Summary

State and local governments typically require new housing to include off-street parking – often much more than residents want, needlessly driving up the price of housing.

Download the technical supplement

Many apartment dwellers do not want or need car-parking. About 40 per cent of households in studio or one-bedroom apartments, and 19 per cent of households in two-bedroom apartments, do not own a car. And 58 per cent of households in family-sized apartments with three or more bedrooms have just one car, or none.

The result is a mismatch between what parking is mandated, and what’s needed. There are more car spaces in apartments in Sydney and Melbourne than cars. Off-street car-parking accounts for 13 per cent of the built floor space of apartments in these cities. And as much as 40 per cent of these spaces sit vacant each night.

This report shows that every year, Australia spends more than $1 billion building off-street car-parking that residents don’t want or need.

These rules add $70,000 to the cost of building a typical two-bedroom apartment in Sydney, $62,000 in Melbourne, $113,000 in Brisbane, $137,000 in Perth, and $95,000 in Adelaide. This extra cost acts as a handbrake on new housing.

State and local governments should remove parking requirements for new housing developments. Home-builders would still provide the spaces that home-buyers want, but not at the level currently forced upon them. When cities abroad removed minimum parking policies, new residential developments included parking at around half of the rate, or sometimes less, than previously required.

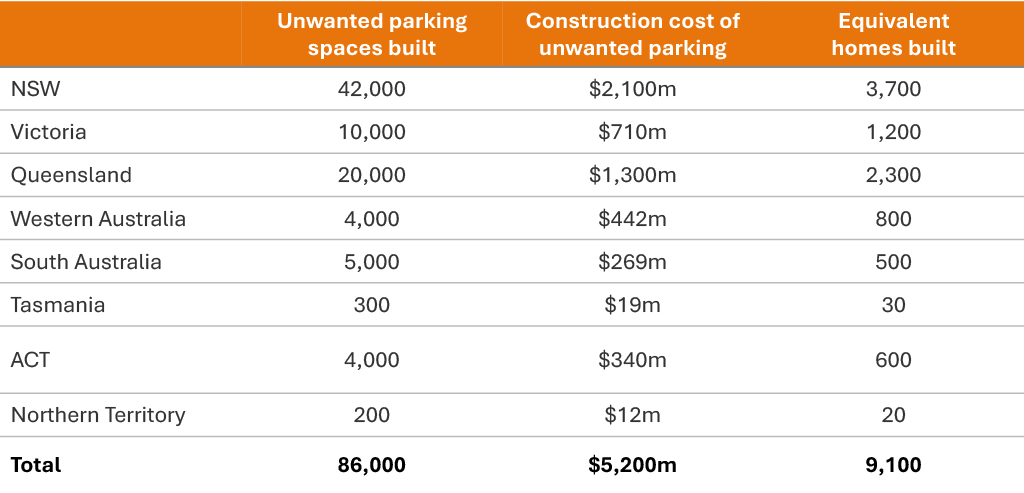

This change would cut thousands of dollars from the cost of new homes and shave months off the time to construct them. It would avoid the cost of constructing more than 86,000 unwanted car spaces nationwide over the next five years – spaces that would otherwise consume $5.2 billion in construction resources that could go toward building more than 9,000 extra homes.

State and local governments should instead better manage demand for on-street car-parking in high-demand areas. Most on-street car-parking is free to use, and is typically occupied by local residents who already have off-street spaces. Better managing on-street car-parking via permit schemes, time limits, and user pricing would reduce congestion on our streets. Charging for on-street parking would also provide a valuable source of revenue for cash-strapped local councils that could be reinvested in local infrastructure.

State and local governments should also remove barriers to allowing parking spaces to be purchased or rented separately from housing. ‘Unbundling’ car spaces from homes would give residents greater choice to purchase or rent parking in line with their needs – making housing cheaper for households that don’t want a car space, and reducing pressure on on-street parking.

Letting Australian homebuyers choose the car-parking they need will make housing cheaper, get more homes built faster, and create more walkable, cleaner, and better-designed cities.

Recommendations

Recommendation1

State and local governments should remove all car-parking

requirements for new housing developments.

Recommendation 2

State and local governments should adopt tools to manage demand for on-street parking – such as parking permit schemes, time limits, and user charging – in high-demand areas.

Recommendation 3

State and local governments should facilitate the unbundling of car-parking rights from new housing, so that parking spaces can be purchased or leased independently of the home, giving residents greater choice over the parking they pay for.

Recommendation 4

The federal government should encourage the states and territories to remove car-parking requirements for new housing developments.

1 Home-builders are forced to build too much car-parking

Australia has a shortage of housing – especially where people most want to live. Planning rules set by state and local governments are a significant part of the problem. Among the most consequential, yet least scrutinised, are the rules dictating how much off-street car-parking new housing must include.

Off-street car-parking accounts for 13 per cent of the floor space of apartments in Sydney and Melbourne. But many residents do not want or need off-street parking: on average, about 40 per cent of households in a studio or one-bedroom apartment across Australia’s capital cities do not own a car. Among households in two-bedroom apartments, 19 per cent do not own a car, and 58 per cent of households in three-or-more-bedroom apartments have one car or none.

Most studio and one-bedroom apartments – where car ownership is lowest – typically include at least one off-street parking space. And most three-bedroom apartments have more than one car space.

There are more car spaces in apartment buildings in Sydney and Melbourne than there are cars owned by residents. As much as 40 per cent of off-street car parking sits vacant each night.

1.1 Planning rules don’t just govern where homes get built – they govern parking too

Australia’s housing crisis is, in large part, a planning problem. Grattan Institute’s 2025 report More homes, better cities: Letting more people live where they want, showed that state and local government planning rules add hundreds of thousands of dollars to the cost of new housing in our capital cities, and lock most of our well-located residential land into low-density use.1Coates et al (2025).

But the planning rules don’t stop at building heights, setbacks, lot sizes, and where apartments are allowed. They also dictate how much off-street car-parking each new home must include. These minimum car-parking requirements add to the cost of new homes, and stop many from being built at all.

1.2 State and local government rules typically require a lot of off-street car parking in new housing

Minimum car-parking rules were introduced into planning schemes in the 1950s, to accommodate rapidly increasing vehicle use and pressures on on-street car-parking.2For example, the first Melbourne-wide off-street parking requirements were introduced in 1954 as part of the Melbourne Metropolitan Planning Scheme: Taylor (2017, Table 1).

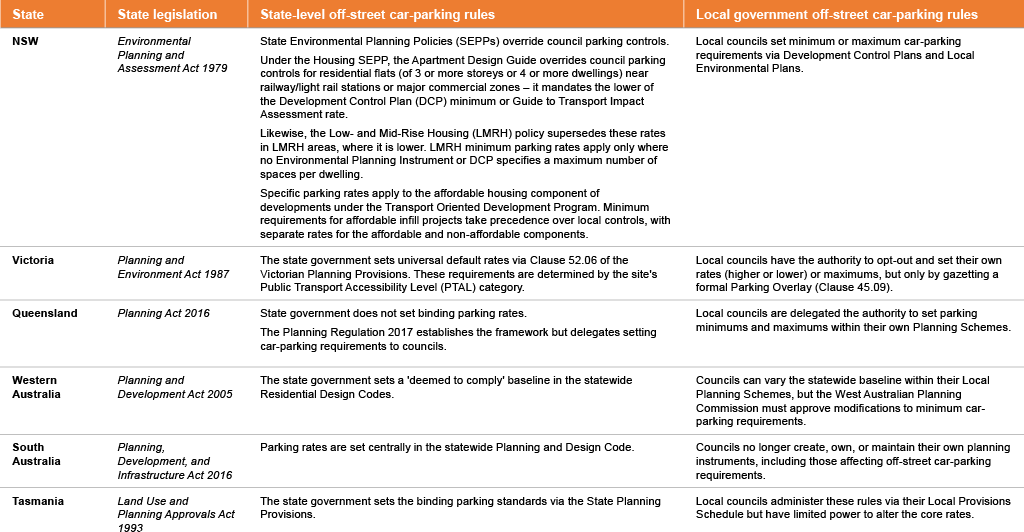

Most states3In this report, ‘states’ refers to Australia’s states and territories. impose minimum car-parking rules for new housing developments. Local councils in many states also set parking rules via local planning instruments (Figure 1.1).4Governments typically also mandate the minimum number of parking spaces that commercial premises should provide.

Car-parking rules typically vary depending on the type of dwelling, number of bedrooms, and location, including proximity to public transport.5See Appendix A in the Technical Supplement to this report.

In late 2025, the Victorian Government abolished minimum car-parking requirements in areas a short walk from train, tram, or bus routes with frequent service, and relaxed minimum requirements in other areas [Box 1].

Figure 1.1 Most states set minimum car-parking rules for new residential developments

Note: This list is not exhaustive – it doesn’t capture all state government policies, rules, schemes, instruments, and other regulations relating to off-street car-parking in new residential developments. Sources: State government planning system legislation and governance documents.

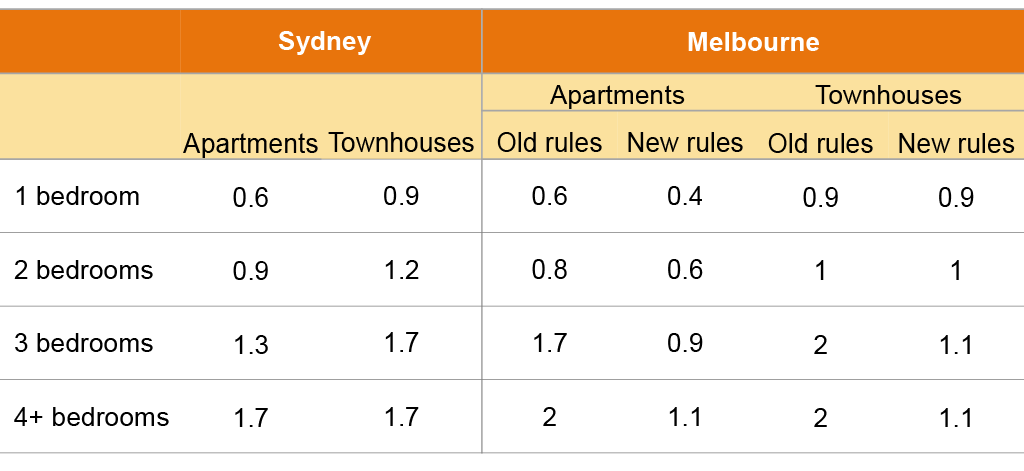

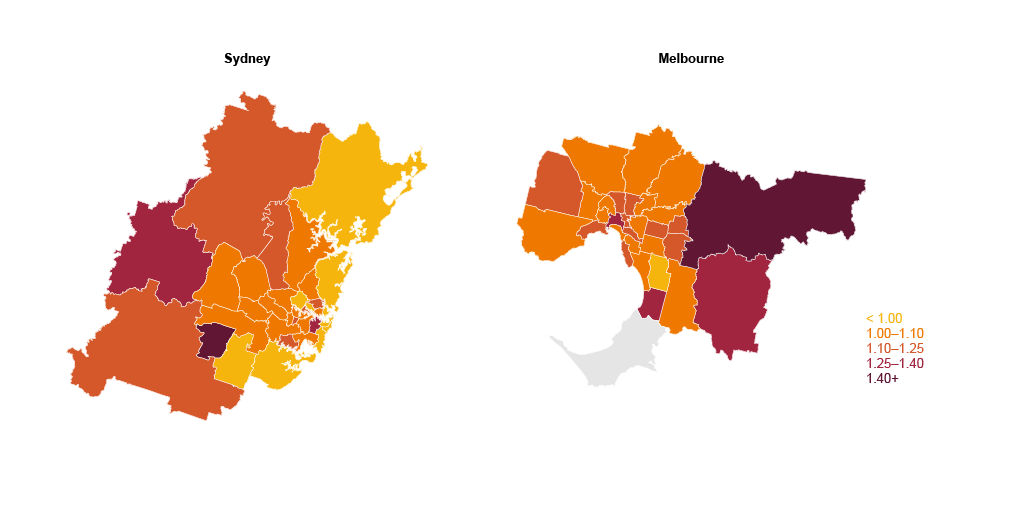

In Sydney, one-bedroom apartments on average require 0.6 car spaces, rising to 0.9 spaces for two-bedroom apartments, and 1.3 spaces for three-bedroom apartments (Figure 1.2).

