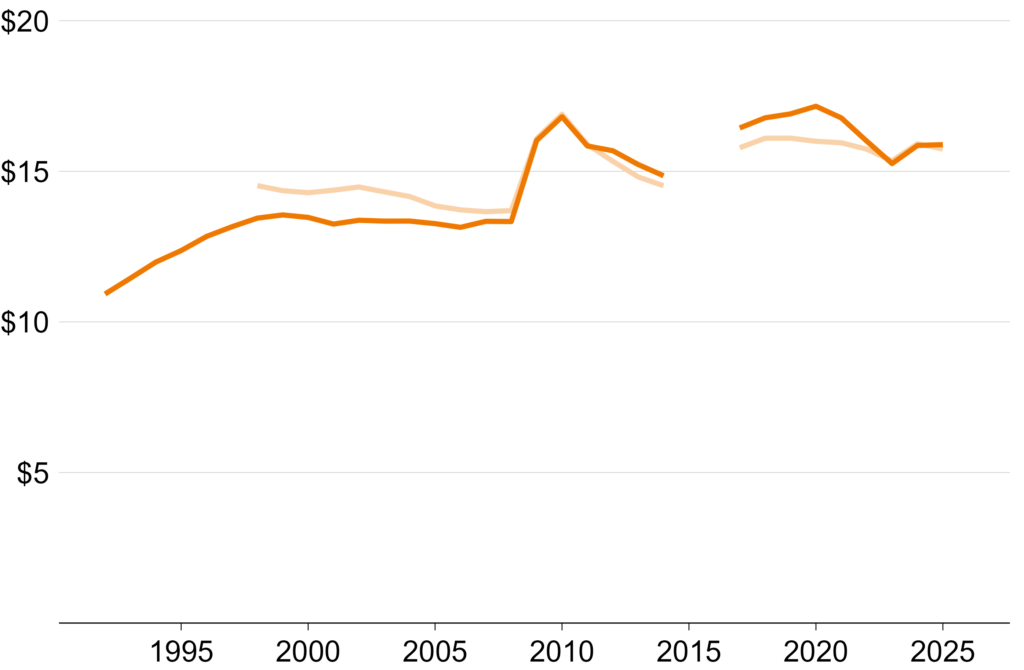

Dispensing payments for each over co-payment script have risen by 45 per cent since the first Community Pharmacy Agreement was signed in 1990, after accounting for inflation (Figure 4.2).83Growth in pharmacy remuneration has outpaced both the Consumer Price Index (CPI) and Wage Price Index (WPI) – rising from $10.90 in 1991-92 to $15.90 in 2024-25 in today’s dollars. We use CPI rather than WPI because productivity gains from automation over that period mean labour costs per script should have risen more slowly than wages. Some of this increase may reflect legitimate cost pressures – an older, sicker population and growing polypharmacy may place greater demands on pharmacists’ time.84For trends in polypharmacy, see Lee et al (2026). Polypharmacy is the simultaneous, regular use of multiple medications, often defined as five or more, by an individual: RACGP (2019).

Figure 4.2: Pharmacy remuneration has increased since the first Community Pharmacy Agreement

Average pharmacy remuneration per over co-payment script, adjusted for inflation using CPI and WPI

Notes: CPI = Consumer Price Index. WPI = Wage Price Index. Average remuneration per script is calculated as total pharmacy remuneration (excluding ex-manufacturer costs, wholesale remuneration, Additional Community Supply Support program, cost Funding of Chemotherapy, and funding for pharmacy professional programs) divided by total pharmacy prescription volume and inflated to March 2026 dollars using both the CPI and WPI: ABS (2026a) and ABS (2026b). WPI was first reported in 1997. Years refer to the end of the financial year (e.g. 1991-92 is shown as 1992). Data for 2014-15 and 2015-16 are not available. The jump in 2008-09 is partially due to the introduction of the Premium Free Dispensing Incentive and PBS online payments: ANAO (2015).

Sources: Data for 1991-92 to 2013-14 from ANAO (ibid, Appendix 10); for 2016-17 to 2024-25 from Tables 15a and 17a of the PBS Expenditure and Prescriptions

reports, available at Department of Health, Disability, and Ageing (2026a), though table numbers vary across editions.

But over the same period, technology has substantially reduced the labour required to dispense a standard script. PBS Online Claiming and ePrescribing have replaced labour-intensive, paper-based systems.85Online claiming was introduced in 2005 and ePrescribing in 2020: ANAO (2024) and Pharmaceutical Society of Australia (n.d.). As of December 2024, 99.9 per cent of claims were processed online. In a 2022-23 survey of 120 Australian community pharmacies, 40 per cent reported a reduced workload due to ePrescribing and Electronic Health Records: Hareem et al (2024). A time-and-motion study of five NSW and Queensland pharmacies identified similar efficiencies: ADHA (2023). Automated dispensing robots – already common in Australian hospitals86See Levy (2022). A systematic review of automated dispensing in hospitals identified significant efficiency gains: Batson et al (2021). – are increasingly being used in community pharmacies,87Numerous manufacturers now market automated dispensing systems specifically to community pharmacies, advertising significant efficiency gains. For example Willach Pharmacy Solutions (n.d.) and Meditech (n.d.). further reducing physical labour. And online dispensing (see Box 4) will only continue to streamline dispensing.