Across Greater Melbourne, one-bedroom apartments are now required to provide an average of 0.4 off-street parking spaces, rising to 0.6 spaces for two-bedroom apartments, and 0.9 spaces for three-bedroom apartments (Figure 1.2).6See Appendix E in the Technical Supplement to this report for methodology. Parking rules for new homes in Victoria are now set with reference to PTAL (Public Transport Accessibility Level) categories. Well-serviced areas can have no car-parking spaces; in poorly-serviced areas, up to 1.2 spaces per dwelling are required.

Some local governments in inner-city areas, such as the City of Sydney and the City of Melbourne, impose maximum (rather than minimum) off-street parking rates for new residential developments. Brisbane City Council imposes maximum rates in areas with good public transport.7See Committee for Sydney (2022, p. 64), Streets Alive Yarra Inc. (2026), and Brisbane City Council (2014).

Figure 1.2: State and local government rules require a lot of parking, especially for larger homes.

Average minimum parking spaces required

Notes: See Appendix E in the Technical Supplement to this report for how minimums are calculated. Old rules refer to pre-December 2025 Principal Public Transport Network rates. New rules refer to Public Transport Accessibility Level categories.

Sources: Grattan analysis of Cotality (2025) and Melbourne and Sydney planning data (see Appendix E in the Technical Supplement for details).

1.3 These rules lead to more car-parking being built than residents want or need

Minimum car-parking requirements force developers to build parking that many home-buyers don’t want or need.8Chapter 2 measures the gap between cost and value across Sydney and Melbourne.

Where minimums apply, developers rarely exceed them. In Melbourne, 73 per cent of apartments and 70 per cent of townhouses built since 2019 provided only the legal minimum.9Grattan analysis of Cotality (2025) and Victorian Government (2025a). Excludes visitor parking requirements. Only includes dwellings subject to a non-zero minimum. Where the minimum requirement is fractional (6.7 per cent of dwellings), it is rounded down to the nearest whole number.

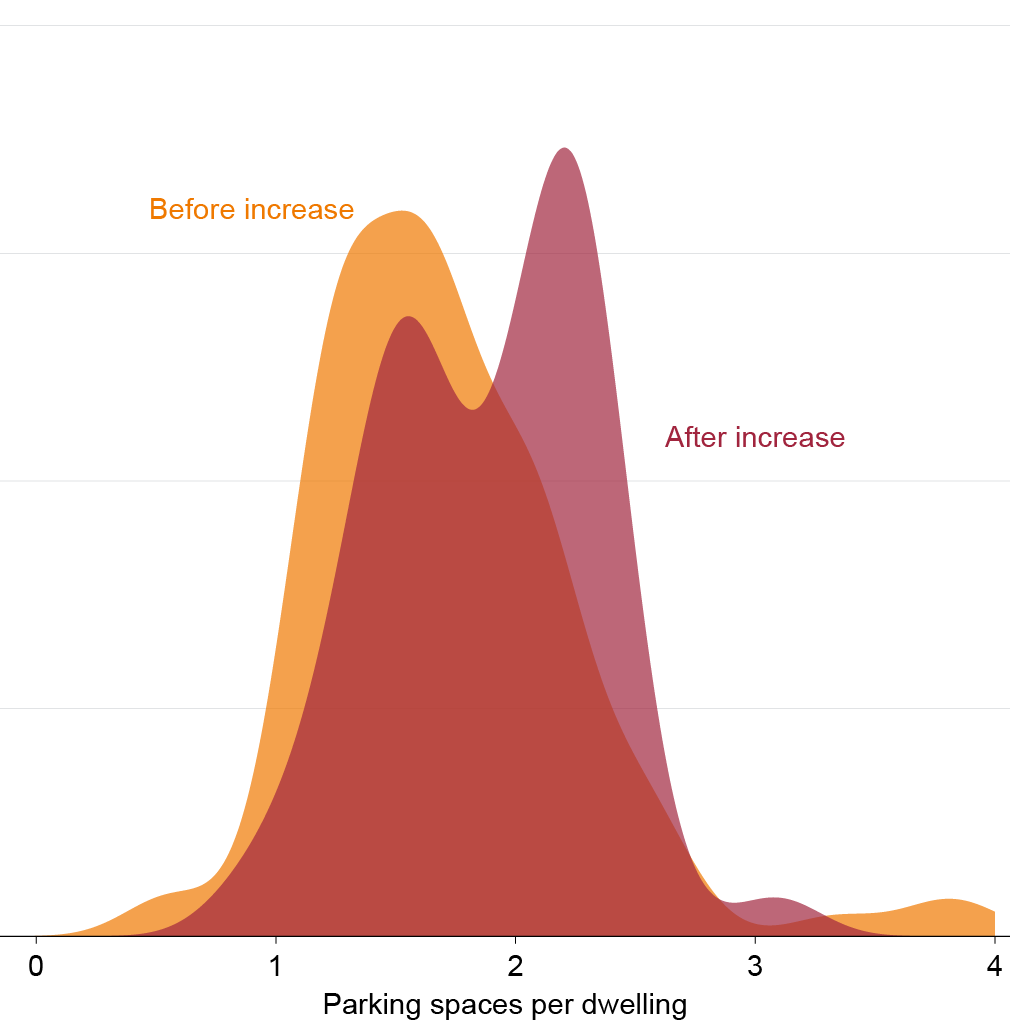

In 2019, Brisbane City Council substantially increased minimum parking requirements for apartments and townhouses across large areas of suburban Brisbane. This change has resulted in a 23 per cent increase in the number of parking spaces provided for each new home built since (Figure 1.3).

Where minimums don’t apply, developers still provide parking in response to demand, but at much lower rates. In Melbourne’s inner 10km – where public transport is generally good and car ownership is lower – apartments built since 2019 with minimum requirements provide 1.2 spaces per dwelling on average. By contrast, apartments in the same areas with no minimum requirement provide just 0.7 spaces.10Grattan analysis of Cotality (2025) and relevant planning schemes. Excludes visitor parking requirements. Where the minimum requirement is fractional (6.7 per cent of dwellings), it is rounded down to the nearest whole number.

Figure 1.3: Lifting minimum parking requirements in Brisbane led to more parking being built

Parking spaces per dwelling in areas affected by increased parking minimums

Note: Amendment J became operational in November 2019, and increased parking minimums for multiple dwelling (townhouse and apartment) projects in most suburban areas of Brisbane.

Source: The Centre for International Economics (2025).

1.3.1 Parking rules bear little relation to ownership

About 40 per cent of studio and one-bedroom apartment households in Australia’s capital cities own no car – double the rate of two-bedroom apartment households (19 per cent). And 58 per cent of three-or-more-bedroom households have just one car, or none.11Analysis covers apartments (flats in buildings of all heights) across all Australian capital cities. Studio apartments are included with one-bedroom dwellings: ABS (2021).

In Melbourne and Sydney, car ownership falls noticeably among those living closer to the city centre.12In Melbourne, 41 per cent of apartment households within 5km of the CBD have no car, compared with 15 per cent 20km or more from the CBD; in Sydney, 36 per cent compared with 18 per cent (ABS (ibid)). This is less so in Brisbane, Perth, and Adelaide, which have lower population densities in inner areas.13In Brisbane, 19 per cent of apartment households within 5km of the CBD have no car, compared with 20 per cent 20km or more from the CBD; in Perth, 19 per cent compared with 14 per cent; and in Adelaide, 28 per cent compared with 26 per cent (ABS (2021)). See also Coates et al (2025, Figure 1.8) on population density gradients across cities. But even among residents living in apartments more than 10km from a city centre, across all capital cities, 18 per cent do not own a car.

1.3.2 Minimum requirements result in a glut of vacant car-parking spaces across our cities

Minimum parking requirements push supply well above what many residents either want or need. The result is a glut of vacant spaces across Australian cities.

Across almost every local government area in Greater Melbourne and Greater Sydney, the number of off-street apartment parking spaces per dwelling exceeds the number of cars owned by the residents of those homes (Figure 1.5).14Car ownership is derived from ABS (2021) dwelling-level vehicle counts for apartments, aggregated to LGA level. Parking spaces are from Cotality property data for apartments built by 2021.

A survey of apartment residents in Perth, Melbourne, and Sydney found one in five households had more allocated spaces than cars, with larger apartments more likely to have this oversupply.15De Gruyter et al (2023).

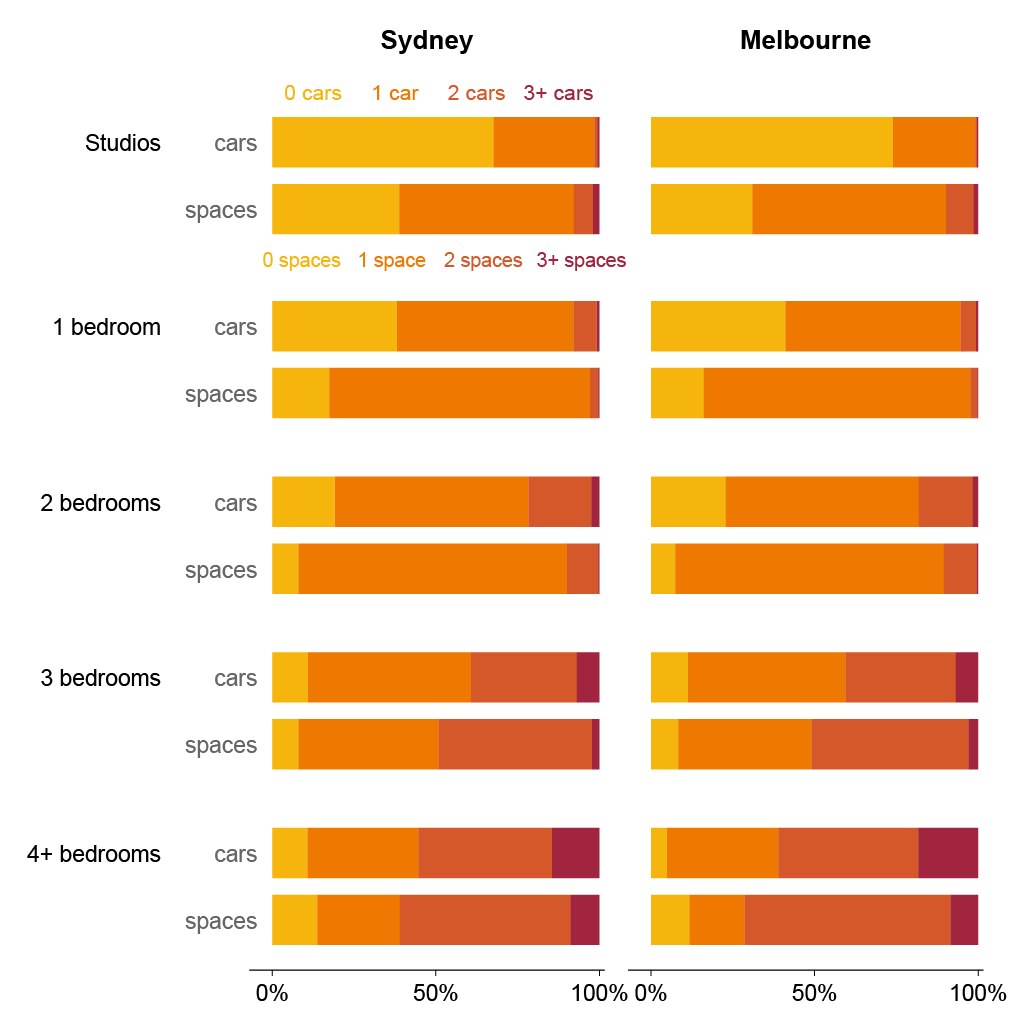

This oversupply is most acute in precisely the apartments where car ownership – and therefore the need for parking – is lowest. Most studio and one-bedroom apartments – where car ownership is lowest – include at least one off-street parking space (Figure 1.4).

The oversupply is also evident in on-street parking: across most postcodes in Australia’s five capital cities, on-street spaces outnumber registered cars (Figure 3.3).

Figure 1.4: Parking requirements force parking into apartment buildings where residents don’t need it

Distribution of car ownership and car spaces by number of bedrooms (apartments only, 2021)

Note: Parking space counts are from Cotality for year built up to 2021; car ownership counts are from the 2021 Census. Both cities are restricted to flats and units.

Sources: Cotality (2025); ABS (2021).

Figure 1.5: Across most Melbourne and Sydney local government areas, off-street apartment parking spaces outnumber residents’ cars

Ratio of off-street parking spaces per apartment relative to cars per apartment, by local government area, 2021

Notes: Average car ownership is derived from ABS Census 2021 dwelling-level vehicle counts divided by 2021 Census dwellings. Parking spaces per dwelling is calculated from Cotality property data divided by Cotality dwelling counts, filtered for built in 2021 or earlier. Covers Greater Melbourne and Greater Sydney. Excludes granny flats. We assign four vehicles exactly to all households reporting ‘four or more’ vehicles; this affects about 1 per cent of apartment households. Mornington Peninsula in Melbourne is excluded due to lack of data.

Sources: ABS (2021) and Cotality (2025).

Much of this parking sits empty. One study found that 30-to-40 per cent of parking spaces in Melbourne apartment buildings were left vacant,16De Gruyter et al (2015, Table 7). and a separate City of Melbourne study found that 25-to-41 per cent of apartment parking in the inner city is vacant.17City of Melbourne (2018).

In Brisbane, a 2021 audit of nearly 2,500 units found average occupancy rates of around 60 per cent across weekdays and weekends — meaning roughly four in 10 spaces were unused.18Riga and Ryan (2021).

And a survey of 1,300 apartment residents across Melbourne, Sydney, and Perth found that 13 per cent of surveyed households did not own a car, but most were still allocated a parking space.19Crosby (2023).

Overseas, studies regularly show that more than a third of off-street car-parking is left vacant each night.20For example, see Centre for Neighbourhood Technology (2016) for San Francisco Bay Area, Seattle, and Washington, D.C; and McCahill (2017) for Wisconsin. Table 6 in Litman (2025) provides a synthesis of this literature.

1.4 The structure of this report

Chapter 2 shows how parking rules act as a handbrake on new housing construction. Each of these spaces adds thousands of dollars to the cost of new housing – pushing up the price of homes that do get built. And they make many homes that would otherwise be commercially viable harder to build.

Chapter 3 shows why minimum off-street car parking requirements should be abolished, and state and local governments should instead use other tools – such as parking permit schemes or user pricing – to better manage on-street car-parking in high-demand areas.

Chapter 4 shows the benefits of abolishing off-street car-parking requirements for new housing, and better managing on-street car-parking. These benefits include cheaper housing, more new homes, and more walkable and better-designed cities.

1.5 What this report is not about

This report is not about off-street car-parking requirements that apply to developments other than new housing.

It is not about broader land-use planning regulations, especially zoning and other built-form controls, which affect new housing supply. Grattan Institute’s 2025 report More homes, better cities showed that allowing more homes where people most want to live will make housing cheaper and create wealthier, healthier, and more vibrant cities.21Coates et al (2025).

This report is not about reducing congestion on Australian roads beyond on-street parking. Previous Grattan Institute reports have recommended introducing congestion charging in our major cities.22Terrill (2019), and Terrill et al (2019).

And this report is not about how to arrest the decline in productivity of the housing construction sector,23Since 1994, productivity in the housing construction sector has fallen by 12 per cent, whereas productivity across the economy as a whole has increased by 49 per cent: Productivity Commission (2025). or the shortage of skilled workers needed to build more homes. Past Grattan work has identified opportunities to boost the supply of construction workers through the migration program.24Coates (2025) and Coates and Wiltshire (2024).

Box 1: Some state and local governments have begun to reform off-street car-parking rules:

In late-2025, the Victorian state government announced it would abolish minimum car-parking requirements in areas a short walk from train, tram, or bus routes with frequent service. Under the changes, new dwellings in areas deemed well serviced by public transport have no minimum parking requirement, though a maximum of two spaces per dwelling applies. Developments in areas deemed not well serviced by public transport are required to provide at least one car-park per dwelling, with no set maximums.aVictorian Government (2025b).

If these new rules had been applied to the apartments built in Melbourne between 2020 and 2025, they would have required almost 29,000 fewer car-parking spaces – a 39 per cent reduction.bGrattan analysis of Cotality (2025), Victorian Government (2025a), and Charter Keck Cramer (2025).

In NSW, several inner Sydney councils — including the City of Sydney, City of Parramatta, Inner West, Waverley, City of Canada Bay, and North Sydney — have set maximum rather than minimum parking requirements for apartments, either across the whole council area or in designated centres.

In Queensland, Brisbane City Council relaxed minimum car-parking rules for inner-city developments in March 2025. The reforms shifted from minimum requirements for off-street parking in new housing developments to maximum limits on the amount of parking permitted in the City Core precinct and reduced minimum parking requirements in the City Frame precinct, to boost housing supply and affordability in well-connected areas.cBrisbane City Council (2025) and Greater Brisbane (2024). This change reversed a 2019 move by the Council to increase minimum car-parking requirements for new housing developments.dThat change required all new apartment buildings to have two car-park spaces for all two-bedroom apartments, instead of just one: Stone (2019).

See Figure 1.6 below.

Figure 1.6: Parking requirements in Victoria decrease with better public transport accessibility

Minimum and maximum parking requirements by PTAL category in Melbourne

Note: Excludes tourist heritage railways (Puffing Billy, Mornington Peninsula and Yarra Valley) and private/industrial rail sidings. Public Transport Accessibility Level (PTAL) measures connectivity to public transport based on walking time to stops/stations, service frequency and reliability, and waiting times.

Sources: Victorian Department of Transport and Planning (2025a) and Victorian Department of Transport and Planning (2025b).

2 Car-parking requirements add to the cost of homes and prevent more being built

Car-parking minimums add tens of thousands of dollars to the cost of building new homes in our biggest cities.

For apartments, basement parking in major cities typically costs between $55,000 and $178,000 per space. Garages for townhouses typically cost between $40,000 and $137,000 per space – including the cost of the land that they occupy.

Meeting the typical requirements adds $70,000 to the construction cost of a 2-bedroom apartment in Sydney, $62,000 in Melbourne, $113,000 in Brisbane, $137,000 in Perth, and $95,000 in Adelaide. The cost of meeting minimum parking rules for three-bedroom apartments exceeds

$100,000 in most capital cities (Figure 2.1).

Residents without cars – or those who own fewer cars than they have spaces – are forced to subsidise parking they do not use. These costs fall most heavily on low-income households, people with disabilities, and older Australians who are the least likely to own a car. Many low-income households are priced out of new housing because parking minimums push rents and purchase prices beyond their reach.

These requirements also act as a handbrake on homebuilding. They reduce the housing that can practically be built on a site, especially for townhouses where parking often occupies land that could otherwise be used to construct more housing. They also push some projects below the required hurdle rate of return – meaning otherwise commercially feasible homes don’t get built at all.

2.1 Parking requirements add substantially to the cost of building new housing

Minimum car-parking requirements add tens of thousands of dollars to the cost of building new homes in our biggest cities. And the costs of satisfying minimum-parking requirements have increased sharply in recent years, in line with sharp increases in the cost of construction,25The costs of constructing new housing have risen nearly 40 per cent since 2020: ABS (2024). and may rise even further following the sharp rise in global energy prices caused by the Iran war.26Rabe (2026).

Underground parking in major cities typically costs between $55,000 and $178,000 per space (Figure 2.2). Above-ground structured parking costs $29,000–$115,000. And a residential garage costs $40,000–$137,000 (Figure 2.3).27Grattan analysis of Rawlinsons (2026), Rider Levett Bucknall (2026), Cotality (2025), and Cotality (2026). Above-ground cost range is based on RLB’s estimate of open deck multi-storey car-parks.

Minimum parking requirements often disproportionately increase the cost of homes in smaller apartment buildings. Per-space costs are higher in smaller developments, where a greater share of basement floor area is taken up by common spaces such as ramps, circulation, and driveways rather than parking bays.

Parking construction costs can be much higher in areas with rocky or contaminated ground. For example, the Committee for Sydney estimates that the cost of constructing each basement car space can be up to $250,000 in some difficult locations.28Committee for Sydney (2022, p. 12).

Digging a basement for parking can also be among the most time-consuming parts of construction. On top of construction costs, the typical 12-month timeframe for building underground parking adds $7,700 per unit in interest and taxes to a 30-unit apartment development in Sydney. In Melbourne, the extra cost can be about $4,200 per apartment.29Timeframe based on industry consultation. Costs assume a 75th percentile priced lot of between 1,000sqm and 2,000sqm developed into 30 units. See Coates et al (2025, p. 27).

In Brisbane, planning rules steer developers toward basement construction.30See Brisbane City Council City Plan 2014, Multiple Dwelling Code (s 9.3.14), AO34.1 and accompanying Note. Above-ground parking is permitted only within the footprint, behind the main building line, and if landscaped and screened. Anything over a metre tall counts as a storey, reducing dwelling height.. Basement construction costs in Brisbane can run up to $120,000 per space, and Brisbane’s variable soil conditions mean excavation carries significant uncertainty.31Rider Levett Bucknall (2026) and information provided to Grattan Institute by UDIA Queensland.

2.1.1 Parking requirements are most costly where they are least needed

Satisfying minimum parking requirements is more expensive per car space where parking is least needed.

In dense inner-city areas – where land is expensive, public transport is often plentiful, and car ownership is lowest – developers must build the most expensive parking: basement parking. Conversely, in areas on the fringe, with plentiful cheap land, developers can comply with parking requirements by providing inexpensive surface lots.32Manville and Shoup (2010).

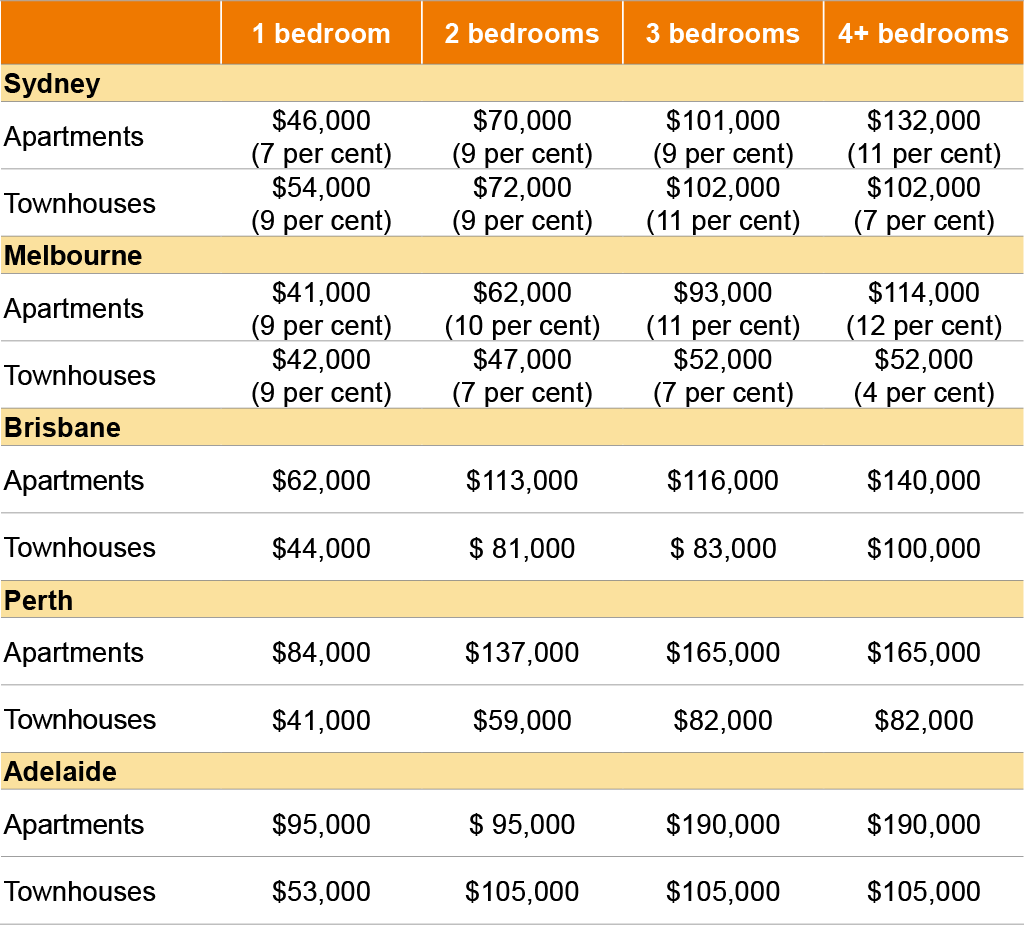

The cost of providing the average minimum level of off-street parking required in Sydney is $46,000 for one-bedroom apartments, $70,000 for two bedrooms, $101,000 for three bedrooms, and $132,000 for apartments with four or more bedrooms. Satisfying minimum parking requirements for new apartments in Melbourne costs between 11–14 per cent less than that, after recent reforms (Figure 2.1).