Yet negotiated fees have never been adjusted to reflect these efficiency gains, meaning all the cost savings have flowed to pharmacies, and none to patients or taxpayers.

Box 4: Online dispensing

Online dispensing involves patients having their prescription medicines delivered, with written medicine information supplied, and pharmacist advice available by phone or online.aPharmacy Board of Australia (2023, p. 6) and Pharmaceutical Society of Australia (2019).

Online dispensing offers patients greater convenience and access to medicines, and demand will probably grow over time.bLimbu and Huhmann (2024).

Pharmacy policy needs to adapt to support the benefits of online dispensing while addressing the potential risks:

– Quality and safety: International evidence suggests online dispensing can improve medicine adherence relative to in-person dispensing.cSchwab et al (2019), Schmittdiel et al (2011), and Khandelwal et al (2011). Quality and outcomes of online dispensing should still be monitored.

– Pricing: To ensure patients and taxpayers don’t over- or under-pay for online dispensing, the Independent Health and Aged Care Pricing Authority should consider whether a different remuneration structure is needed.

– Equitable access to pharmacies: Online dispensing may increase access to medicines for those who cannot easily visit a pharmacy, but this may also reduce the need for some brick-and-mortar pharmacies.dJervelund et al (2025). Resulting pharmacy closures could threaten medicine access for patients who do not use online options, and reduce locations delivering pharmacy services. This risk should be assessed as part of the proposed viability monitoring scheme.

4.2.2 Pharmacists may be paid for time they don’t spend

Some pharmacy payments – the dispensing fee, dangerous medicine fee, and Safety Net recording fee – pay for a pharmacist’s time and related overheads rather than infrastructure.

For these payments, we can work backwards from the fee levels and the typical pharmacist’s hourly pay rate to calculate how many minutes of pharmacist time each fee implicitly funds (Table 4.1).88In 2025, the median hourly pay rate for pharmacists more broadly – including hospital and industrial pharmacists – was $52: Jobs and Skills Australia (2025). This method uses 2024-25 fees for consistency, and assumes they cover only pharmacist labour and related on-costs, and no profit. These estimates are therefore indicative only: in practice, the dispensing fee covers the full labour chain – including assistants and technicians. On this basis, for example, it would take a community pharmacist about eight minutes to dispense a ready-prepared prescription.89This also implies that compounded medicines take less than two minutes longer to dispense than ready-prepared medicines – almost certainly too low. Compounded medicines comprise a tiny minority of total prescriptions, so this barely affects overall fee adequacy – but for specialised compounding pharmacies, fees may significantly undercompensate the labour involved.

Table 4.1: Implied time taken for components of dispensing

Notes: Calculated using an estimated hourly pay rate of $52 for community phar-macists, with a 1.3 multiplier applied to capture related on-costs: ANU (2015).

Source: Grattan analysis of Department of Health, Disability, and Ageing (2026d) and Jobs and Skills Australia (2025).

Unfortunately, there is little research on how long these tasks actually take. The only available Australian evidence – a time-and-motion study of 15 community pharmacies in WA and NSW – found that across almost 100 hours of observed dispensing time, there were about 5,700 prescriptions dispensed.90Total dispensing time taken from Karia et al (2022, Table 2), and includes time spent solely on dispensing as well as multi-tasking time. Number of prescriptions provided to Grattan by the author on request. That’s one every 62 seconds, on average.

This evidence isn’t definitive – it draws on a small sample of pharmacies and may not be nationally representative. It also probably understates total dispensing time, since pharmacy assistants and other pharmacists often handle parts of the process and their time may not have been captured. Even so, the total labour time per prescription – across all staff involved – is probably far less than the eight minutes the dispensing fee implicitly funds.

4.3 Dispensing fees should reflect the cost of dispensing

In Chapter 3, we made the case for a simpler dispensing fee that no longer includes unjustified payments. Critically, the level of this fee should be grounded in actual cost data.

In a well-functioning pharmacy sector, the dispensing fee should cover the cost of dispensing a medicine plus a reasonable profit margin.91For example, this margin could be set equal to the average return on capital across the community pharmacy sector – that is, for each dollar of capital invested in a business, how much profit it earns.

Fortunately, an institution already exists with relevant expertise for setting this fee.92While the Pharmaceutical Benefits Remuneration Tribunal (PBRT) still technically exists, it has only five members, one of whom requires Guild approval before appointment: Department of Health, Disability, and Ageing (2025f) and section 98 of the National Health Act 1953. It lacks both the resources and the independence required for this task. The Independent Health and Aged Care Pricing Authority (IHACPA) is an independent statutory body that already develops evidence-based pricing advice for government. Most relevantly, it uses detailed cost data from aged care providers to calculate funding rates.93Registered aged care providers are required to submit quarterly financial reports to government: Department of Health, Disability, and Ageing (2026h). IHACPA draws on this data alongside its own cost collections to develop pricing advice: IHACPA (2025a).