Figure 2.1: Meeting parking minimums adds tens of thousands of dollars to the cost of a new home

Estimated cost of meeting typical minimum requirements, (share of dwelling value)

Notes: Cost per space is the midpoint of the outside CBD construction cost range for apartments, or total cost (construction plus land) for townhouse garages (see Figure 2.2 on page 17). Multiplied by average minimum spaces required. See Appendix E in the Technical Supplement to this report for methodology on average requirements for each city. Share of dwelling value uses bedroom- and typology-specific median estimates from Cotality (2020–2025) for Sydney and Melbourne.

Source: Grattan analysis of Cotality (2025); ABS (2025a) and relevant planning data (see Appendix E in the Technical Supplement to this report).

Costs are even higher in Perth, Brisbane, and Adelaide, because minimums are typically higher, especially for larger apartments. In Perth, this is compounded by basement construction costs that are among the highest in the country.33See outside CBD costs in Figure 2.2.

The costs of constructing residential garages for townhouses are much lower – at an average of just $24,000 per space across Australia’s major capital cities – because they are built at ground level. But accounting for the value of land these garages occupy significantly increases the cost.

In Sydney, the estimated cost of a 21sqm townhouse garage (land and construction) is about $60,000 on average, rising to $137,000 in areas within 10km of the CBD. In Melbourne the average cost of a garage is about $47,000, rising to an average of $81,000 within the inner 10km. The total cost of garages in other capital cities ranges from $103,000 in Brisbane within 10km of the CBD to $44,000 beyond 20km, and about $92,000 in inner Perth, to $47,000 beyond 20km.34See Figure 2.3 for methodology.

A share of these costs is passed on to home-buyers and residents.35See Schwartz et al (2026), Table 1, for a synthesis of recent research. Infrastructure Victoria found that apartments with two parking spaces were 34 per cent more expensive than similar homes with no parking.36Infrastructure Victoria (2023a). Another recent study showed that parking mandates across US cities increased rents by 17 per cent.37Gabbe and Pierce (2017).

Box 2: Parking minimums make housing less affordable in two ways

Minimum parking requirements push up the cost of housing through two distinct channels.

First, parking is bundled into the price of new homes. Developers must plan for and build the mandated number of spaces, and recover the cost. Where buyers value those spaces at less than they cost to build – which our analysis shows is true across most of Sydney and Melbourne (Figure 2.4) – households end up paying for parking they would not otherwise choose to buy at that price. Some of this cost is passed back to landowners in the form of lower land values, and some is passed forward to home-buyers and renters through higher prices.aThe split between these channels depends on market conditions, including how responsive housing demand is to price, how easily land supply adjusts, and how competitive the development sector is. Glaeser and Gyourko (2018) show that in supply-inelastic markets, shifts in housing demand are absorbed primarily through prices rather than quantities – meaning cost increases tend to flow forward to buyers and renters rather than being offset by reductions in the housing stock.

Second, where the cost of building parking is much higher than buyers’ willingness-to-pay, some projects won’t get built at all.

In some cases, the cost of building unwanted parking can be absorbed through some combination of higher prices, lower land bids, and thinner developer margins. But where this cost pushes the project below the required hurdle rate of return, an otherwise commercially feasible project will be shelved. Fewer new homes are built, the overall housing stock grows more slowly, and prices rise across the broader market – not just for new builds.bRemoving parking mandates can make previously unviable projects commercially feasible. See Coates et al (2025) for the commercial feasibility framework.

2.1.2 The rules disadvantage low-income residents, who are the least likely to own cars

Minimum parking requirements impose costs most heavily on those least likely to benefit from them.

Car ownership rises steadily with income: from an average of 1.2 cars per household for those earning less than $52,000; to 1.8 cars for middle-income households ($52,000-to-$156,000); to 2.3 cars for those earning $156,000 or more.38ABS (2021).

Low-income households are far more likely to have no car: in 2025, about 18 per cent of Victorian households earning less than $52,000 a year had no car – six times the rate of those earning $156,000 or more (3 per cent).39Transport Victoria (2025). While many low-income families own cars out of necessity – especially in areas with limited public transport – minimum parking requirements serve them poorly. They force everyone to pay for a fixed bundle of parking regardless of how many cars they own or whether that money could be better spent elsewhere.

People with disabilities, who rely disproportionately on public transport to participate in society, are also less likely to own a car. Older Australians are also less likely to drive – license ownership falls steadily from about age 60.40Loader (2015); Bezyak et al (2017).

And minimum parking requirements typically add proportionately more to the cost of smaller apartments, which are likely to be owned or rented by people on lower incomes.41Schwartz et al (2026, p. 41).

2.2 Parking requirements act as a handbrake on new housing construction

Parking requirements reduce the amount of new housing built each year.42For example, Andersson et al (2016) estimate that minimum parking requirements in Sweden reduce the housing stock by 1.2 per cent and increase rents by 2.4 per cent. Over time, restricting the production of new housing also drives up the cost of existing housing in desirable areas, as more people compete for a limited number of homes.43See Coates et al (2025).

Minimum parking requirements can reduce the housing that can practically be built on a site, especially in inner-city areas where garages and driveways take space that could be used for housing.

In other cases, minimum parking requirements can make prospective developments infeasible. Our analysis shows the costs of providing car-parking spaces for new apartment developments often vastly exceed what new home-buyers are willing to pay for them.

Figure 2.2: Basement parking construction adds a heavy cost burden to new developments

Average cost of basement car spaces, lower and upper bound estimates

Note: Assumes basement parking for apartments.

Source: Rider Levett Bucknall (2026).

2.2.1 Australia has a shortage of housing where people most want to live

Australia has a shortage of housing. Since the turn of the century, Australia has had the second-largest decline in the OECD in the amount of housing per adult.44Coates et al (ibid, Figure 1.5). Unsurprisingly, countries – including Australia – that have added fewer homes relative to population growth have had faster growth in house prices.45Coates et al (ibid, Figure 1.6).

We especially aren’t building enough homes where people most want to live: in established suburbs of our major cities, close to jobs, transport, schools, and other amenities. Our major cities are among the least-dense in the developed world. And most of our major cities have added comparatively fewer new homes in suburbs that are between 5km and 20km from the CBD.46Coates et al (ibid, Figure 1.7).

Figure 2.3: Land costs drive the price of a garage in new townhouses – especially close to the city

Average costs of garage car-spaces, by distance from CBD

Notes: Includes both construction and land cost. Assumes residential garages (21sqm) for townhouses. Sydney and Melbourne land cost estimates are based on Grattan analysis of Cotality (2025) property valuation microdata and lot size. Estimates for Brisbane, Perth, and Adelaide are based on Cotality median dwelling value and land area data at the SA3 level. In all cases, we assume land value is 60 per cent of total property value per square metre.

Source: Grattan analysis of Rawlinsons (2026), Cotality (2025), and Cotality (2026).

2.2.2 Parking requirements directly reduce housing density

Minimum parking requirements reduce allowable housing density.47Manville (2013) found that within New York City, a 10 per cent increase in minimum parking requirements was associated with a 6 per cent reduction in both housing density and population density.

For instance, the interaction between parking requirements and planning controls, such as site coverage and floor-space ratios, can reduce the amount of housing that is permitted. Garages and carports count in Victoria towards controls such as maximum site coverage or garden area, limiting the amount of housing that can be built on a given site.48Victorian Department of Transport and Planning (2025c).

Below-ground space must also accommodate other planning requirements, such as deep planting zones and electricity infrastructure.

This interaction is especially pronounced for gentle density, such as two- and three-storey townhouses on smaller sites with limited street frontage – where ground floor area is at a premium and there is limited scope to compensate by building upward.

Minimum parking requirements can also make small or irregularly shaped parcels effectively undevelopable, by mandating more parking than can physically fit on a site.49For example, US developers subject to similar parking rules as Australia cited parking requirements as an obstacle to constructing compact, walkable developments in transit-rich areas. See Guthrie and Fan (2016).

2.2.3 Minimum parking rules make fewer developments profitable to build

Our hedonic analysis of apartment transactions in Melbourne and Sydney shows that buyers’ willingness-to-pay for basement parking is well below what it costs to build. This gap holds across all of Melbourne, and most of Sydney beyond a handful of wealthy eastern suburbs (Figure 2.4).50See Appendix B in the Technical Supplement to this report.

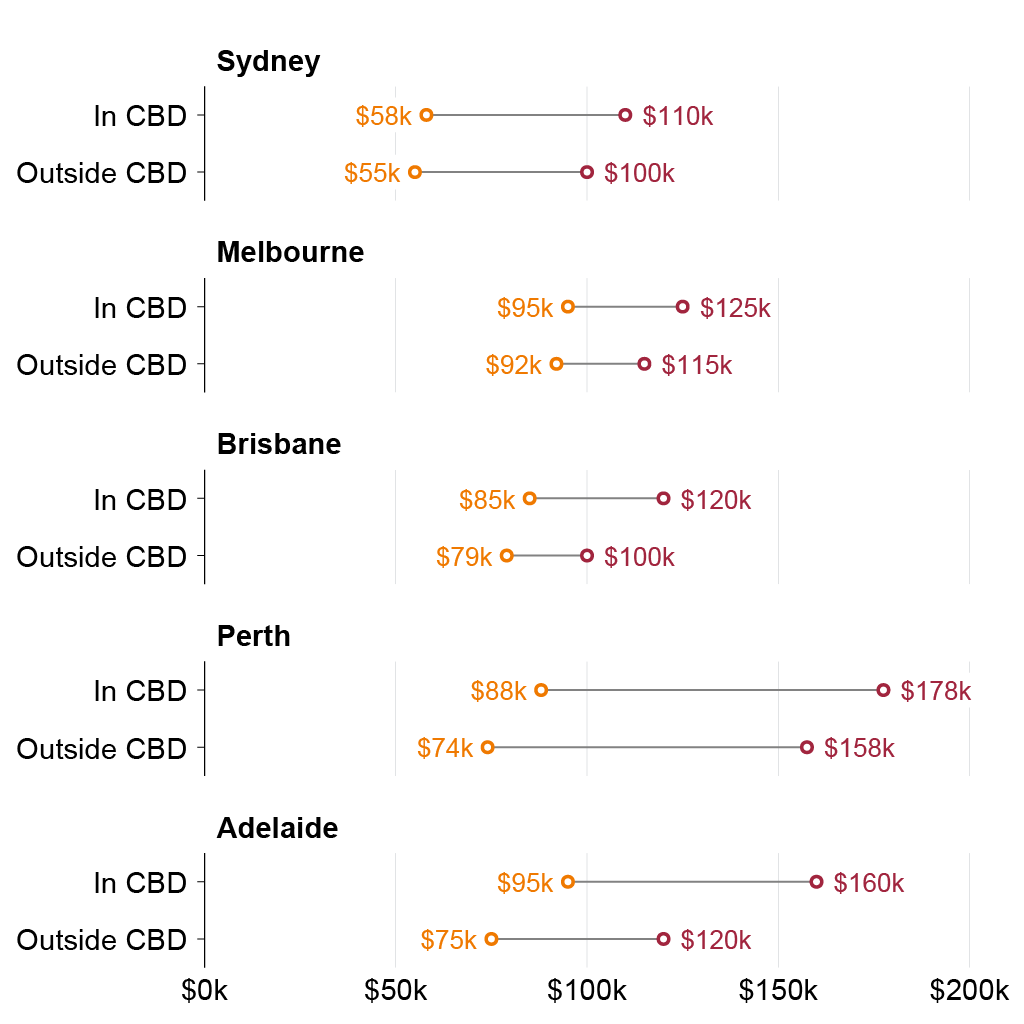

In Melbourne, the median willingness to pay for a first basement parking space ranges from about $88,000 in Bayside to just $58,000 in Melton. Willingness to pay for a second space falls to about $46,000 in Bayside and $30,000 in Melton.

Yet basement parking – the type mandated in most inner and middle-ring areas where land is constrained – typically costs between $92,000 and $125,000 in Melbourne and between $55,000 and $110,000 in Sydney (Figure 2.2).

As a result, minimum parking requirements reduce the commercial feasibility of new apartments by upwards of $40,000 for the first space across much of Melbourne – and by more than $70,000 per space where a second space is required.51See Appendix B in the Technical Supplement to this report for methodology.

In Sydney, prospective apartment buyers in a handful of wealthy inner areas – including Woollahra and Waverley – are willing to pay more for a parking space than it costs to construct, meaning parking requirements impose no hit to commercial feasibility in these locations.