IHACPA will need to determine the most appropriate method for calculating the baseline cost of dispensing.

One approach is calculating the actual average cost of dispensing a medicine.94The King Review proposed a similar approach to calculate best-practice dispensing costs: King et al (2017b, Recommendation 5.2). This will require data on cost inputs – including labour and infrastructure – as well as the time taken to dispense. IHACPA could gather these data as part of a broader time-and-motion study of community pharmacy covering dispensing and other professional services.95A similar time-and-motion study existed for general practice. The Bettering the Evaluation and Care of Health (BEACH) study ran from 1998 to 2016, with a nationally representative sample of GPs: University of Sydney (n.d.). This model has since been adapted for general practice nurses, nurse practitioners, physiotherapists, and Aboriginal and/or Torres Strait Islander Health Workers through the new Occasions of Care Explained and ANalysed (OCEAN) study: University of Sydney (2025). Similar large-scale studies have been conducted on community pharmacies in the US to inform Medicaid pricing: Shoemaker-Hunt et al (2020). These data could be collected from a representative sample of community pharmacies each year, and the dispensing fee updated to reflect changes in technological efficiency, medicine complexity, and patient mix. Pharmacy participation should be mandatory, as a condition of receiving PBS payments.

Where cost data reveal a type of dispensing that is significantly more or less expensive and unevenly distributed across pharmacies, IHACPA should set an additional targeted fee. This may include compounded medicines,96Compounded medicines are more labour-intensive to dispense than ready-prepared medicines and are concentrated among specialist pharmacies: Cooper et al (2025). Without a targeted fee, these pharmacies would be systematically undercompensated. complex or dangerous medicines, or in-person dispensing as opposed to online.

We estimate that expanding IHACPA’s role to include community pharmacy would cost about $9.8 million per year, with any necessary primary data collection adding a further $3.3 million a year.97See Appendix D for the methodology used to estimate these costs.

Implementing this change will require amending the National Health Act 1953 to give IHACPA responsibility for advising on community pharmacy dispensing fees.

4.4 A better approach to protecting sector viability

Setting fees that cover costs is the best way to ensure the sector as a whole is financially viable. Instead, the government gives the sector a blanket revenue guarantee. Rural subsidies take the same unfocused and wasteful approach, providing extra funding whether a pharmacy needs it or not.

Policy should focus on the real goal: maintaining patient access to medicines. Financial viability should be actively monitored using administrative tax data to identify pharmacies that genuinely need support, and make sure they get it.

4.4.1 Replace a blanket guarantee with targeted support

Community Pharmacy Agreements guarantee a total amount of pharmacy remuneration. Under the current agreement, it is $24.6 billion over five years.98Department of Health, Disability, and Ageing and Pharmacy Guild of Australia (2024, Table 2). This includes the Additional Community Supply Support payments but excludes funding for pharmacy programs.

That funding is locked in through the payment adjustment mechanism (Box 5). If there are fewer scripts than expected, the fees paid for each script are adjusted up, to ensure pharmacies still receive the promised total. And the opposite is true if there are more scripts than expected. This reduces the risk of unexpected government spending while securing pharmacy income.

The goal of ensuring pharmacies can viably and safely dispense medicines is legitimate, but the payment adjustment mechanism is the wrong instrument, for four reasons.

First, it is skewed in pharmacies’ favour. If prescription volumes exceed forecasts by more than 10 per cent, fees are reduced to claw back the overpayment. But if volumes fall short by any amount – even by 1 per cent – fees are increased to make up the shortfall.99Pharmacy Guild of Australia (2024a). Taxpayers have got the short end of the stick.

Second, locking in funding five years in advance makes it difficult for the system to respond to changing circumstances, such as improvements in efficiency driven by technological advances.

Third, the payment adjustment mechanism compensates all pharmacies equally regardless of individual circumstances. Dispensing volumes will not fall uniformly – some pharmacies will have increases, others decreases – yet the mechanism adjusts remuneration sector-wide, meaning pharmacies who haven’t suffered any adverse impacts will benefit alongside those who have.

Fourth, even where dispensing volume does fall, viability is not necessarily threatened. Pharmacies with high margins or strong non-dispensing revenue (Box 3) can absorb modest volume reductions without any risk to survival.

Instead of guaranteeing a fixed pot of money to the sector regardless of need, the government should monitor viability and respond accordingly. It should use existing administrative tax data to assess pharmacy profitability across location types, ownership models, and pharmacy formats. If parts of the sector are struggling, affected pharmacies should be able to seek support if they provide additional financial information demonstrating genuine need. But support should be provided only if a closure would leave a community without equitable and adequate access to medicines. If that can be achieved by other pharmacies in the area, or by online dispensing, additional support should not be provided.

Box 5: The Community Pharmacy Agreement payment adjustment mechanism