But across most of Sydney, buyers’ willingness to pay for car spaces in new apartments falls well short of construction costs. In western suburbs such as Liverpool and Fairfield, willingness to pay for a parking space is only around $37,000 for the first space and $36,000 for the second – reducing the commercial feasibility of new apartments by about $40,000 per space.52Representative local government areas selected to illustrate the range of willingness-to-pay across locations. Our analysis covers 335 SA2s in Melbourne and 326 SA2s in Sydney. See Appendix B in the Technical Supplement to this report for methodology.

Figure 2.4: In most areas of Sydney and Melbourne, buyers’ willingness to pay for parking falls below construction cost

Median willingness to pay per parking space, by SA2

Notes: Statistical Area Level 2 areas (SA2s) are geographical regions defined by the ABS containing about 10,000 people each. Each dot represents one SA2. Dashed line shows the midpoint construction cost of the outside CBD estimate (Melbourne: $103,500; Sydney: $77,500). Excludes SA2s with fewer than 20 observations. Feasibility hit represents the difference between parking construction cost and willingness to pay (WTP). See Appendix B in the Technical Supplement to this report for full methodology.

Source: Grattan analysis of Cotality (2025).

In suburbs where the gap between the cost of constructing car spaces and home-buyers’ willingness to pay is widest, the first parking space reduces the commercial feasibility of new apartments by up to $46,000 per parking space in Melbourne and $41,000 in Sydney. For a 50-dwelling apartment building in these areas, this gap represents about $2 million in costs that must be recovered through higher purchase prices or rents (Figure 2.4).53Some portion of the extra cost may also be passed backwards to landowners via the developer being willing to pay less for the land in the first place.

These challenges are exacerbated by the sharp construction cost rises since the COVID pandemic. The cost of constructing new housing in Australia has risen by 36 per cent since March 2020.54Grattan analysis of ABS (2025b, Table 18). These rising costs mean fewer new homes are commercially feasible to build today.55New housing is commercially feasible to build if it is both permitted by planning controls, and profitable to build after accounting for land acquisition, construction costs and related expenses, the developer profit margin, and the final sale prices: see Coates et al (2025, Figure 3.1).

Where this gap is small enough that the project remains viable, the cost is passed on – either forward to buyers through higher sale prices, or backward to landowners through lower land bids.56The split between these channels depends on market conditions, including how responsive housing demand is to price, how easily land supply adjusts, and how competitive the development sector is. Over time, where projects don’t proceed, fewer new homes add to price pressure across the broader housing stock. But where the gap is wide enough to erode the necessary margin – particularly in lower-priced outer suburbs where margins are already thin – projects simply don’t stack up, and the homes don’t get built at all.57See Box 2.

Fewer feasible projects mean fewer homes, and in a market already short of housing, that pushes prices up for everyone.

Box 3: Car-parking rules are one reason few larger apartments are built in our cities

Three-bedroom apartments make up only a small share of apartments – typically less than 15 per cent – in Australia’s capital cities. And apartments with four or more bedrooms account for less than 1 per cent of all apartments in each capital city.aData don’t include Hobart and Darwin. Killalea and Stevens (2025). A big reason is the cost of meeting minimum car-parking requirements for larger apartments.

Minimum car-parking requirements are most onerous for larger dwellings, with many new homes with three or more bedrooms required to have up to two car spaces.bSee Figure 1.2 and Appendix A in the Technical Supplement to this report.

This burden is significant. Three-bedroom apartments in Sydney have an average minimum requirement of 1.3 spaces per dwelling – adding $101,000 to the cost of a single apartment – rising to an average of 1.7 spaces for apartments with four or more bedrooms, at an average cost of $132,000. In Melbourne, the typical three-bedroom apartment requires 0.9 car spaces, and apartments with four or more bedrooms 1.1 spaces. These parking requirements add an average of $93,000 to the cost of three-bedroom apartments, and $114,000 to the cost of apartments with four or more bedrooms (Figure 1.2 on page 8).cCost estimates use the midpoint of the outside-CBD construction cost range for basement parking in apartments, as per Figure 2.2 on page 17.

And many of these spaces are not needed. A survey of 1,316 apartment residents across Sydney, Melbourne, and Perth found that for each additional bedroom, there was a 4.6-fold increase in the odds of a dwelling having an oversupply of car-parking.dDe Gruyter et al (2023).

3 State and local governments should axe car-parking requirements for new homes

State and local governments should remove parking requirements for new homes. These requirements are intended to avoid the extra cars from new homes clogging up our residential streets. But they don’t work, and are making housing more expensive for no good reason.

In much of our cities, there is enough on-street parking that we can build more homes without parking becoming overly congested. In these locations, parking requirements are solving a problem that doesn’t exist.

And even in higher-density areas, if on-street parking isn’t well managed, people will tend to park on the street anyway. In these places, the result is both more expensive homes and more congested streets.

Better managing demand for on-street parking by giving drivers incentives to limit the amount they use is the most effective way to avoid congested streets in busy areas.

State governments should also remove barriers to allowing parking spaces to be purchased or rented separately from housing. ‘Unbundling’ car spaces from homes would give residents greater choice to purchase or rent parking in line with their needs.

The federal government should incentivise the states to remove car-parking requirements for new housing developments.

3.1 Governments should axe minimum car-parking requirements for new housing

State and local governments should abolish off-street car-parking requirements for new housing developments. Instead, home-builders should be free to supply the car-parking that home-buyers want.

Governments should, however, continue to set rules relating to a minimum number of accessible car-parks for people with disabilities.58Under the Building Code of Australia, a required number of parking spaces must be allocated as disabled car-parking. See NCC (2022).

Abolishing minimum car-parking requirements would allow developers to use scarce land in our cities for more homes, rather than parking spaces. Removing these requirements would result in less unnecessary parking being built, which would cut the cost of new housing, and boost home-building (Chapter 4).

New Zealand’s National Policy Statement on Urban Development provides a template for abolishing parking requirements. In 2020, the NZ government abolished car-parking requirements – minimums and maximums – in NZ’s largest cities. The benefits, in the form of cheaper and more abundant housing, were between 2 and 19 times greater than the costs (Figure 3.1).59PwC (2020, p. 87).

Many other cities have abolished minimum off-street car-parking requirements for new residential developments, including London, Sao Paolo, selected areas of Beijing, Austin, Atlanta, Buffalo, Boulder, Denver, Edmonton, Hartford, San Francisco, Berlin, and Hamburg.60See Yanocha and Allan (2023); Colorado General Assembly (2024); Herrick (2025); Zialcita (2025); Schwartz et al (2026); Guo and Li (2014); and Taylor (2021). Beijing, Atlanta, and Sao Paolo replaced car-parking minimums with maximums.

These experiences show that when minimum car-parking rules are relaxed or abolished, home-builders still provide parking, but only at the level that home-buyers want: well below what current regulations force them to build.61See Box 6 in Chapter 4.

They also show that the intended benefits of these parking requirements – less congested on-street parking – are small, if they exist at all. Minimum parking requirements alone don’t prevent on-street parking congestion (Section 3.3). This means that removing the rules won’t lead to parking chaos on our streets – particularly in the low-density suburbs of our cities.

Figure 3.1: The benefits of removing minimum parking requirements hugely outweigh the costs

Range of benefit-cost ratios of removing minimum parking requirements, by NZ city

Source: PwC (2020).

3.2 In many parts of our cities, there is ample street parking

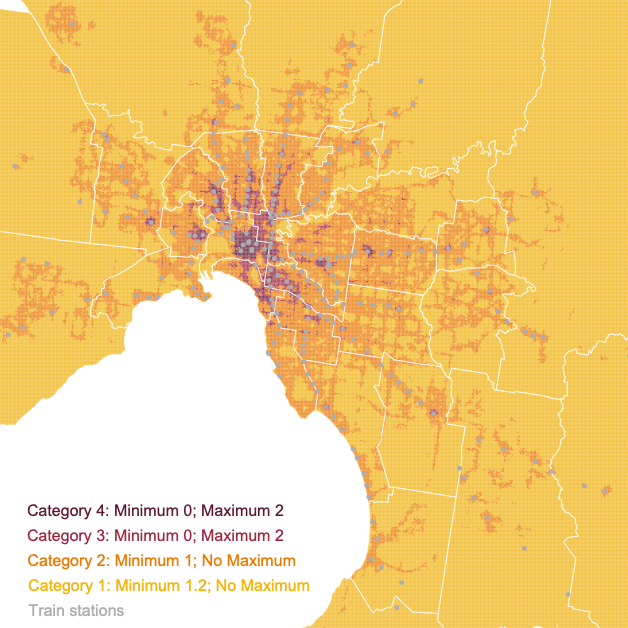

Across much of our cities, there is enough parking that even if new homes are added to an area, streets won’t fill up. Less than a third of street parking spaces in inner Brisbane are typically occupied, and outside of the inner-city, most streets sit largely empty (Figure 3.2).

In these areas, parking is abundant enough that additional housing won’t cause congestion. For example, we estimate that within 10km of the Brisbane CBD, there are about 3,000 streets that could accommodate six additional townhouses – without parking garages – while still leaving more than three-quarters of the street’s parking empty, even with everyone parking on the street.

Figure 3.2: Two-thirds of street parking spaces in inner Brisbane are typically unoccupied

Notes: Point-in-time estimate of on-street parking utilisation using machine learning analysis of aerial imagery. Weekend imagery used to maximise the likelihood of cars being at home. Nighttime occupancy estimated by uprating daytime occupancy by estimates of the share of vehicles away during the day. Parking capacity estimate from Brisbane City Council parking signs and lines data. See Appendix D in the Technical Supplement to this report for details.

Source: Grattan analysis of Brisbane City Council (2026a) and Nearmap (2026).

Where there is lots of parking, minimum parking requirements are unnecessary. Where parking is congested, they don’t help. In all of these areas, they should be abolished.

Forcing residents of new homes to pay for a car-space they don’t want, even as they park on the street anyway, is the worst of both worlds: fewer, more expensive homes and congested streets.

Studies from the Netherlands, UK, and US show that where free on-street parking is available, many households use their off-street parking spaces for other purposes, such as storage, with garages used for car-parking only about half the time.62Scheinar et al (2020).

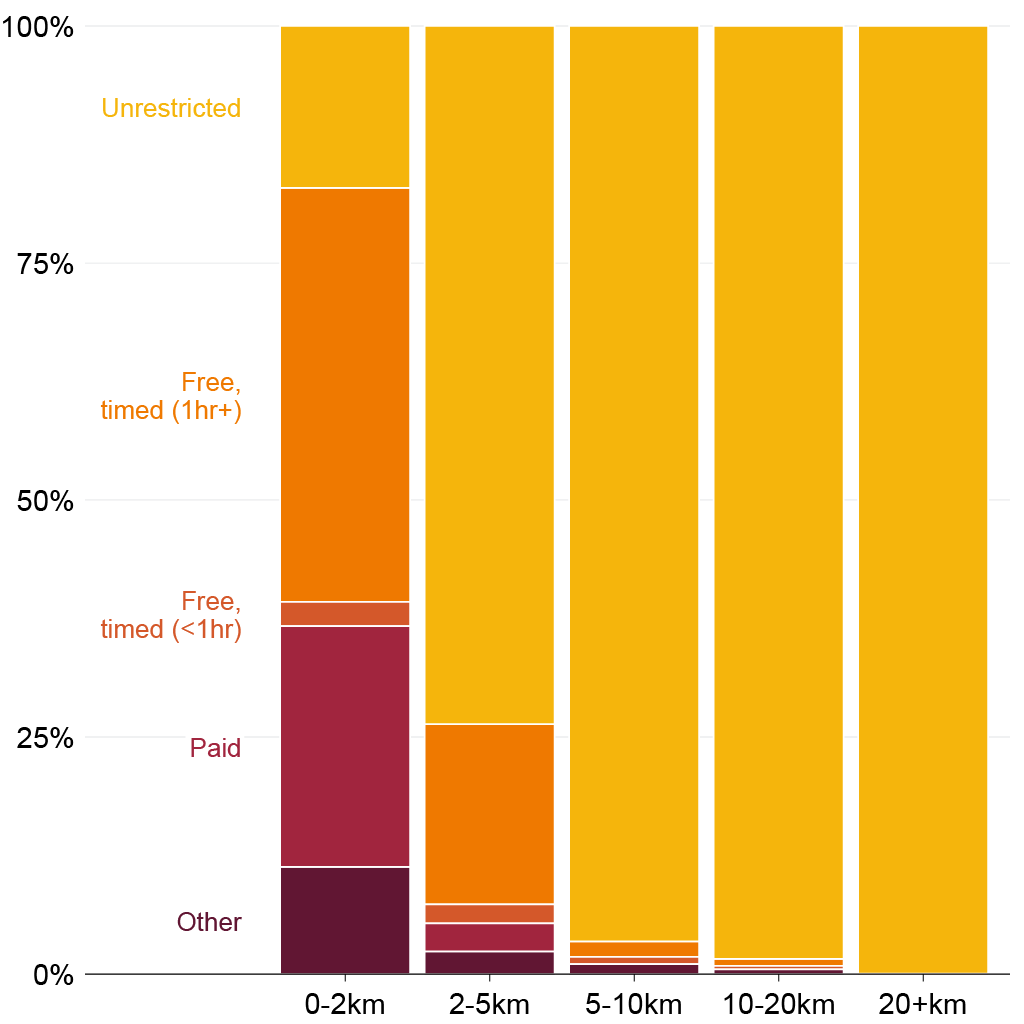

On-street parking is free and has no time limits in most areas of our capital cities. In Brisbane, for example, outside of the inner-most suburbs, the overwhelming majority of on-street parking is unrestricted (Figure 3.4 on page 26).

This is because without measures to better manage on-street parking, both new and existing residents have little incentive to not park on the street, even if they have their own off-street space.

In areas where parking can become congested, parking minimums mostly don’t achieve their aim of preventing congestion.

Figure 3.3: In many areas of our cities, there are many more on-street parking spaces than cars

On-street parking spaces per registered car, by postcode

Notes: Includes only passenger and light commercial vehicles (vans and utes). Excludes parking spaces that are unavailable for regular use (such as loading and taxi zones). Detailed analysis undertaken for Brisbane and extended using modelled street length ratios to other cities – see Appendix D in the Technical Supplement to this report for details.

Sources: Grattan analysis of Brisbane City Council (2026a), OpenStreetMap (2025), Transport for NSW (2026), and BITRE (2025).

3.3 In higher-density areas, parking requirements often don’t achieve their aim

This means most residents in places such as Sydney’s upper North Shore, Melbourne’s western suburbs, and Brisbane’s Bayside, would see little change in their ability to park even if extra housing were built in their street (Figure 3.3).

This is the case across much of our capital cities. Outside the inner city in Perth and Adelaide, and middle-ring suburbs in Sydney, Melbourne, and Brisbane, there is more on-street parking than there are registered cars (Figure 3.3). In much of these areas, even if everyone parked on the street, there would still be enough parking to go around.

Figure 3.4: Almost all on-street parking in Brisbane is unrestricted

Share of on-street parking spaces, by distance to the CBD

Notes: Distances calculated from Roma Street station. ‘Other’ includes loading zones, taxi zones, and dedicated accessible parking. St Lucia traffic area counted as timed, but restrictions only apply from February to November. Otherwise, unrestricted parking spaces with event-day restrictions marked as unrestricted.

Source: Grattan analysis of Brisbane City Council (2026a) – see Appendix D in the Technical Supplement to this report for details.

3.4 Modest regulations can prevent street parking from becoming congested

Parking minimums don’t prevent congestion. Instead, when street parking starts to fill up, local governments should introduce residential parking permit schemes.

These schemes, which set time limits for parking and provide residents with a limited number of permits exempting them from these rules, can be highly effective, by discouraging people who don’t need to park on the street from doing so.

These schemes work: an evaluation of residential parking permit schemes in Berkeley, California, found that after their introduction, there was at least one available space on every block 98 per cent of the time.63Moylan et al (2024).

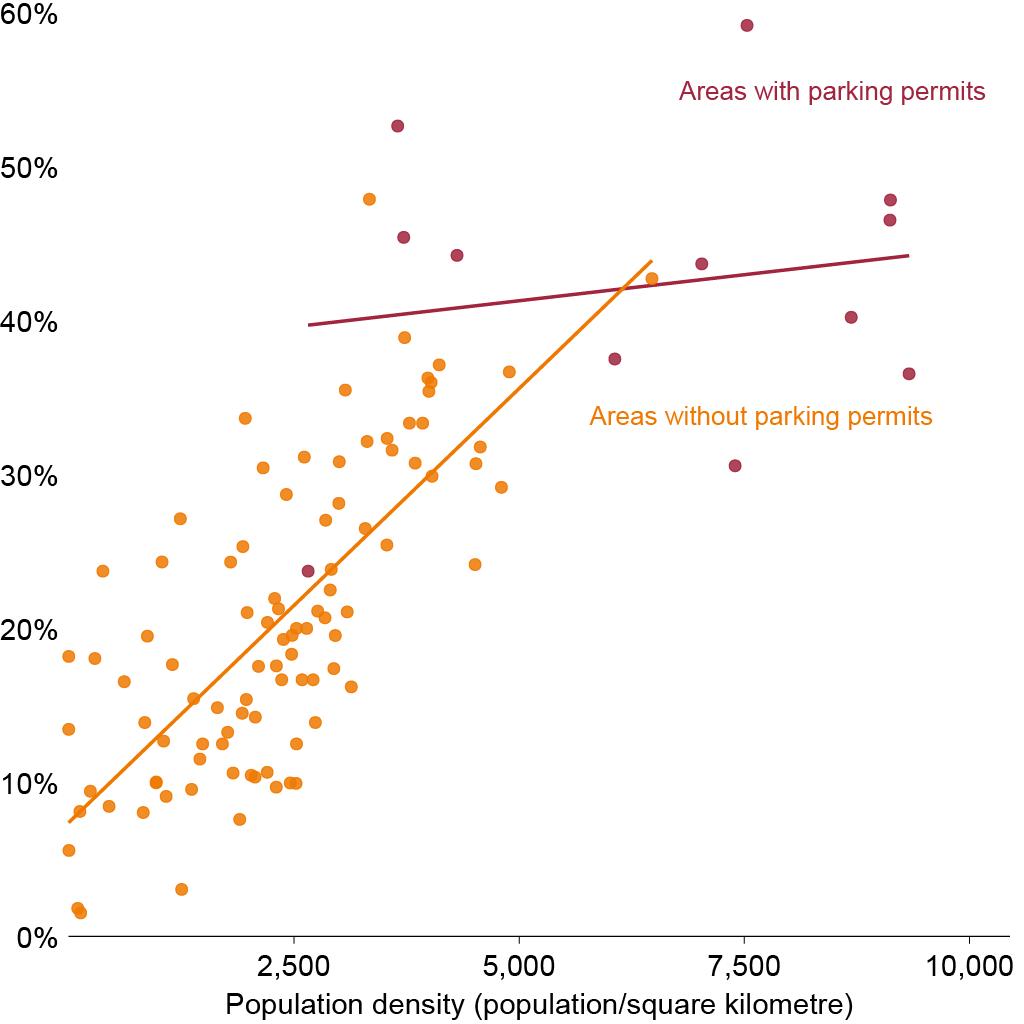

Once the population density of a suburb rises above about 3,000 people per square kilometre – such as in Gordon in Sydney, Burwood in Melbourne, and Sunnybank Hills in Brisbane – there are typically fewer on-street spaces than there are registered cars (Figure 3.3). In these areas, street parking may start to become congested, and permit schemes should be considered.64In Brisbane, street parking utilisation rises sharply with density in suburbs without permit schemes; in permit-scheme suburbs, utilisation stays broadly stable as density increases (Figure 3.5).

This is already happening. More than 90 per cent of suburbs in Sydney with a population density of more than 3,000 people per square kilometre have some form of permit scheme, compared to only 21 per cent of less-dense suburbs (Box 4).

Most parking permits are offered to residents for free, or are priced cheaply, at typically less than $100 a year. In moderately dense areas, low-cost permit schemes can work well.

But as on-street parking becomes especially scarce, offering permits so cheaply is unlikely to effectively manage demand. In these areas, the price of permits should rise to reflect demand.

Increasing the cost of on-street parking permits also provides an incentive for developers to provide off-street parking spaces when building new housing in that suburb – as long as there is demand for them.

Parking permit schemes in areas with high demand for street parking are potentially a valuable source of revenue for local councils.

The revenue from parking permit schemes – above the cost of administering them – could be reinvested in the local community to fund new street trees, local road and footpath maintenance, playgrounds, safe crossings at parks and schools, or improved public transport infrastructure such as bus shelters.65For example, Shoup (2024) proposed the establishment of Parking Benefit Districts, where revenue from on-street parking is ‘ring-fenced’ to the local area, so residents see the money invested in their local area.

In addition to permit schemes, a broader set of tools can help mitigate parking pressure. Reserving street space for car-share services, providing bike parking, and installing public charging stations for electric cars all reduce the need for off-street space.66Committee for Sydney (2022).

3.5 State and local governments should encourage ‘unbundling’ of car-parking from housing

Many residents are paying for parking spaces they don’t use or want. The total value of this unused off-street car-parking in Sydney, Melbourne, and Perth, by one estimate, exceeds $6 billion.67Zheng (2023). At the same time, if someone does want more parking than they currently have, it can be difficult to source.

Figure 3.5: Parking permits can help ease the pressure on street parking as cities grow

Utilisation of street parking by SA2, Brisbane City Council

Notes: SA2s are geographical areas defined by the ABS containing about 10,000 people each. 75th percentile of utilisation for each SA2 shown. Area marked as

having parking permits if at least 50 per cent of its area is covered by a permit scheme. Excludes event-day parking areas.

Source: Grattan analysis of Brisbane City Council (2026a), ABS (2025c), and Nearmap (2026) – see Appendix D in the Technical Supplement to this report for details.

‘Unbundling’ parking – allowing residents to pay for parking spaces separately from their unit – would help to address this mismatch. Giving residents choice over the amount of parking they want to pay for would result in savings for residents who don’t want a parking space.

Research on buildings in Los Angeles converted under the Adaptive Reuse Ordinance found that bundled parking increased apartment asking rents by about US$200 per month.68Manville (2013). Similarly, a study using national American Housing survey data found that the cost of garage parking to renter households is about US$1,700 per year, or an additional 17 per cent of a housing unit’s rent.69Gabbe and Pierce (2017).

A survey of Melbourne apartment residents found that 42 per cent were receptive to the idea of unbundling – and residents with two or more cars were three times more likely to be receptive than those with one, probably because unbundling enables people to purchase additional spaces if they want to.70De Gruyter et al (2024). Designed well, unbundling can give residents the same choice over parking as they already have over bedrooms.

Unbundling can also help make the most of existing spaces, reducing the pressure on on-street parking. By allowing people who need more parking to get it, families with multiple cars won’t need to compete for street parking.

Some developers already offer a partial form of unbundling – Melbourne Square in Southbank, for example, sold parking separately from apartments off the plan. Without parking minimums, this could be expanded to allow buyers to purchase only the spaces they want.

A handful of other recent Australian developments have also adopted some form of unbundling, including Indi City Sydney, and Arklife Brisbane.71Zheng (2023).

However, unbundling can be difficult to implement. Strata schemes are already complex legal instruments, and unbundling requires either introducing separate lots for parking spaces, the owner’s corporation maintaining ownership of all parking spaces, or sub-leasing the parking component of the building to a third party operator. All of these options would add substantial complexity for developers and residents. And some banks appear reluctant to lend to home-buyers purchasing an apartment without a dedicated parking space.72Car spaces are often included in calculations for banks’ criteria for minimum apartment sizes: Astbury (2025).

For this reason, successful examples of unbundling overseas have generally been in locations where most or all apartment buildings are owned by a single entity. In California, for example, where several cities have successfully implemented unbundling (Box 5),73Committee for Sydney (2022). only 3 per cent of new housing is strata-titled units.74Formally, condominiums, the US equivalent of strata-titled units Fulton (2025).

Unbundling is most likely to be successful in Australia in the nascent build-to-rent sector, where institutional investors are more able to manage the legal and financial risks associated with unbundling. This is already beginning to occur: Indi Southbank, a 434-unit build-to-rent building in central Melbourne, offers parking spaces separately to units for an additional fee.75Unilodge (2026). And build-to-rent projects tend to have far fewer car spaces per home.76Build-to-rent developments in NSW, Victoria, and Queensland have an average car-space-to-unit ratio below 0.5 – one car-park for every two units: Bleby (2025).

State, territory, and local governments should support the unbundling of parking spaces from new homes via:

- Reforming model strata by-laws to prevent them banning sub-letting of parking spaces.

- Removing barriers to the development of dedicated parking buildings in new high-density areas, to give residents of new apartment buildings the ability to buy or lease a parking space nearby, rather than needing a dedicated space in their own building.

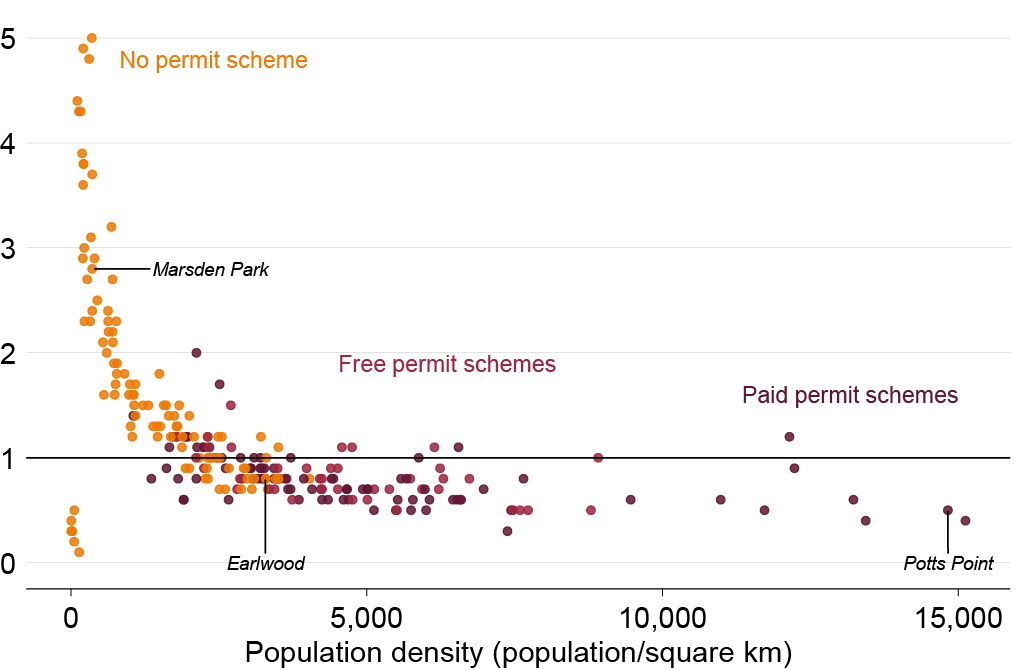

Box 4: Many councils in Sydney have introduced residential parking permit schemes to better manage on-street parking space

Where Sydney councils have introduced residential parking permit schemes, they tend to do so once there is about one on-street parking space for each registered car, or less, in a postcode. This tends to happen when population density reaches about 3,000 people per square kilometre (Figure 3.6).

– Access is modestly limited for those with off-street parking: Most councils limit the number of permits offered to houses with off-street parking, generally allowing one car to be parked on the street in addition to the off-street spaces available. In high-demand, high-density areas of the City of Sydney, such as Potts Point, no permits are issued to any household with an off-street space.

– Fees are low, if applied at all: Transport for NSW guidelines permit councils to charge only for the cost of operating the scheme – rather than charging a price that reflects the value of the permit. Many councils offer permits for free. And paid schemes are cheap, costing at most about $100 a year.

– Permits are often not available to residents of new apartments: Apartments built recently are often ineligible for permits. For example, the City of Sydney (1996), Willoughby (1998), the Inner West Council (2001), Randwick (2013), and Bayside (2016) have introduced restrictions.

See Figure 3.6 below.

Figure 3.6: Parking permit schemes make sense in denser suburbs

On-street parking spaces per registered car, Sydney, by postcode

Notes: Postcode identified as having a parking permit scheme if it contains a suburb covered in part by a scheme. Cars include passenger and light commercial vehicles (vans and utes). Detailed analysis on parking spaces undertaken for Brisbane and extended using street length ratios to other cities – see Appendix D in the Technical Supplement to this report for details.

Sources: Grattan analysis of Brisbane City Council (2026a), Transport for NSW (2026), BITRE (2025), and assorted local council documents.

3.6 Maximum car-parking restrictions for new homes should also be abolished

Maximum parking restrictions should be axed for the same reason that minimums should be axed: home-buyers know better than planners how much parking they need, and should be free to choose the parking that fits their varied needs.

For example, in Sydney, Waverley council effectively bans parking for new studio apartments.77The Waverley Development Control Plan 2022 sets a maximum of 0 for studio apartments in medium- and high-density residential areas: the areas where apartment development is generally permitted. But if someone wants to buy a new studio in Waverley with a parking space, they should have the option to do so.

In cases like this where maximums are substantially below the level that would be demanded, they prevent residents from accessing parking that they are happy to pay for. This can reduce the feasibility of new homes – lowering supply and increasing prices. The areas where this is most likely to harm development are also where new housing would deliver the most benefits (Figure 2.4).

As Grattan Institute has previously recommended, charging drivers a modest fee is a better way of managing busy urban roads and discouraging car use in dense neighbourhoods.78Terrill (2019), and Terrill et al (2019). Charging drivers a low rate at peak periods creates a freer-flowing road, benefiting all commuters, as shown following the introduction of congestion charging in New York City.79Komanoff (2026).

Box 5: Many US cities have unbundled parking from new homes

Several US cities require developers to ‘unbundle’ parking from the price of a unit – giving residents the option to rent or buy parking spaces, but also the choice to save money by not having a parking space.aSee Committee for Sydney (2022).

In 2006, San Francisco mandated unbundled parking for all new residential developments with 10 or more dwellings. San Francisco apartment residents with unbundled parking and car-share own on average 0.76 cars, whereas apartment residents with bundled parking and no car-share own on average 1.03 cars.bCapital City Development Corp Boise (2011).

In 2015, Santa Monica mandated unbundled parking in specified zones for all new residential developments with four or more dwellings, all new residential conversions with 10 or more dwellings, and all non-residential developments.

In 2016, the City of Oakland mandated unbundled parking for all new residential developments with 10 or more dwellings, except for affordable housing developments.

The cities of San Diego and Berkeley unbundled parking for most new multi-dwelling residential developments in 2019 and 2021 respectively.

And in 2021, the Californian Government legislated unbundled parking for major infill developments.cSee Nemeth (2023).

3.7 The federal government should reward states that make these reforms

The federal government has a clear imperative to encourage the states to abolish mandatory parking rules for new housing.

First, abolishing minimum parking requirements would boost economic growth, lift construction sector productivity, and improve housing affordability (Chapter 4).

Second, the Commonwealth is uniquely positioned to solve the coordination problem between states. Because the housing market is national, increased supply in one state provides price relief everywhere. By removing wasteful requirements – such as forcing developers to build unwanted car-parks – the construction sector would be freed up to build more homes.

Third, a larger economy driven by abundant housing would generate extra tax revenue. We estimate that removing minimum parking requirements could increase the size of the Australian economy by up to $1 billion (Chapter 4). Past Grattan Institute research found that boosting population density in our biggest cities by 10 per cent could lift Australians’ incomes by up to $5 billion a year by 2050.80Coates et al (2025, p. 48). This translates to up to an extra $1 billion a year in federal tax revenue, of which roughly $200 million would flow back to the states via the GST.81Coates et al (ibid, p. 65).

Fortunately, a ready-made vehicle exists for the Commonwealth to drive this reform.

3.7.1 National Competition Policy should be extended to abolishing parking rules

The federal government can encourage the states to relax or abolish minimum parking requirements by extending the National Competition Policy to cover residential land-use planning.82Alternatively, payments could be made via a separate Federal Financial Agreement on housing between federal and state governments.

States that have already made meaningful reforms, such as Victoria, should receive ‘top-up’ payments in recognition of their progress, provided they commit to the further reforms outlined in this report. By rewarding early movers while pushing laggards, the Commonwealth could ensure a consistent national approach.

The scale of these payments could be determined based on the boost to GDP, and thus to federal tax revenues, expected from the reforms. Alternatively, payments could be benchmarked to the increase in commercially feasible housing capacity, as outlined in Chapter 4.83See also Coates et al (2025, Chapter 5).

The National Competition Council should monitor whether states have enacted and enforced these reforms consistent with the National Competition Policy framework.

4 Axing car-parking rules would cut house prices and boost home-building

We estimate that abolishing minimum car-parking requirements would avoid the construction of 86,000 unwanted car spaces across Australia over the next five years. The total cost of these avoided car parks over that period – spaces that will not need to be dug, poured, waterproofed, lit, and ventilated – is about $5.2 billion.

This reform would make new homes cheaper to buy. Abolishing minimum parking requirements would let buyers opt out of unwanted car spaces – saving about $66,000 in Melbourne and $52,000 in Sydney on a first parking space. Buyers of larger apartments, where minimums often mandate more than one space, would save even more.

No longer building car-parking that residents don’t want, or need, would boost the number of homes built in infill projects and free construction sector capacity to build an extra 9,000 homes nationwide over the next five years. And it would make more homes commercially feasible to build.

4.1 Abolishing off-street parking requirements would result in fewer car parks being built

Abolishing off-street car-parking requirements for new housing would result in fewer car parks being built as part of new housing developments (see Box 6).

We estimate that abolishing minimum car-parking requirements across Australia would reduce the number of car spaces built as part of new housing developments by 86,000 spaces over five years, including 42,000 in NSW, 10,000 in Victoria, 20,000 in Queensland, 4,000 in Western Australia, 5,000 in South Australia, and 4,000 in the ACT.84See Appendix E in the Technical Supplement to this report for methodology on estimating typical minimums.

4.2 Abolishing parking rules would save home-buyers thousands

Reducing the number of wasteful car parks built as part of new housing developments would reduce the cost of buying a new home.

Buyers who don’t want a car park are currently forced to pay for one, bundled into their purchase price. Abolishing minimum parking requirements would let these buyers opt out – saving them about $66,000 in Melbourne and $52,000 in Sydney on a first parking space alone.

These savings are largest for buyers of larger apartments, where minimum requirements often mandate more than one car space.85See Appendix A in the Technical Supplement to this report. A buyer of a larger apartment who wants no parking could save the value of both spaces – about $101,000 in Melbourne and $104,000 in Sydney. Even a buyer who wants one space but not a second could still save about $35,000 in Melbourne and $52,000 in Sydney.

In higher-priced suburbs, such as Bayside in Melbourne, buyers currently pay about $88,000 for a first car space; in lower-priced outer Melbourne suburbs such as Melton, about $58,000.

For townhouse buyers, savings are measured differently – since garages are built at ground level, the cost includes the land they occupy. And the cost savings become larger in inner-city areas where land costs are higher (see Figure 2.3).

Box 6: Fewer off-street car-parks are built when minimum parking rules are abolished

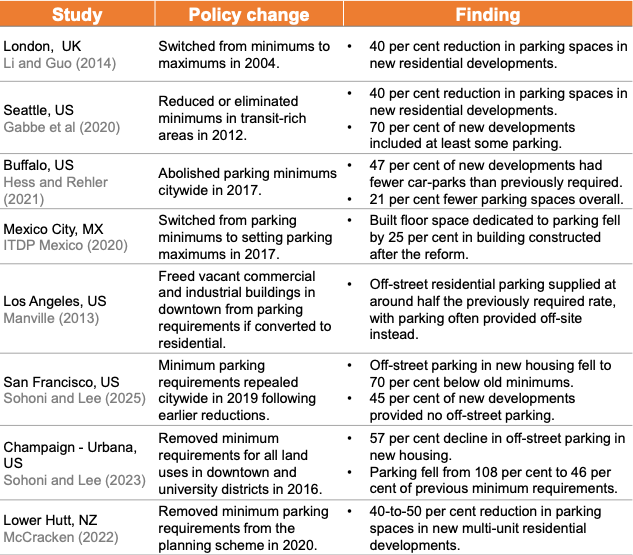

Experience abroad shows that when parking minimums are relaxed or removed, home-builders provide far less parking than the rules required.

Without mandates, developers can better respond to buyer demand: some projects include parking for car-dependent buyers, others offer little or none, with prices reflecting those choices.

When cities such as London,aLondon also established parking maximums, but they explained only 2 per cent of the decline in new parking supply: Guo and Li (2014). and Seattle, Los Angeles, and Buffalo in the US, removed minimum parking policies, new residential developments included parking at about half the rate previous policies required. In other cities, such as San Francisco, there was an even larger fall in the number of spaces built once parking rules were abolished (Figure 4.1).

The declines in the amount of off-street parking provided were typically greatest in inner-city areas with the best access to alternative transport options. For example, in inner London, new developments provided 67 per cent fewer spaces than comparable projects before the reform, whereas in outer London the decline averaged 32 per cent.bGuo and Li (ibid). Similarly, after San Francisco and Buffalo eliminated requirements citywide, reductions in new parking provision within their core areas were 1.5-to-1.9 times greater than in other parts of the cities.cSohoni and Lee (2026).

Figure 4.1: Cities that abolish parking rules build fewer car parks

Note: Excludes reforms in cities that solely cover the central business district.

Sources: Guo and Li (2014); Gabbe et al (2020); Hess and Rehler (2021); Yanocha and Allan (2023); Manville (2013); Guo (2013); McCracken (2022); Sohoni and Lee (2023).

4.3 Abolishing car-parking requirements would make more new housing commercially feasible to build

Parking requirements don’t just raise the cost of new homes, they reduce the number built. By consuming scarce land, locking out otherwise viable sites, and adding months to construction timelines, mandatory parking suppresses housing supply.86Most new housing is built by private developers. These developers need to earn a profit for a project to be commercially feasible to build, and they need to show they can make a profit beforehand to secure finance for the project: see Coates et al (2025, Section 3.2).

Where parking adds more to construction costs than buyers are willing to pay, it can be the decisive factor tipping an otherwise viable project into unprofitability.87See, for instance, Rollet (2025).

On constrained inner-city sites, where excavation is particularly difficult, costs can reach $250,000 per space – making parking requirements the decisive factor in whether a site gets developed at all.88Committee for Sydney (2022, p. 12).

These costs aren’t only financial. Basement excavation can add months to an apartment build,89The typical apartment building takes a little over two years to build (ABS (2025d)), and larger apartment developments with multiple basement levels even longer (Sharam and Bryant (2026, Figure 5)). and time is expensive: speeding up townhouse construction by six months lowers the cost per home by about $18,700.90Coates et al (2025, p. 28).

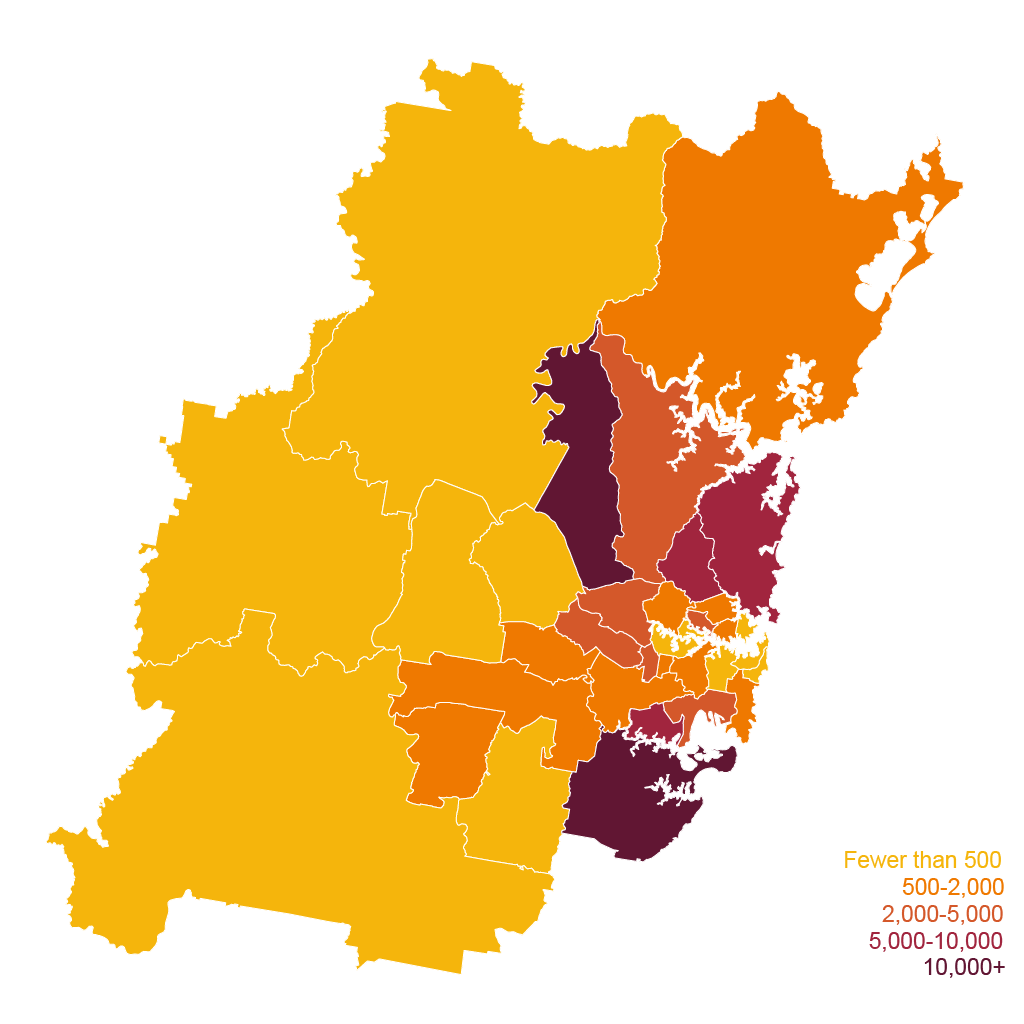

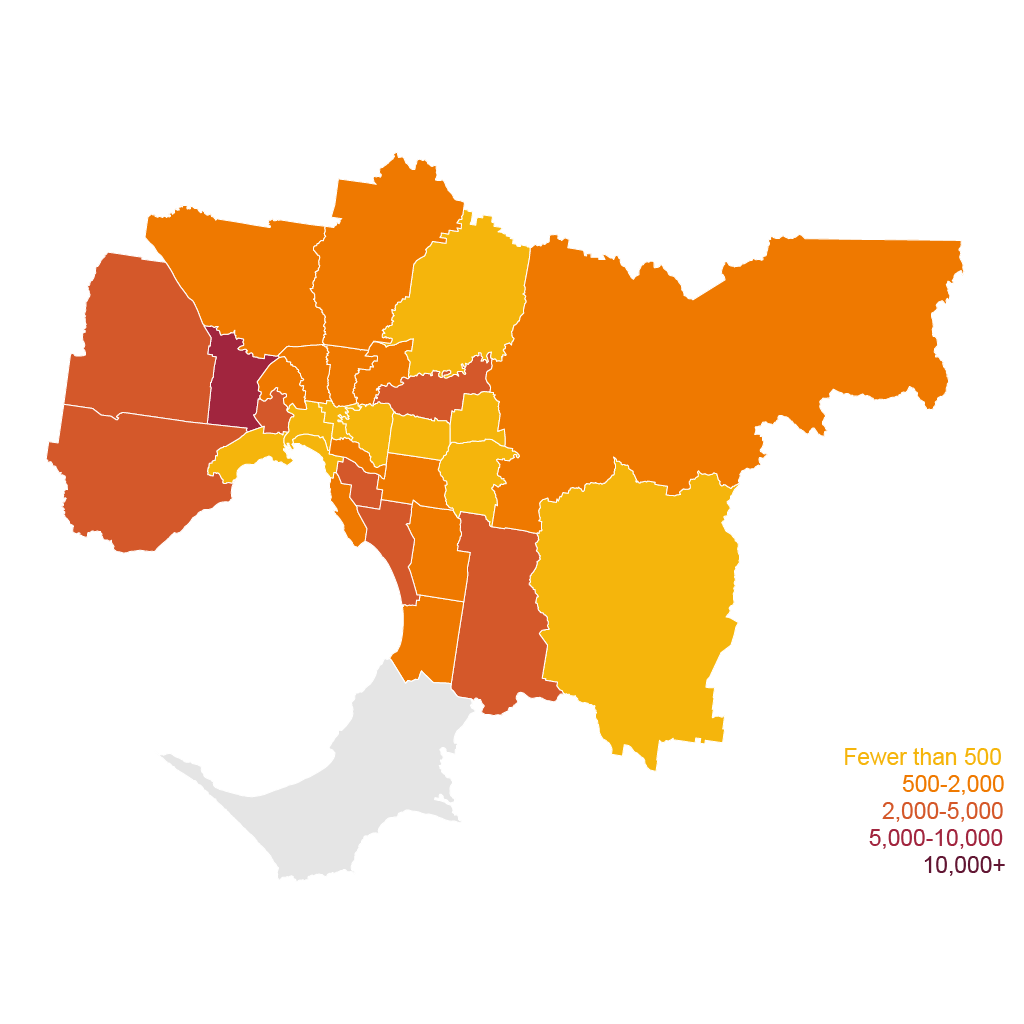

Our modelling shows that removing parking requirements for resident parking alone could make about 140,000 more dwellings commercially feasible to build in Sydney and Melbourne today (Figures 4.2 and 4.3).91See Appendix C in the Technical Supplement to this report for methodology.

Figure 4.2: In Sydney, our parking reforms would unlock the most homes beyond the inner city

Additional dwellings commercially feasible under Grattan’s parking reforms, by local government area, Sydney

Notes: Apartments and townhouses. Based on the Grattan Model of Australian Planning Systems (GMAPS) feasibility modelling comparing current parking requirements to a scenario with no parking requirements. See Appendix C in the Technical Supplement to this report for the full methodology.

Figure 4.3: In Melbourne, feasibility gains would be concentrated in middle and outer suburbs

Additional dwellings commercially feasible under Grattan’s parking reforms, by local government area, Melbourne

Notes: Apartments and townhouses. Based on the Grattan Model of Australian Planning Systems (GMAPS) feasibility modelling comparing current parking requirements to a scenario with no parking requirements. See Appendix C in the Technical Supplement to this report for the full methodology. Mornington Peninsula excluded due to lack of data.

4.3.1 Abolishing car-parking requirements would unlock industry capacity to build more housing

Australia’s construction sector is running near current capacity. Construction costs have increased by nearly 40 per cent since 2020, and construction timeframes have increased by 50 per cent from 2019 to 2024.92ABS (2024).

With workers and materials already stretched across the sector, every worker employed to build parking spaces that will sit empty is one who isn’t building the homes we desperately need. And reducing demand for scarce inputs such as steel, concrete, and timber can ease cost pressures across the sector.

Abolishing minimum parking requirements would reduce the number of off-street car spaces built over the next five years by 86,000, freeing up $5.2 billion in construction sector capacity, and up to 5,000 construction workers. If the workers, equipment, and materials used to build these parking spaces were deployed elsewhere, they could build more than 9,000 extra homes over five years (Figure 4.4).

4.3.2 Abolishing parking rules would boost construction sector productivity

Productivity in the housing construction sector has fallen by 12 per cent since 1994, whereas productivity across the economy as a whole has increased by 49 per cent.93Productivity Commission (2025) and Wilson and Brooks (2025).

Reducing the number of wasteful car parks built as part of new housing developments would help to reverse this decline. Not building parking that residents don’t want or need, and reallocating those resources to more valuable forms of construction, could lift the productivity of Australia’s residential construction sector by about 1 per cent.94Multi-factor productivity treats reduction in parking as a Hicks-neutral cost shifter: see Appendix F in the Technical Supplement to this report. This could increase GDP by up to $1 billion each year.

4.4 Less car-parking makes for better streets and cities

Fewer car-parks would make our cities better, with livelier streets, more productive economies, and a higher quality of life.

The parts of our cities with the least parking – the dense urban cores – are the most in-demand places to live.95For instance, newly built units within 5km of the centre of Sydney trade at double the rate (nearly $15,000 per square metre) of those 25km out ($7,000 per square metre): Coates et al (2025, p. 14). When there is less parking and fewer cars, vibrant urban life has room to emerge. The things that make a great street – shops, restaurants and cafes, footpaths that are safe and enjoyable to walk down – are all limited when we require too much parking.96Gehl (2010).

Off-street parking requires driveways; every driveway means cars crossing footpaths and less space for trees or outdoor seating, shade, and landscaping. That makes walking less safe and detracts from the amenity of the street. By requiring too much parking, we get ground floors lined with roller doors instead of the shops, restaurants, and cafes that make streets worth walking down.

In Melbourne, Nightingale 2 – a 20-apartment development next to Fairfield station, 7km north-east of the CBD – shows what is possible. With no parking requirement, the ground floor became a bar, ice creamery, and shops, bringing the street to life.

After off-street parking minimums were eliminated in Champaign in the US, the share of developments with active frontages increased from 43 per cent to 81 per cent. On average, buildings with active frontages provided 56 per cent of the previously required parking.97The study’s authors defined active frontages as those occupied by uses other than parking — such as residential units, patios, gyms, or retail spaces. See Sohoni and Lee (2023).

The same density that makes streets livelier also makes cities more productive. Cities are economic engines. Cities generate productivity gains through agglomeration – clustering workers and firms creates economies of scale that boost wages. International surveys suggest every 10 per cent increase in employment density raises wages by up to 0.4 per cent.98Ahlfeldt and Pietrostefani (2019). One Australian study found that doubling local density increases wages by 1.6-to-2.7 per cent.99Meekes (2021).